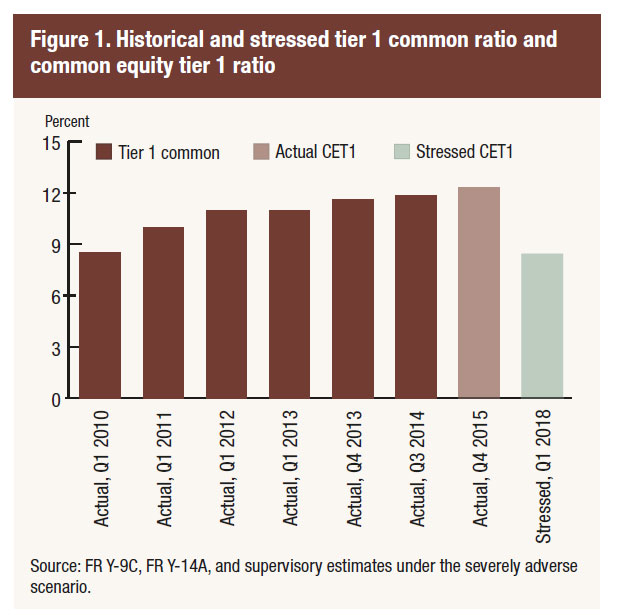

The FED has released the latest stress tests. The most severe hypothetical scenario projects that over the nine quarters of the planning horizon, aggregate losses at the 33 bank holding companies (BHCs) under the severely adverse scenario are projected to be $526 billion. This includes losses across loan portfolios, losses from credit impairment on securities held in the BHCs’ investment portfolios, trading and counterparty credit losses from a global market shock, and other losses. Projected aggregate net revenue before provisions for loan and lease losses (pre-provision net revenue, or PPNR) is $384 billion, and net income before taxes is projected to be –$195 billion. The aggregate Common Equity Tier 1 (CET1) capital ratio would fall from an actual 12.3 percent in the fourth quarter of 2015 to a post-stress level of 8.4 percent in the first quarter of 2018. Since 2009, these firms have added more than $700 billion in common equity capital.

In the adverse scenario, aggregate projected losses, PPNR, and net income before taxes are $324 billion, $475 billion, and $142 billion, respectively. The aggregate CET1 capital ratio under the adverse scenario would fall 173 basis points to its minimum over

In the adverse scenario, aggregate projected losses, PPNR, and net income before taxes are $324 billion, $475 billion, and $142 billion, respectively. The aggregate CET1 capital ratio under the adverse scenario would fall 173 basis points to its minimum over

the planning horizon of 10.5 percent in the first quarter of 2018.

This is the sixth round of stress tests led by the Federal Reserve since 2009 and the fourth round required by the Dodd-Frank Act. The 33 firms tested represent more than 80 percent of domestic banking assets. The Federal Reserve uses its own independent projections of losses and incomes for each firm.

The “severely adverse” scenario features a severe global recession with the domestic unemployment rate rising five percentage points, accompanied by a heightened period of financial stress, and negative yields for short-term U.S. Treasury securities.

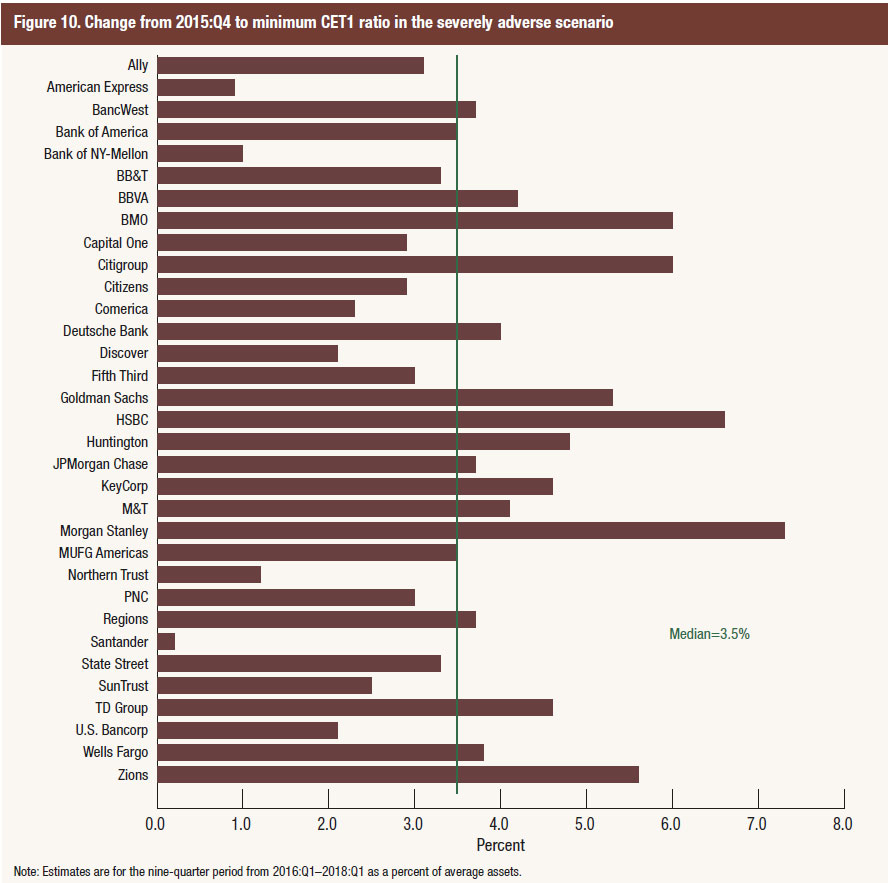

Results are provided for each individual bank. For example, the changes to CET1 ratio would vary considerably. This is much more transparent disclosure than the APRA Australian results which were aggregated and less detailed.

In addition to releasing results under the severely adverse hypothetical scenario, the Board on Thursday also released results from the “adverse” scenario, which features a moderate recession and mild deflation in the United States. In this scenario, the aggregate common equity capital ratio of the 33 firms fell from an actual 12.3 percent in the fourth quarter of 2015 to a minimum level of 10.5 percent.

In addition to releasing results under the severely adverse hypothetical scenario, the Board on Thursday also released results from the “adverse” scenario, which features a moderate recession and mild deflation in the United States. In this scenario, the aggregate common equity capital ratio of the 33 firms fell from an actual 12.3 percent in the fourth quarter of 2015 to a minimum level of 10.5 percent.

The nation’s largest bank holding companies continue to build their capital levels and improve their credit quality, strengthening their ability to lend to households and businesses during a severe recession

The Board’s stress scenario estimates use deliberately stringent and conservative assessments under hypothetical economic and financial market conditions. The results are not forecasts or expected outcomes.

The Dodd-Frank Act stress tests are one component of the Federal Reserve’s analysis during the Comprehensive Capital Analysis and Review (CCAR), which is an annual exercise to evaluate the capital planning processes and capital adequacy of large bank holding companies. CCAR results will be released on Wednesday, June 29. The Federal Reserve annually assesses whether BHCs with $50 billion or more in total consolidated assets have effective capital planning processes and sufficient capital to absorb losses during stressful conditions while meeting obligations to creditors and counterparties and continuing to serve as credit intermediaries.