The February 1 FOMC meeting minutes noted two interrelated developments. First, the narrowing by “corporate bond spreads for both investment- and speculative-grade firms” to widths that “were near the bottom of their ranges of the past several years.” Secondly, some FOMC members were struck by how “the low level of implied volatility in equity markets appeared inconsistent with the considerable uncertainty attending the outlook for such policy initiatives.”

Thus, some high-ranking Fed officials sense that market participants are excessively confident in the timely implementation of policy changes that boost after-tax profits. And they may be right, according to Treasury Secretary Steven Mnuchin’s recent comment that corporate tax reform legislation may not be passed until August 2017 at the earliest. The ongoing delay at remedying the Affordable Care Act warns of a possibly even longer wait for corporate tax reform and other fiscal stimulus measures.

Treasury bond yields declined in quick response to the increased likelihood of a longer wait for fiscal stimulus. Lower benchmark yields will lessen the equity market’s negative response to any downwardly revised outlook for after-tax profits. Provided that profits avoid a replay of their year-to-year contraction of the five quarters ended Q2-2016 and that interest rates do not jump, a deeper than -5% drop by the market value of US common stock should be avoided.

The importance of interest rates to a richly priced and supremely confident equity market cannot be overstated. In fact, the rationale for an unduly low VIX index found in the FOMC’s latest minutes contained a glaring error of omission. Inexplicably, no mention was made of how expectations of a mild and thus manageable rise by interest rates have helped to reduce the equity market’s perception of downside risk. An unexpectedly severe firming of Fed policy would doubtless send the VIX index higher in a hurry.

Moreover, the FOMC’s latest minutes failed to comment on the close linkage between the now below-trend spreads of corporate bonds and an exceptionally low VIX index. As inferred from long-term statistical relationships, the VIX index now supports the possibility of corporate bond yield spreads that are much narrower than what is suggested by the default outlook. For the purpose of quantifying the latter, an aggregate version of expected default frequencies will be employed.

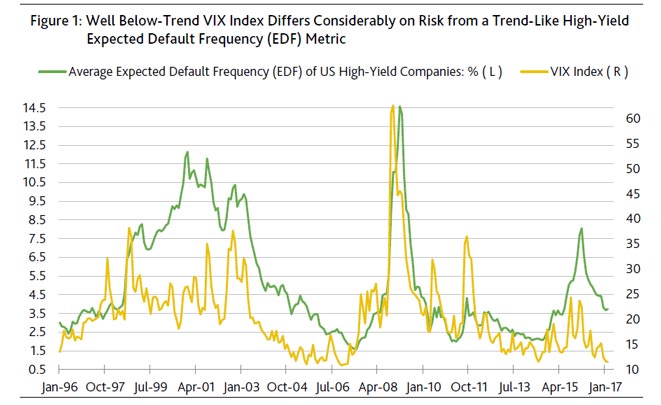

VIX Index and high-yield EDF metric differ on risk

Though the calculations of both the VIX index and EDF (expected default frequency) metrics are sensitive to asset price volatility, the messages delivered by each measure of risk can differ significantly. The 0.72 correlation between month-long averages of the VIX index and the aggregate EDF metric of US/Canadian high-yield issuers is statistically significant, but it is also far from perfect. For example, despite their relatively strong positive correlation, the VIX index and the high-yield EDF occasionally move in different directions.

Since the January 1996 inception of the average high-yield EDF metric, the medians during business cycle upturns were 3.7% for the high-yield EDF and 17.9 for the VIX index. Recently, the high-yield EDF nearly matched its median of all recovery months since December 1995, while a VIX index of less than 13 was well under its comparably measured median. In other words, the high-yield EDF metric senses a good deal more financial market risk than the VIX index does.

By way of simple regression analysis, the high-yield EDF metric now predicts an 18.3 midpoint for the VIX index, which is far above a recent reading of 12.2. Conversely, the VIX index predicts a 2.7% midpoint for the high-yield EDF metric that is less than the actual EDF of 3.7%.

The two broad measures of risk also now predict two vastly different midpoints for the US high-yield bond spread. Compared to the high-yield spread’s recent 384 bp, the VIX index predicts a midpoint of 365 bp which is much thinner than the 462 bp predicted by the recent high-yield EDF and the EDF’s three-month trend.

Both cannot be right. Nevertheless, the modest outlook for 2017’s profits from current production suggests that the EDF’s predictions for the VIX index and the high-yield spread may prove to be more accurate than the VIX index’s projections for the high-yield EDF metric and spread. However as noted earlier, the realization of modest profits growth may be sufficient for the purpose of warding off a deep slide by share prices provided that the effective fed funds rate finishes 2017 no higher than 1.13%, while the 10-year Treasury yield’s annual average for 2017 is no greater than 2.6%.