The latest ABS data for June 2015, covering all lending, continues to portray the momentum in home finance. In June overall $35bn was lent across all the property sectors, out of an overall $94bn lent across the board. $12.bn was for owner occupied loans, $6bn for refinance (an all time record) and $13.7bn for investment loans. Regulatory intervention is too little too late. The 10% speed limit on investment loans was too high, and its implementation too slow to curb the excesses. Property lending is also concentrated in the eastern states. The risks are mounting.

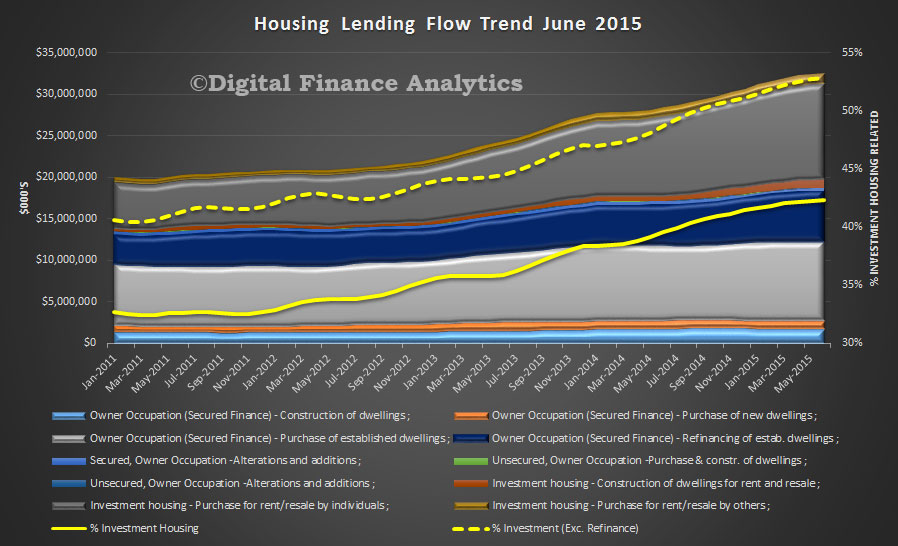

The total value of owner occupied housing commitments excluding alterations and additions rose 0.1% in trend terms (our preferred measure). Within the housing data, we see that 53% of lending for housing, excluding refinance and unsecured was for investment purposes, a record. Moreover, even if you add in unsecured finance, and refinance, it is still a peak, of 43% of all lending.

The total value of owner occupied housing commitments excluding alterations and additions rose 0.1% in trend terms (our preferred measure). Within the housing data, we see that 53% of lending for housing, excluding refinance and unsecured was for investment purposes, a record. Moreover, even if you add in unsecured finance, and refinance, it is still a peak, of 43% of all lending.

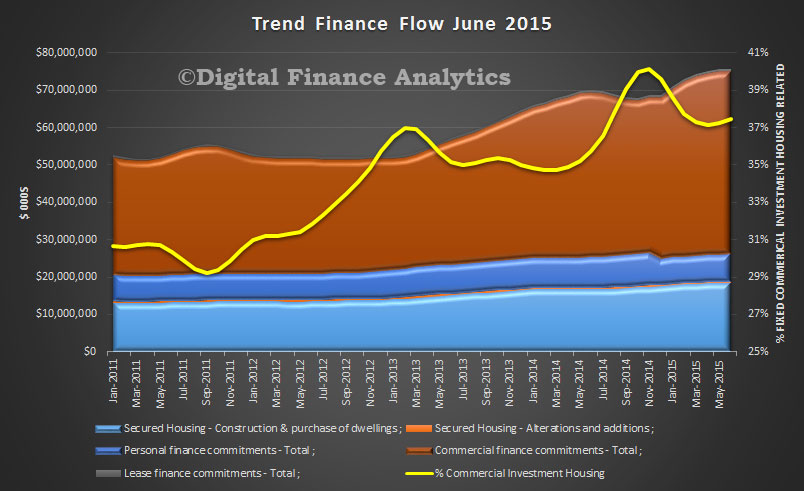

Looking across all finance categories, the trend series for the value of total personal finance commitments rose 0.5%. Fixed lending commitments rose 1.5%, while revolving credit commitments fell 1.2%. The trend series for the value of total commercial finance commitments fell 0.2%. Fixed lending commitments fell 0.4%, while revolving credit commitments rose 0.5%. The trend series for the value of total lease finance commitments rose 1.0% in June 2015. In this picture, commercial lending includes both fixed and revolving loans. We also show the proportion of fixed loans which are for investment property purposes – its sitting at 37%.

Looking across all finance categories, the trend series for the value of total personal finance commitments rose 0.5%. Fixed lending commitments rose 1.5%, while revolving credit commitments fell 1.2%. The trend series for the value of total commercial finance commitments fell 0.2%. Fixed lending commitments fell 0.4%, while revolving credit commitments rose 0.5%. The trend series for the value of total lease finance commitments rose 1.0% in June 2015. In this picture, commercial lending includes both fixed and revolving loans. We also show the proportion of fixed loans which are for investment property purposes – its sitting at 37%.

Interestingly, the ABS also notes that

statistics in this publication are currently derived from returns submitted to the Australian Prudential Regulation Authority (APRA) under the Financial Sector (Collection of Data) Act 2001, primarily for use by the Australian Bureau of Statistics (ABS). The ABS anticipates that in the coming months some lenders will revise residential mortgage data reported to APRA. These revisions are expected to result in changes in the proportion of the investment housing statistics relative to owner occupation statistics. It is not expected that aggregate data on lending statistics for housing will change significantly. The ABS is working closely with APRA and affected lenders as they remediate their data and processes.

We may get more “ANZ” type restatements between loan categories.