The RBA has released their financial aggregates to September 2017. The data confirms the growth is still in the mortgage sector, with both owner occupied and investment lending growing quite fast, significantly faster than productive business lending. So expect to see household debt rise still further. The settings are just not right to create sustainable economic growth, rather they still support a debt driven property splurge.

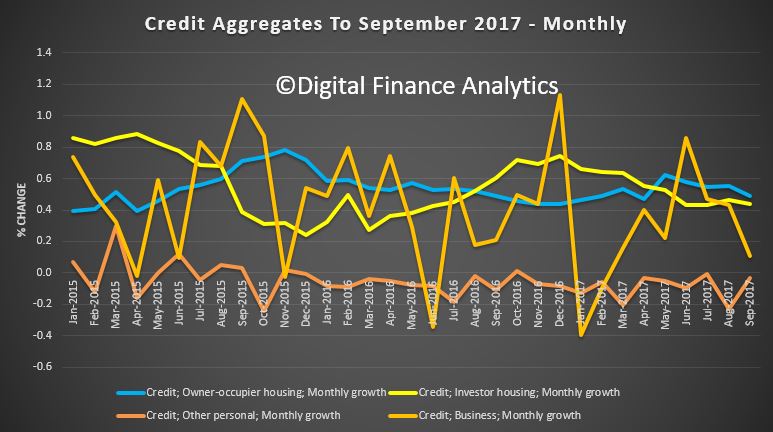

There was a significant volume of loans switched in the month – $1.4m are shown in the aggregates table, but are corrected in the growth tables, which is why investor lending is reported more strongly there.

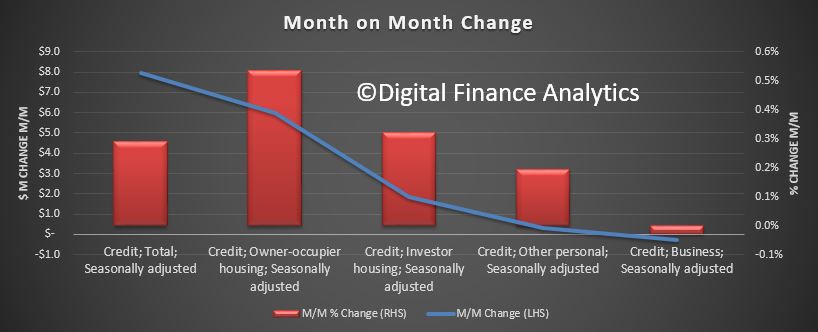

Overall lending for housing rose 0.5% in the months, or 6.6% for the year, which is higher than the 6.4% the previous year. Personal credit rose slightly in the month and down 1.% in the past year. Lending to business rose just 0.1% to 4.3% for the year, which is down from 4.8% the previous year.

Owner occupied lending grew $5.5bn or 0.5% to $1.11 trillion while investment lending rose $1.9% or 0.3% to $583 billion. Lending to business rose just $0.3 billion and personal credit rose $0.3 billion or 0.2%, the first rise since February 2017.

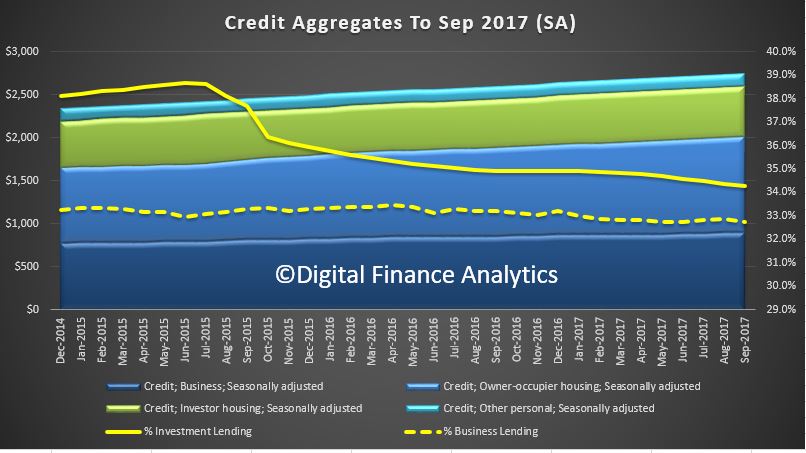

The share of investment lending remained at 34.3% of lending for housing, while the share of all lending to business fell to 32.7%.

The share of investment lending remained at 34.3% of lending for housing, while the share of all lending to business fell to 32.7%.

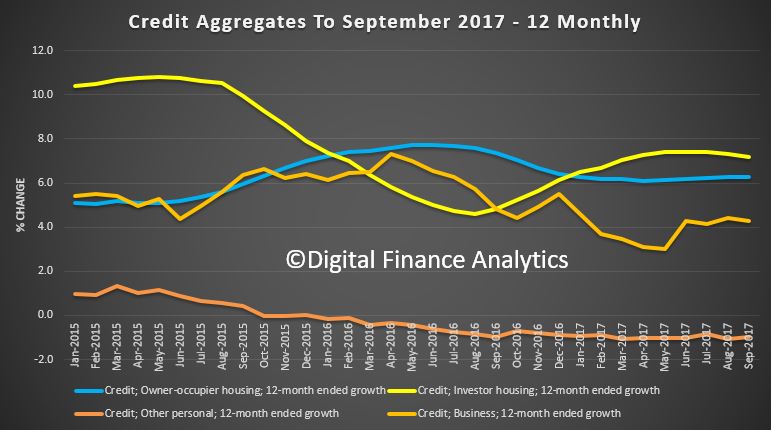

Looking at the adjusted RBA percentage changes we see that over the 12 months investor lending is still stronger than owner occupied lending, both of which showed a slowing growth trend, while last month growth in business lending continued to ease.

The RBA noted that:

Following the introduction of an interest rate differential between housing loans to investors and owner-occupiers in mid-2015, a number of borrowers have changed the purpose of their existing loan; the net value of switching of loan purpose from investor to owner-occupier is estimated to have been $59 billion over the period of July 2015 to September 2017, of which $1.4 billion occurred in September 2017. These changes are reflected in the level of owner-occupier and investor credit outstanding. However, growth rates for these series have been adjusted to remove the effect of loan purpose changes.