Macquarie Group has announced a net profit after tax of $A1,248 million for the half-year ended 30 September 2017 (1H18), up 19 per cent on the half-year ended 30 September 2016 (1H17) and up seven per cent on the half-year ended 31 March 2017 (2H17).

Once again the Group has exceeded market forecasts, thanks to strong growth in performance fees from its annuity style businesses, this despite a fall in net interest income. Impairments fell. Their outlook for FY18 is also stronger. More of their business is offshore than in Australia, so as the economic pace picks up in USA and Europe, they should benefit.

They gave their normal comprehensive briefing:

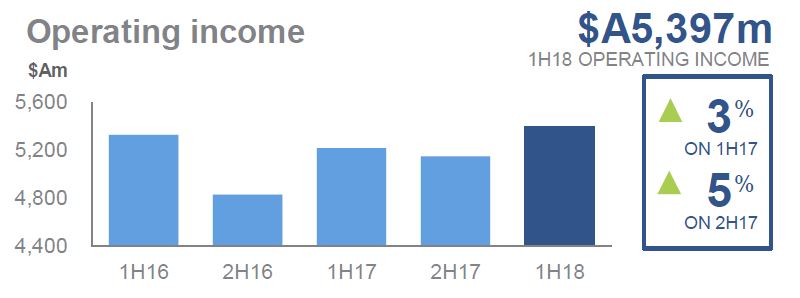

Net operating income of $A5,397 million for 1H18 was up three per cent on 1H17, while total operating expenses of $A3,693 million were down one per cent on 1H17.

Macquarie’s annuity-style businesses (Macquarie Asset Management (MAM), Corporate and Asset Finance (CAF) and Banking and Financial Services (BFS)), which represented approximately 80 per cent of the Group’s 1H18 performance, generated a combined net profit contribution of $A2,094 million, up 28 per cent on 1H17 and up 30 per cent on 2H17.

Macquarie’s annuity-style businesses (Macquarie Asset Management (MAM), Corporate and Asset Finance (CAF) and Banking and Financial Services (BFS)), which represented approximately 80 per cent of the Group’s 1H18 performance, generated a combined net profit contribution of $A2,094 million, up 28 per cent on 1H17 and up 30 per cent on 2H17.

Macquarie’s capital markets facing businesses (Commodities and Global Markets (CGM) and Macquarie Capital) delivered a combined net profit contribution of $A568 million, down 18 per cent on 1H17 and down 25 per cent on 2H17.

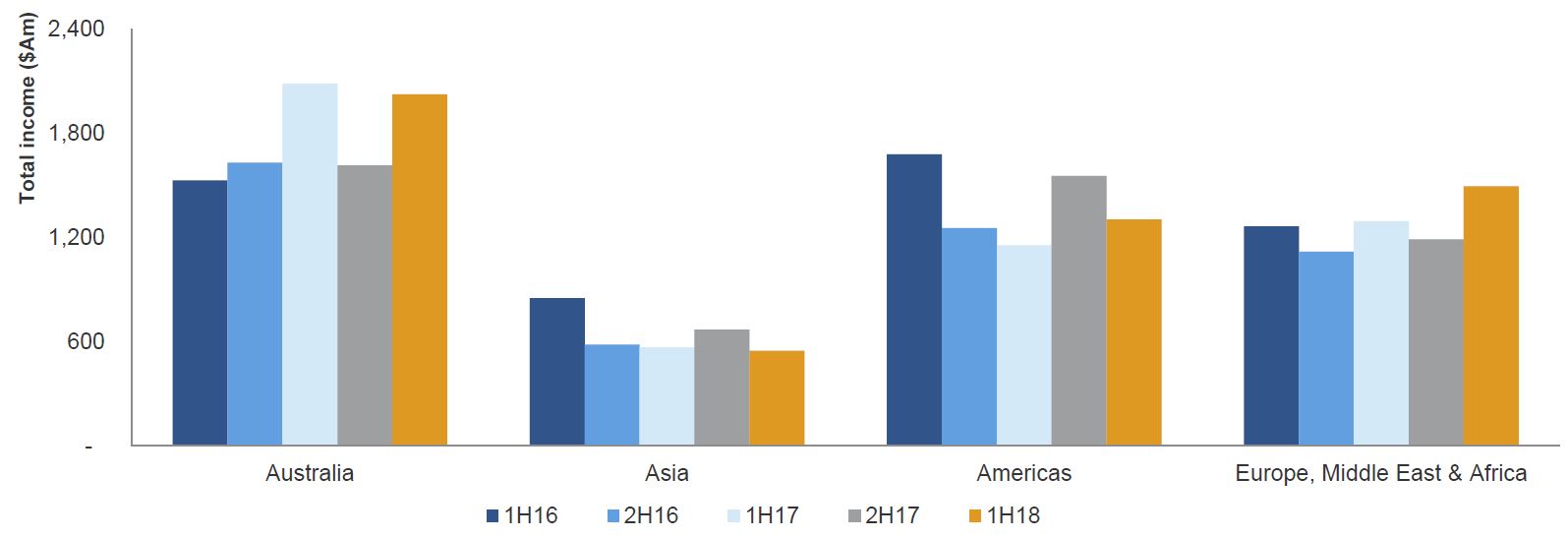

International income accounted for 62 per cent of the Group’s total income.

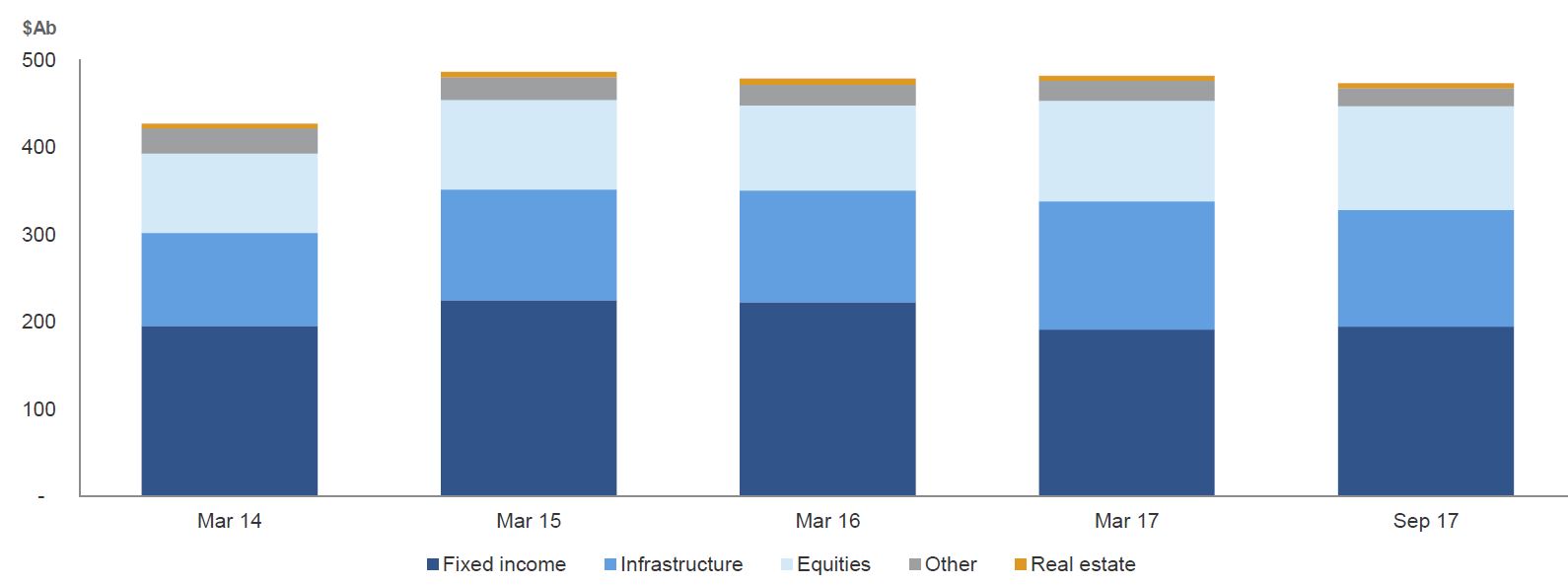

Macquarie’s assets under management (AUM) at 30 September 2017 was $A473.6 billion, down two per cent from $A481.7 billion at 31 March 2017, largely due to net asset realisations in Macquarie Infrastructure and Real Assets (MIRA)5 and unfavourable currency movements in Macquarie Investment Management (MIM), partially offset by positive market movements.

Macquarie’s assets under management (AUM) at 30 September 2017 was $A473.6 billion, down two per cent from $A481.7 billion at 31 March 2017, largely due to net asset realisations in Macquarie Infrastructure and Real Assets (MIRA)5 and unfavourable currency movements in Macquarie Investment Management (MIM), partially offset by positive market movements.

Macquarie also announced today a 1H18 interim ordinary dividend of $A2.05 per share (45 per cent franked), up on the 1H17 interim ordinary dividend of $A1.90 per share (45 per cent franked) and down from the 2H17 final ordinary dividend of $A2.80 per share (45 per cent franked). This represents a payout ratio of 56 per cent. The record date for the final ordinary dividend is 8 November 2017 and the payment date is 13 December 2017.

Macquarie also announced today a 1H18 interim ordinary dividend of $A2.05 per share (45 per cent franked), up on the 1H17 interim ordinary dividend of $A1.90 per share (45 per cent franked) and down from the 2H17 final ordinary dividend of $A2.80 per share (45 per cent franked). This represents a payout ratio of 56 per cent. The record date for the final ordinary dividend is 8 November 2017 and the payment date is 13 December 2017.

Key drivers of the change from 1H17 were:

- A one per cent increase in combined net interest and trading income to $A1,892 million, up from $A1,874 million in 1H17. The movement was mainly due to volume growth in the loan and deposit portfolios and improved margins in BFS, and a reduced cost of holding long-term liquidity in Corporate. This was partially offset by reduced interest income from Macquarie Capital’s debt investment portfolio and higher funding costs associated with an increase in principal investments, including the acquisition of Green Investment Group (GIG), as well as lower trading income in CGM as a result of lower market volatility.

- A 17 per cent increase in fee and commission income to $A2,568 million, up from $A2,203 million in 1H17, due to increased performance fee income in MAM and higher fee income from the US debt capital markets business in Macquarie Capital due to increased client activity.

- This was partially offset by reduced Life Insurance income in BFS after Macquarie Life’s risk insurance business was sold to Zurich Australia Limited in September 2016; lower mergers and acquisitions fee income in the US and Asia in Macquarie Capital; and reduced CGM brokerage and commissions income, mainly in equities due to continued low volatility across global equity markets and reduced brokerage commission rates due to the trend towards lower margin platforms.

- A one per cent decrease in net operating lease income to $A469 million, down from $A476 million in 1H17, due to improved underlying income in CAF from the Aviation, Energy and Technology portfolios offset by foreign exchange movements.

- Share of net profits of associates and joint ventures accounted for using the equity method of $A103 million in 1H18 increased from a loss of $A8 million in 1H17, primarily due to the improved underlying performance of investments held in Macquarie Capital.

- Other operating income and charges of $A365 million in 1H18, down from $A673 million in 1H17. The primary drivers were lower principal gains in Macquarie Capital and CGM and the non-recurrence of the gain on sale of Macquarie Life’s risk insurance business to Zurich Australia Limited in 1H17 by BFS, partially offset by lower charges for provisions and impairments across most operating groups.

- Total operating expenses of $A3,693 million in 1H18 decreased one per cent from $A3,733 million in 1H17, mainly due to reduced project activity in BFS, reduced employment expenses from lower average headcount, partially offset by transaction, integration and ongoing costs associated with the acquisition of GIG in Macquarie Capital.

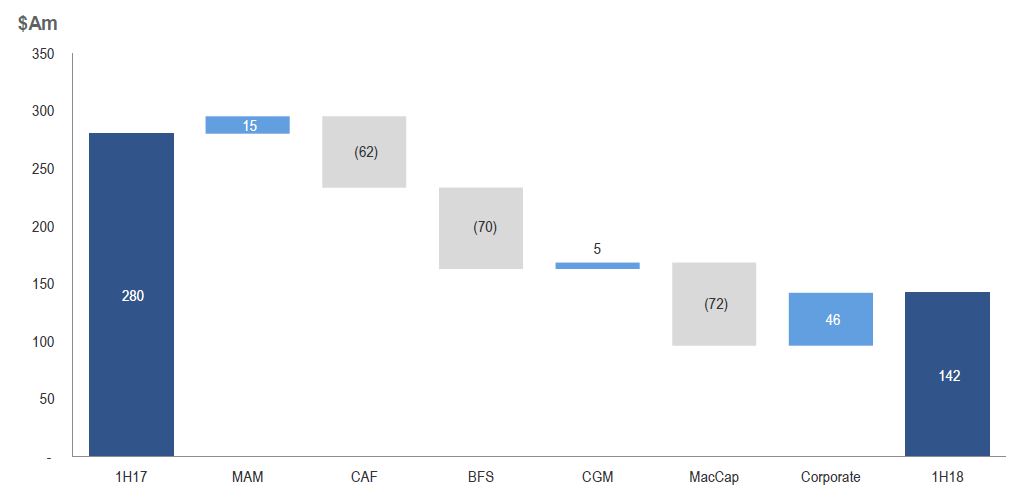

Impairments fell from $280m (1H17) to $142m 1H18.

Staff numbers were 13,966 at 30 September 2017, up from 13,597 at 31 March 2017.

Staff numbers were 13,966 at 30 September 2017, up from 13,597 at 31 March 2017.

The income tax expense for 1H18 was $A448 million, a two per cent increase from $A438 million in 1H17. The increase was mainly due to higher profit before tax. The effective tax rate of 26.4 per cent was down from 29.4 per cent in 1H17 and broadly in line with the 2H17 rate of 26.9 per cent, reflecting the geographic mix and nature of earnings.

Total customer deposits increased three per cent to $A49.4 billion at 30 September 2017 from $A47.8 billion at 31 March 2017. During 1H18, $A8.2 billion of new term funding7 was raised covering a range of tenors, currencies and product types.

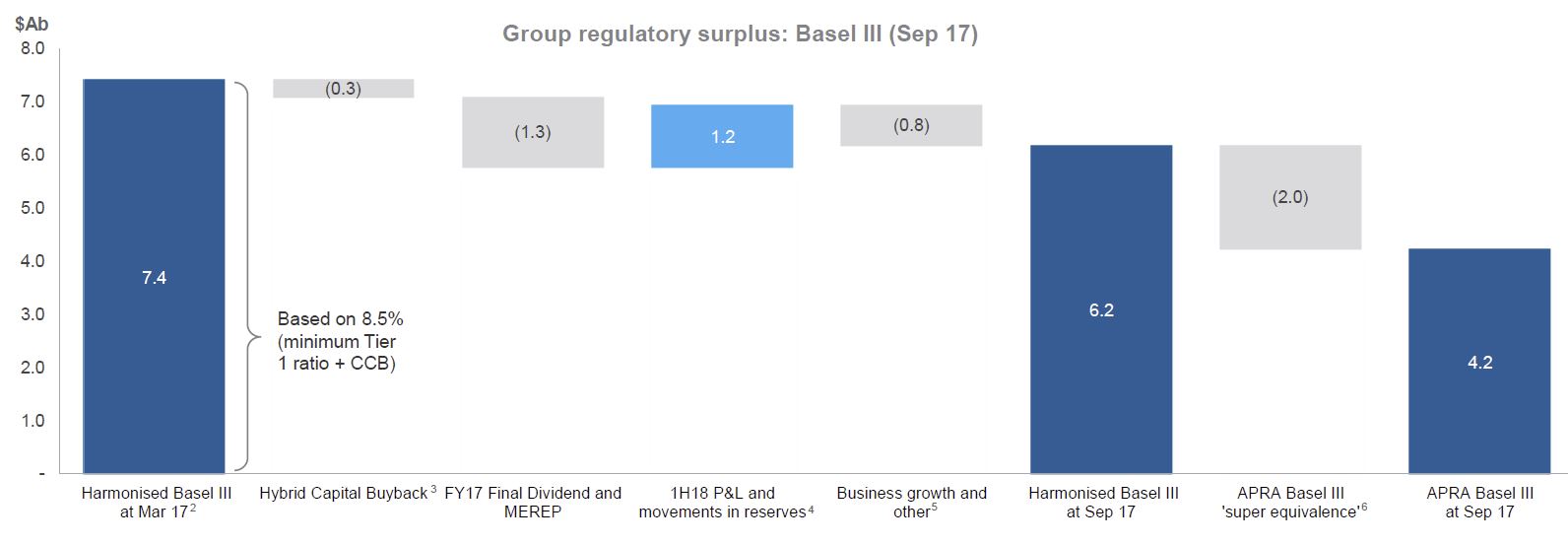

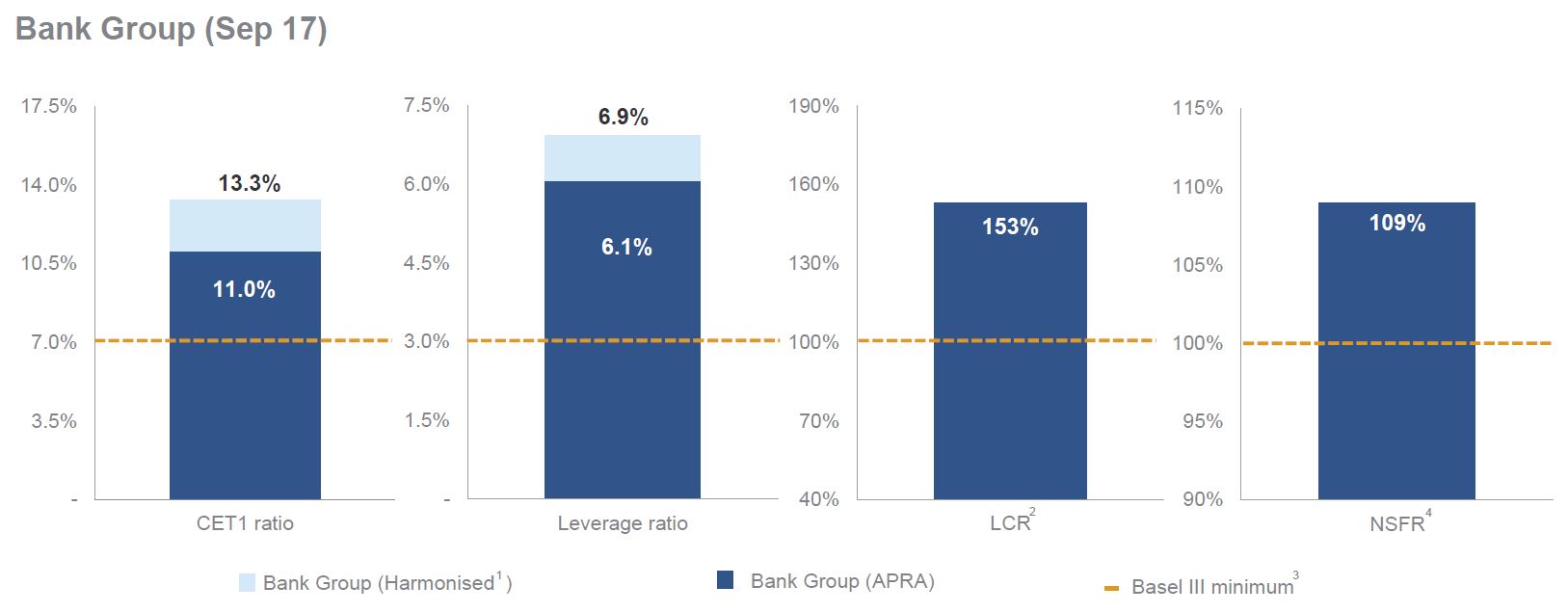

Macquarie’s financial position comfortably exceeds APRA’s Basel III regulatory requirements, with Group capital surplus of $A4.2 billion at 30 September 2017. This surplus was down from $A5.5 billion at 31 March 2017, following payment of the FY17 final dividend and FY17 Macquarie Group Employee Retained Equity Plan buying requirement, the ECS buyback and business growth, partially offset by 1H18 profit and movement in reserves. The Bank Group APRA Basel III Common Equity Tier 1 capital ratio was 11.0 per cent (Harmonised: 13.3 per cent) at 30 September 2017, down from 11.1 per cent (Harmonised: 13.3 per cent) at 31 March 2017.

The Bank Group’s APRA leverage ratio was 6.1 per cent (Harmonised: 6.9 per cent), LCR was 153 per cent and NSFR was 109 per cent at 30 September 2017.

The Bank Group’s APRA leverage ratio was 6.1 per cent (Harmonised: 6.9 per cent), LCR was 153 per cent and NSFR was 109 per cent at 30 September 2017.

The Basel Committee has delayed the finalisation of proposals to amend the calculation of certain risk weighted assets under Basel III. Any impact on capital will depend upon the final form of the proposals and local implementation by APRA.

The Basel Committee has delayed the finalisation of proposals to amend the calculation of certain risk weighted assets under Basel III. Any impact on capital will depend upon the final form of the proposals and local implementation by APRA.

APRA has delayed until at least 1 January 2019 the implementation of a new standardised approach for measuring counterparty credit risk exposures on derivatives (SA-CCR) and capital requirements for bank exposures to central counterparties. APRA has also announced that it does not expect to finalise a new market risk standard until at least 2020, with implementation from 2021 at the earliest.

APRA provided guidance around CET1 capital ratios for Australian banks to be considered ‘unquestionably strong’ and intends to release further details on how the new requirements will be implemented later this year. APRA has indicated11 that the implementation of the proposal will incorporate changes to the prudential framework resulting from the finalisation of Basel III. Based on existing guidance, Macquarie’s surplus capital position remains sufficient to accommodate any additional requirements.

To provide additional flexibility to manage the Group’s capital position going forward, the Board has approved an on-market buyback of up to $A1 billion, subject to a number of factors including the Group’s surplus capital position, market conditions and opportunities to deploy capital by the businesses. This buyback has received the necessary regulatory approvals.

Operating group performance

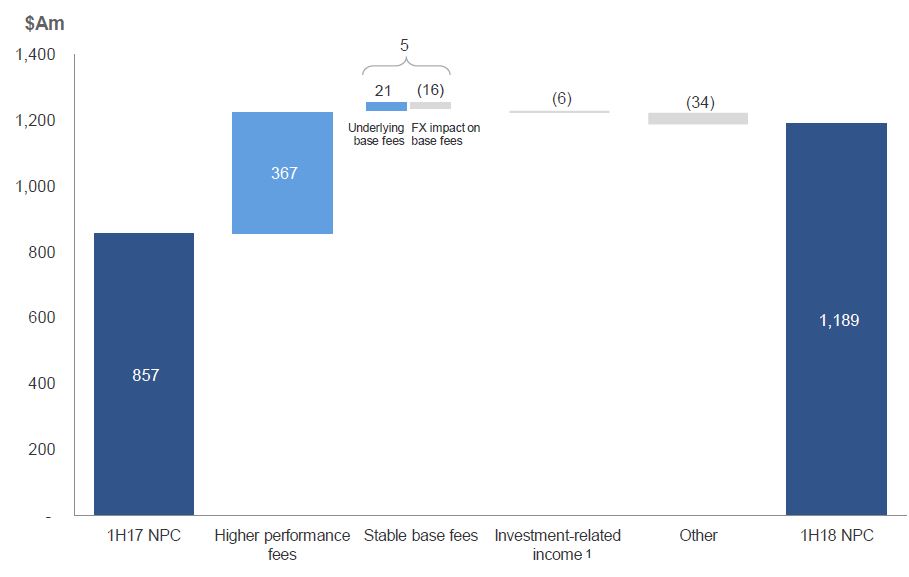

- Macquarie Asset Management delivered a net profit contribution of $A1,189 million for 1H18, up 39 per cent from $A857 million in 1H17. Performance fee income of $A537 million, from Macquarie European Infrastructure Fund 3 (MEIF3), Macquarie Atlas Roads (MQA) and other MIRA-managed funds and co-investors, was up from $A170 million in 1H17. Base fees of $A795 million were broadly in line with 1H17 as investments made by MIRA-managed funds, growth in the MSIS Infrastructure Debt business and positive market movements in MIM AUM were partially offset by asset realisations by MIRA-managed funds, net flow impacts in the MIM business and foreign exchange impacts. Investment-related income was broadly in line with 1H17 and included gains from sale and reclassification of certain infrastructure investments. Assets under management of $A471.9 billion decreased two per cent on 31 March 2017.

- Corporate and Asset Finance delivered a net profit contribution of $A619 million for 1H18, up 19 per cent from $A521 million in 1H17. The increase was mainly driven by increased income from prepayments, realisations and investment-related income in the Principal Finance portfolio and lower provisions for impairment, partially offset by lower interest income as a result of the reduction in the Principal Finance portfolio. The Asset Finance portfolio continued to perform well. CAF’s asset and loan portfolio of $A35.5 billion decreased three per cent on 31 March 2017.

- Banking and Financial Services delivered a net profit contribution of $A286 million for 1H18, up 10 per cent from $A261 million in 1H17. The improved result reflects increased income from volume growth in the loan and deposit portfolios and improved margins. 1H17 included the gain on sale of Macquarie Life’s risk insurance business net of expenses including impairment charges predominately on equity investments and intangible assets, and a change in approach to the capitalisation of software expenses in relation to the Core Banking platform. BFS deposits12 of $A46.4 billion increased four per cent on 31 March 2017 and funds on platform13 of $A78.9 billion increased nine per cent on 31 March 2017. The Australian mortgage portfolio of $A29.9 billion increased four per cent on 31 March 2017, representing approximately two per cent of the Australian mortgage market.

- Commodities and Global Markets delivered a net profit contribution of $A378 million for 1H18, down 23 per cent from $A490 million in 1H17. The result primarily reflects reduced income from the sale of investments, mainly in energy and related sectors, and lower volatility across the commodities platform resulting in reduced client activity and trading opportunities. This was partially offset by strong client flows and revenues from interest rates and foreign exchange, improved results across the equities platform, and lower operating expenses reflecting reduced commodity-related trading activity, reduced average headcount and associated activity, and realisation of benefits from cost synergies following the merger of Commodities and Financial Markets and Macquarie Securities Group. Macquarie Energy improved its Platts ranking to become the No. 2 US physical gas marketer in North America.

- Macquarie Capital delivered a net profit contribution of $A190 million for 1H18, down seven per cent from $A205 million in 1H17. The result reflects reduced investment-related income and lower M&A fee income in the US and Asia, partially offset by higher fee income from debt capital markets in the US and lower provisions and impairment charges. During 1H18, Macquarie Capital advised on 152 transactions valued at $A73 billion including being defence adviser to DUET Group in response to the $A13.4 billion acquisition by Cheung Kong Infrastructure; acquisition of 100 per cent ownership interest in RES Japan, a Japanese subsidiary of Renewable Energy Systems Group, rebranded as Acacia Renewables and focused on developing a pipeline of onshore wind energy projects; and financial advisor and equity investor in the restructuring and acquisition of the 907MW Norte III combined cycle gas plant in Juarez, Mexico. During 1H18, Macquarie completed the acquisition of the UK Green Investment Bank plc from HM Government for £2.3 billion. The Green Investment Bank, rebranded as Green Investment Group, is one of Europe’s largest teams of green energy investment specialists, with expertise in project finance and development, construction, investment and asset management of green energy infrastructure.

Macquarie advised today that ex. RBA Chief Glenn Stevens will be appointed to the Macquarie Group Limited and Macquarie Bank Limited Boards as an independent director, effective 1 November 2017.