On Monday, Macquarie Bank became the latest lender to reprice its home loans, announcing that owner-occupier variable rate loans with principal and interest repayments will increase by 0.06 of a percentage point, while those with interest-only repayments will increase by 0.10 of a percentage point across all LVR bands.

Investment and SMSF loans with variable rates will increase by 0.10 of a percentage point.

Macquarie will drop its three-year fixed rate by 10 basis points for all owner-occupier and investor loans.

The changes are effective from 13 July for new customers and 23 July for existing customers.

ING also flagged the need to increase rates by 10 basis points this week for variable owner-occupied mortgages.

Non-bank lender Pepper is also believed to have lifted rates. As of 6 July, Pepper’s rates are understood to have increased by up to 55 basis points.

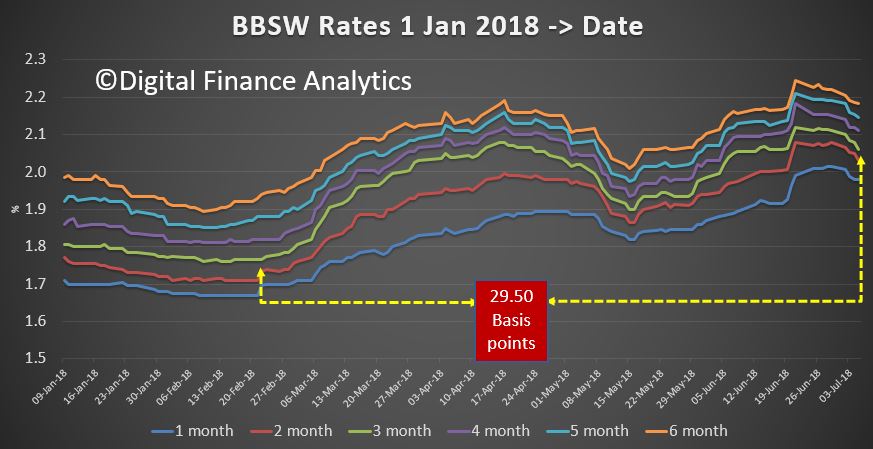

Late last month, AMP Bank and Auswide Bank also announced rate hikes in response to increased funding costs. Speaking to Mortgage Business, the chief financial officer (CFO) of Auswide Bank, Bill Schafer, attributed the lender’s decision to lift interest rates on its mortgage products to the sharp rise in the bank bill swap rate (BBSW).

“Our funding costs have risen significantly in the last four months,” Mr Schafer said.

“The BBSW — the 30-day rate and the 90-day rate — has had a large effect on our wholesale funding lines, and they’ve increased by between 30 and 35 points since the beginning of March, so that’s had a substantial effect on our net interest margin.

“We’ve been trying to absorb that across that period of time, with the hope that those costs would be relieved and the BBSW rates would decline, but now we’re nearing the end of the fourth month, we’ve taken the decision that the impact on our net interest margin is too severe, and unfortunately we needed to do an out-of-cycle rate increase.”

The latest Deloitte Australian Mortgage Report 2018, released last week, found that the biggest challenge for non-majors is access to funding relative to the big four.

“We have seen that in the most recent fortnight, some of the non-majors have had to move their standard variable rate in response to movements in the underlying BBSW spread over cash,” Deloitte financial services partner James Hickey said.

“The majors have so far been able to absorb that and not pass on that movement. They may well move on it soon, but it just goes to show the heightened level of sensitivity the regional lenders have to wholesale funding markets.”