We have updated our core market model with household survey data this week. One interesting dynamic is the LTI metrics across the portfolio. We calculate the dynamic LTI, based on current income and loan outstanding. This is not the same a Debt Servicing Ratio (DSR), and is less impacted by changes in mortgage rates. It is also a better measure of risk than Loan To Value (LVR)

LTI has started to become an important measure of how stretched households are. For example the Bank of England issued a recommendation to the PRA and the Financial Conduct Authority (FCA) advising that they should ‘ensure that mortgage lenders do not extend more than 15% of their total number of new residential mortgages at loan to income ratios at or greater than 4.5’.

In response, UK banks trimmed their offers. For example,

NatWest is lowering its loan-to-income ratio for some borrowers, which means they won’t be able to borrow as much to buy a home.

House buyers who stump up a deposit between 15 and 25 per cent will only be able to borrow up to 4.45 times their annual income, down from the previous maximum of 4.75 per cent.

The new multiple will apply to both single and joint earners.

The move suggests a rising number of borrowers are having to stretch themselves to be able to afford to buy a home as prices continue to rise.

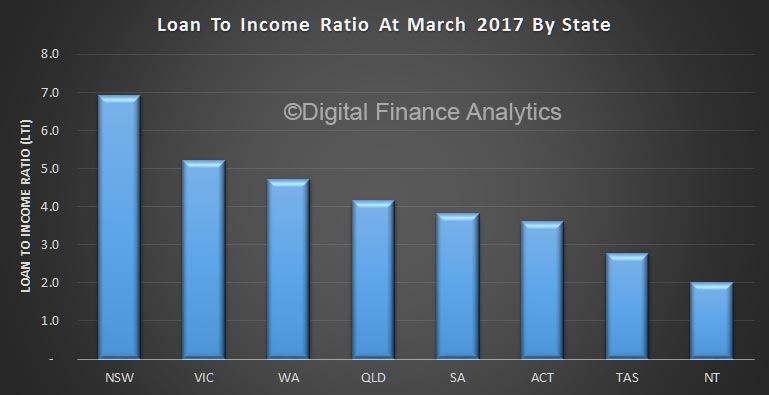

Turning to Australia, we start with a state by state comparison. The AVERAGE loan in NSW is sitting at close to 7, ahead of Victoria at over 5, and the others lower. This highlights the stress within the system for property purchasers in Sydney, with affordability a major barrier.

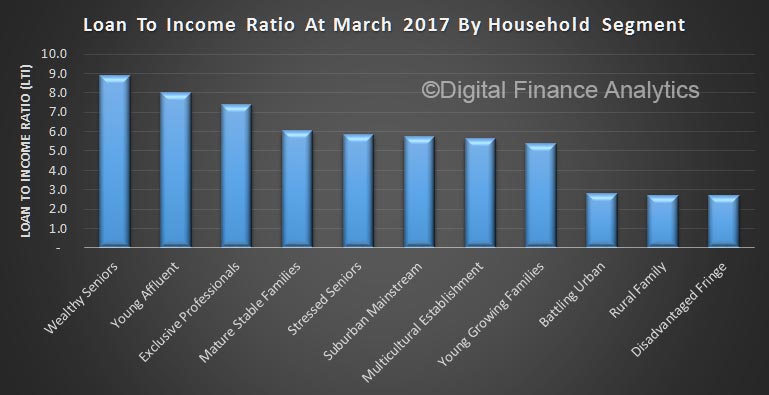

Across our household segments however, the three most exposed segments are the most affluent. Wealthy Seniors sits about 9, followed by Young Affluent at 8 and Exclusive Professionals at 7.5. On the other hand, Young Growing Families are at around 5.5 (still above the Bank of England threshold).

Across our household segments however, the three most exposed segments are the most affluent. Wealthy Seniors sits about 9, followed by Young Affluent at 8 and Exclusive Professionals at 7.5. On the other hand, Young Growing Families are at around 5.5 (still above the Bank of England threshold).

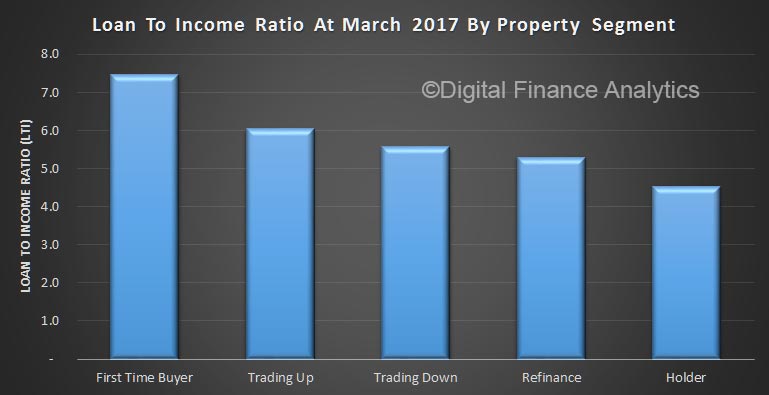

Looking at type of buyer, First Time Buyers are sitting at 7.5%, with those trading up at 6%. Holders are sitting at 4.5%

Looking at type of buyer, First Time Buyers are sitting at 7.5%, with those trading up at 6%. Holders are sitting at 4.5%

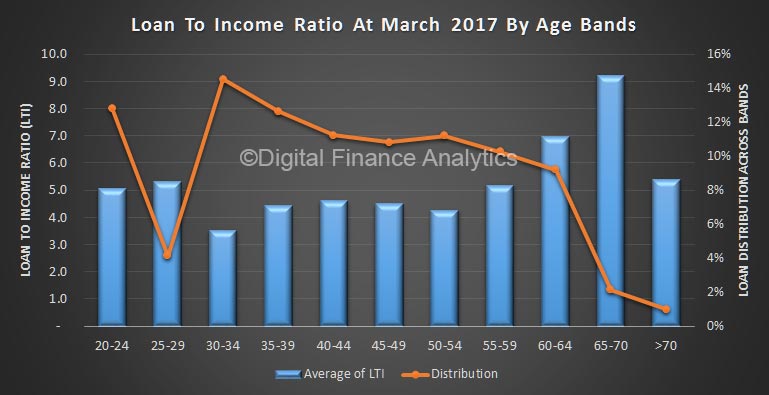

Finally, here is an average by age bands, and plotted against relative volumes of mortgages. Pressure is highest in the 60+ age groups, this is because incomes tend to fall as households move towards part-time or retirement, but these days more will still have a mortgage to manage.

Finally, here is an average by age bands, and plotted against relative volumes of mortgages. Pressure is highest in the 60+ age groups, this is because incomes tend to fall as households move towards part-time or retirement, but these days more will still have a mortgage to manage.

The dip in volumes in the 25-29 group is explained by many in this band choosing education, or starting a family, rather than home purchase, and the peak volume for purchase in after 30.

The dip in volumes in the 25-29 group is explained by many in this band choosing education, or starting a family, rather than home purchase, and the peak volume for purchase in after 30.

Overall LTI is a good indicator of affordability pressure, and the regulators could [should?] impose an LTI cap to slow lending growth, counter building affordability risks and rising housing debt.

One thought on “Latest Loan To Income (LTI) Data”