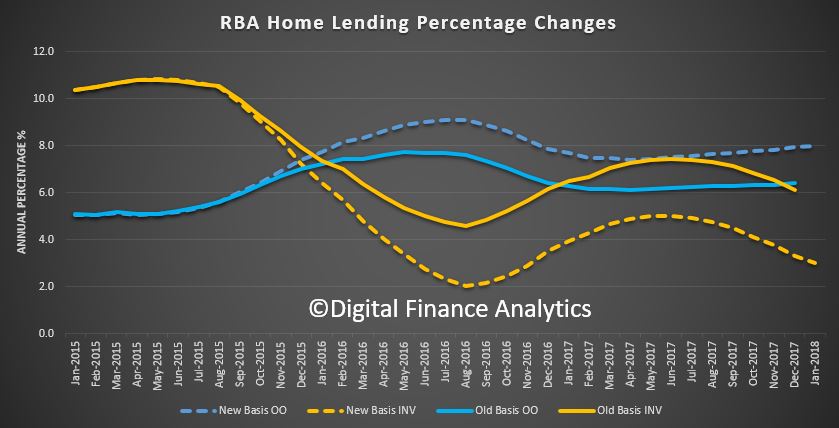

I did a mapping between the old and new basis for investor and interest only loans in the RBA credit aggregates. I posted the data earlier.

Since mid-2015 the bank has been writing back perceived loan reclassifications which pushed the investor loans higher and the owner occupied loans lower.

They have now reversed this policy, so the flow of investment loans is lower (and more in line with the data from APRA on bank portfolios). Investor loans are suddenly 2% lower. Magically!

They have now reversed this policy, so the flow of investment loans is lower (and more in line with the data from APRA on bank portfolios). Investor loans are suddenly 2% lower. Magically!

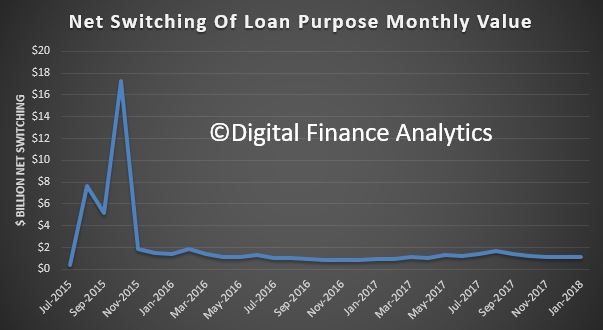

This is the monthly switching:

But two points.

First I am amazed the banks feels its OK to suddenly change the basis of their calculations, when its such a critical issue. The provided reasoning is perverse – loan switching is “normal”. Suddenly back tracking over the past two years is plain weird. The section in the Stability Report said it was going to happen. That is all.

Second, it once again highlights the rubbery nature of the data on lending in Australia. What with data problems in the banks, and at the RBA, we really do not have a good chart and compass. It just happens to be the biggest threat to financial stability but never mind.

Standing back though, despite the static growth in investment lending, do not forget that overall debt is still rising faster than incomes, by a factor of two to three times.

Owner occupied lending must be tamed too if we are to ever get back to a more even keel – the case for more macro-prudential intervention just got stronger!