The ABS data to December 2015 of total lending by category shows that the total flow value of owner occupied housing commitments excluding alterations and additions rose 1.3% in trend terms (to $21.9 bn), and the seasonally adjusted series rose 0.9%.

The trend series for the value of total personal finance commitments fell 0.7% (to $6.9 bn). Fixed lending commitments fell 1.0% and revolving credit commitments fell 0.3%. The seasonally adjusted series for the value of total personal finance commitments rose 2.1%. Fixed lending commitments rose 2.6% and revolving credit commitments rose 1.5%.

The trend series for the value of total commercial finance commitments fell 0.3% (to $44.1 bn). Revolving credit commitments rose 2.4%, while Fixed lending commitments fell 1.2%. The seasonally adjusted series for the value of total commercial finance commitments fell 7.3%. Revolving credit commitments fell 18.3% and fixed lending commitments fell 3.3%.

The trend series for the value of total lease finance commitments rose 0.1% in December 2015 (to $602m) and the seasonally adjusted series rose 1.7%, after a fall of 3.8% in November 2015.

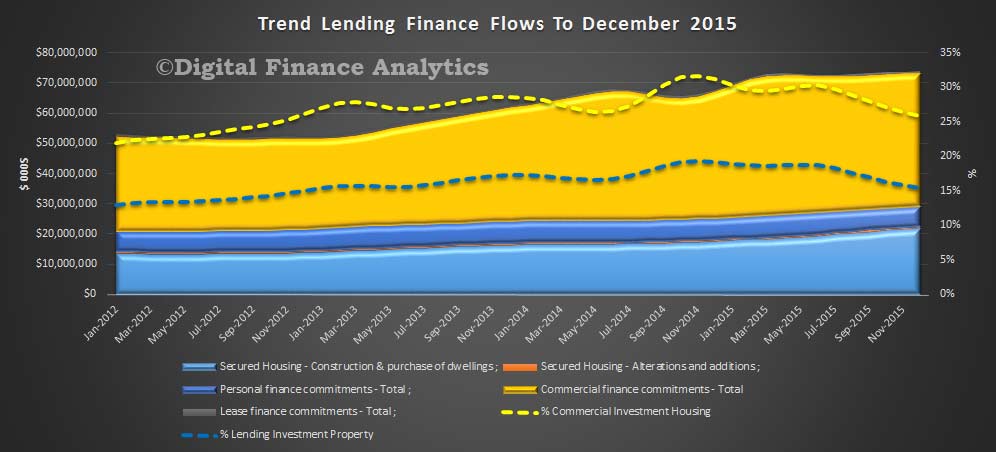

Commercial finance includes lending to individuals and other for investment property purchase. We see that lending for investment property purchase slid to 15% of all lending in December, having reached a high of nearly 20% in late 2014. In addition, the proportion of commercial lending which related to investment property purchase fell to 25% of all commercial lending, having reached a peak of 31.4% in late 2014.

Commercial finance includes lending to individuals and other for investment property purchase. We see that lending for investment property purchase slid to 15% of all lending in December, having reached a high of nearly 20% in late 2014. In addition, the proportion of commercial lending which related to investment property purchase fell to 25% of all commercial lending, having reached a peak of 31.4% in late 2014.

However, bearing in mind total commercial lending fell in the month, we see that owner occupied lending is now growing considerably faster (1.3%), compared with investment lending (down 2.4% and $11.4 bn) and commercial lending in aggregate is down 0.34%, but the non-investment housing segment rose 0.38% (to $32.7 bn).

If investment lending continues to slow, this will put more pressure on commercial lending growth, or create space for other lending to business, depending on your point of view. Or will the banks simply continue to chase owner occupied refinancing, the easy option? That said, lending to business ex. investment housing did grow, if but a little in the month. We need much stronger movement here to drive productive growth.