Last week we discussed data from our core market model on negative gearing, and using our segmentation demonstrated that some, and more wealthy segments, benefit the most. There is room to trim the excesses, without necessarily removing gearing overall.

Today we look at another perspective, which supports this argument. We estimate that 61.7% of households with investment property are negatively geared – this has been rising significantly, as investment property penetration as risen. Around 2.4 million households hold investment property, but not all is mortgaged or geared.

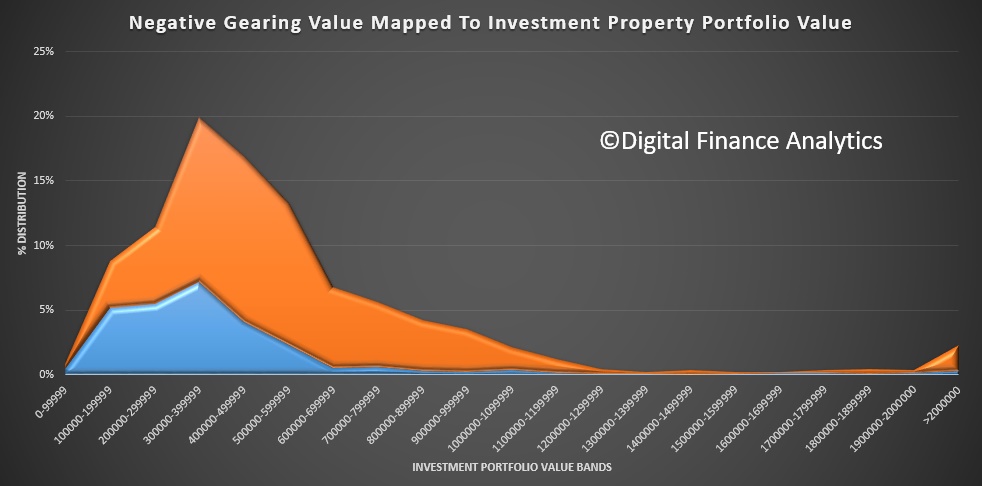

The first chart shows the value of investment property mortgages mapped to the value bands of investment property held. The orange area are households who negatively gear, the blue those who do not. This shows that the larger value portfolios have more gearing, and therefore get the greater tax benefits. Note also the small, but important peak in portfolio values above $2m. We are seeing the rise in the “professional” investor class, or Portfolio Investors as we call them.

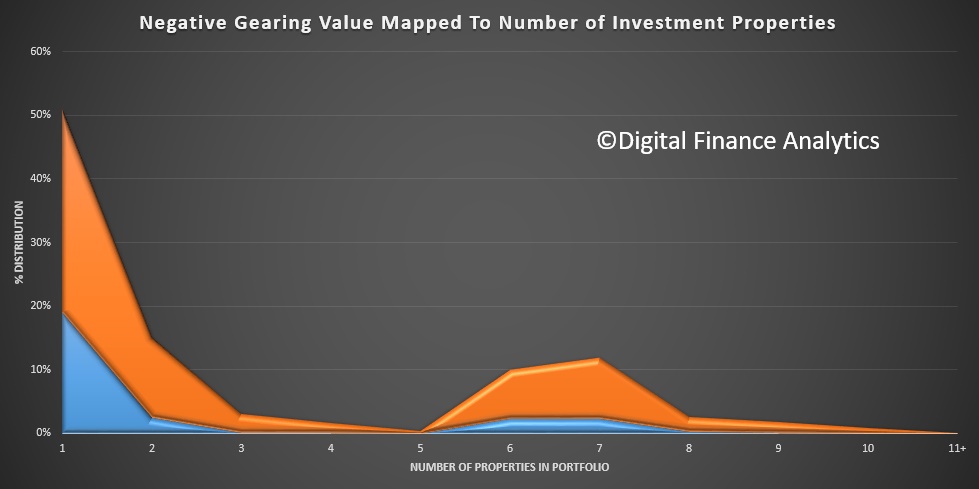

Another way to look at the value distribution is by the number of properties held in the investment portfolio. Again the orange area is property negatively geared, the blue, not geared. We see a significant spike in gearing above 5 properties, as well an an expected strong distribution in one or two properties. Our modelling shows around 79% of households have one or two properties.

Another way to look at the value distribution is by the number of properties held in the investment portfolio. Again the orange area is property negatively geared, the blue, not geared. We see a significant spike in gearing above 5 properties, as well an an expected strong distribution in one or two properties. Our modelling shows around 79% of households have one or two properties.

The overall costs of negative gearing and capital gains tax concessions are an estimated $7.7 billion annually, and three-quarters of the capital gains tax concessions are enjoyed by the top 10 per cent of income earners.

The overall costs of negative gearing and capital gains tax concessions are an estimated $7.7 billion annually, and three-quarters of the capital gains tax concessions are enjoyed by the top 10 per cent of income earners.

So, in our view, the Government should be looking to curtail the gearing available to multiple property holders, and limit the total amount which can be geared. Those two simple measures would take heat out of the market, reduce the tax burden and still allow “mum and dad” investors to benefit.

A categorical “NO” to negative gearing reform is a major mistake. Treasurer, please note! As it stands, as mortgage rates rise, and investment loans will bear the brunt of these rises, actually the poor tax payer pays for this, insulating geared investors from the extra costs. Treasury should be modelling the extra impost this will be on the budget.