DFA’s coverage in the SMH today relating to the probability of default by post code has stimulated significant interest. As part of our household surveys, we capture data on mortgage stress, and when we overlay industry employment data and loan portfolio default data, we can derive a relative risk of default score for each household segment, in each post code. This data covers mortgages only (not business credit or credit cards, which have their own modelling).

Given that income growth is static or falling, house prices and mortgage debt is high, and costs of living rising, (as highlighted in our Household Finance Confidence index released yesterday), pressure on mortgage holders is likely to increase, especially if interest rates were to rise, which we have argued will happen sometime (and perhaps sooner rather than later given the recent RBA commentary on jobs and capacity). In addition, the internal risk models the major banks use, will include a granular lens of risk of default.

So, some borrowers in the higher risk areas may find it more difficult to get a mortgage, without having to jump through some extra screening hoops, and may be required to stump up a larger deposit, or cop a higher rate.

In the CBA results last week we saw some leading indicators of potential higher risks from the lender with the biggest owner occupied portfolio. So no surprise, the banks are aware of potential relative risks, especially if credit decisions are automated. In fact some of the smaller lenders appear to have greater flexibility.

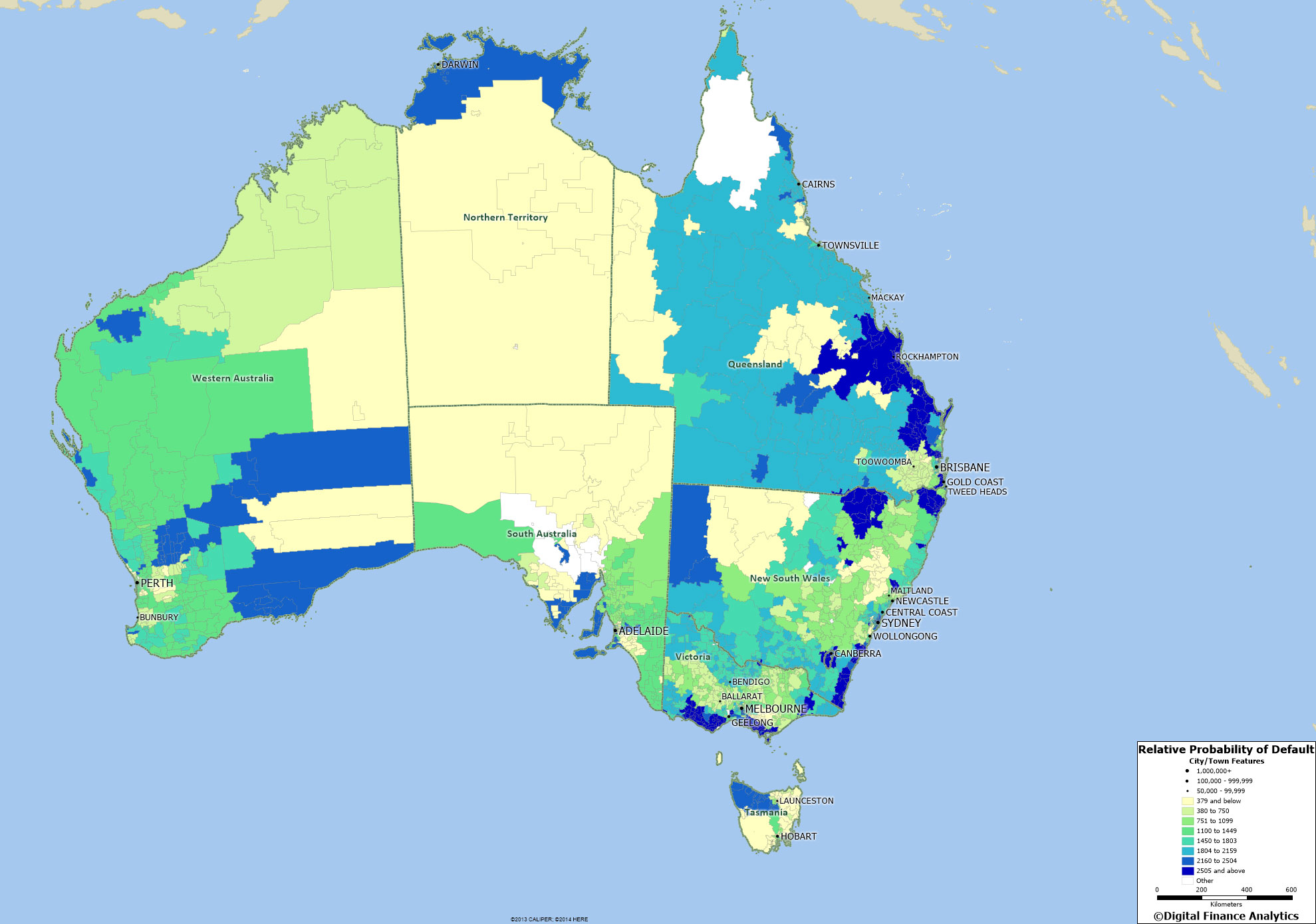

Here is the national map of relative default probability. It shows the relative ranking, with the higher probability ranked 1, and clustered into meaningful groups.

Here is the national map of relative default probability. It shows the relative ranking, with the higher probability ranked 1, and clustered into meaningful groups.

One thought on “Loan Probability Of Default By Post Code”