Last Friday, the Nikkei reported that Bank of Tokyo-Mitsubishi UFJ, Ltd. (BTMU, Sumitomo Mitsui Banking Corporation, and Mizuho Bank, Ltd. (MHBK, the main banking units of Japan’s three megabank groups, Mitsubishi UFJ Financial Group, Inc., Sumitomo Mitsui Financial Group, Inc., and Mizuho Financial Group, Inc., introduced voluntary limits on consumer credit card loans at half or one-third of a borrower’s annual income. The banks’ self-imposed limits are credit negative because they will likely hamper growth in credit card lending, one of few highly profitable domestic businesses for the banking sector.

The restriction responds to growing criticism from lawyers and politicians that excessive credit card lending could lead to a repeat of Asia’s 1997 debt crisis. In Japan, banks’ unsecured lending, including card lending, is not subject to the country’s money lending business law, which was revised in 2010 to restrict consumer finance companies’ unsecured lending to one-third of each customer’s annual income.

Some regional banks in Japan, such as the unrated Akita Bank, Ltd., the 77 Bank, Ltd., and Hyakugo Bank, Ltd., have implemented similar limits on credit card loans, and more banks will likely follow to fend off public criticism. Last Thursday, Nobuyuki Hirano, chairman of the Japanese Bankers Association and president of BTMU’s parent group, MUFG, said at a press conference that while he does not see a need to legally limit banks’ credit card lending, each bank should try to prevent consumer clients from taking on excessive debt.

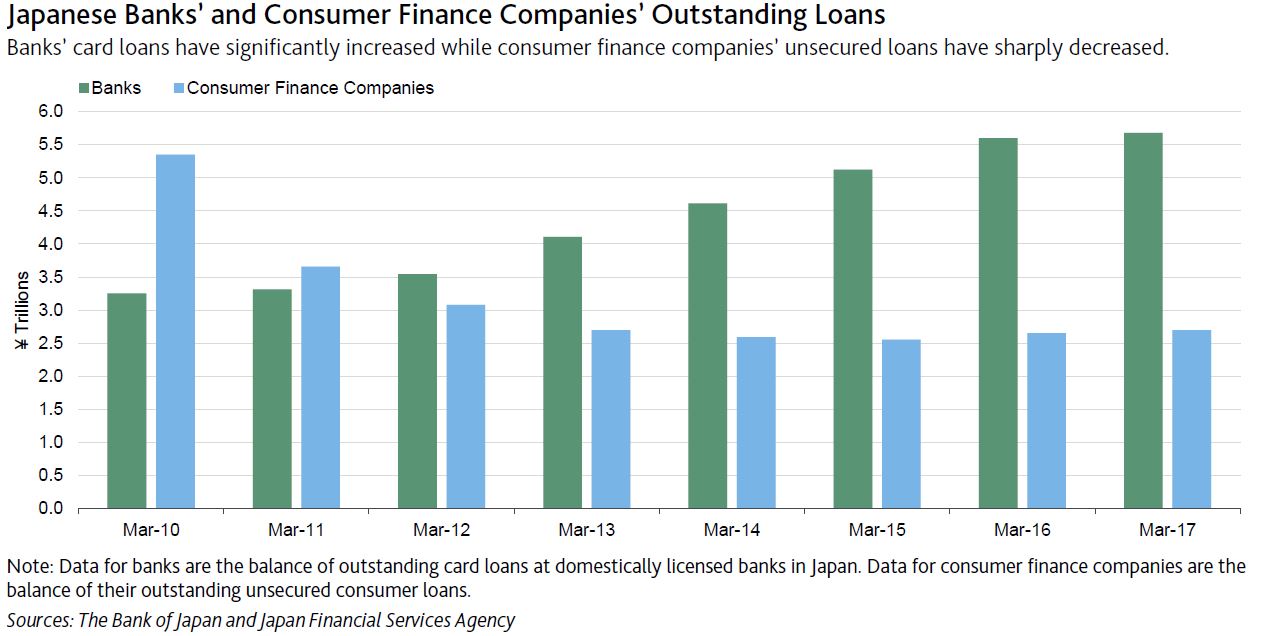

Banks have benefitted from the 2010 revision to the money lending business law, which led to the rapid growth in banks’ card loans and a sharp decrease in consumer finance companies’ unsecured loans. High margins make card lending an attractive revenue source for Japanese banks and especially domestically focused regional banks as low interest rates and weak credit demand weigh on their profitability. Interest rates on banks’ card loans are 2%-15%, significantly higher than an average loan yield of 1.1% for all Japanese banks in fiscal 2016, which ended in March 2017.

Credit card lending is riskier than secured lending, but because the size of each credit card loan is small, risks from the business are easily manageable for banks. Also, default rates for banks’ credit card loans have been low.