The RBA said recently, when they released their credit aggregates to end March, that $51 billion of loans have been switched from investor to owner-occupier, with $1.2bn in March.

Following the introduction of an interest rate differential between housing loans to investors and owner-occupiers in mid-2015, a number of borrowers have changed the purpose of their existing loan; the net value of switching of loan purpose from investor to owner-occupier is estimated to have been $51 billion over the period of July 2015 to March 2017, of which $1.2 billion occurred in March 2017. These changes are reflected in the level of owner-occupier and investor credit outstanding. However, growth rates for these series have been adjusted to remove the effect of loan purpose changes.

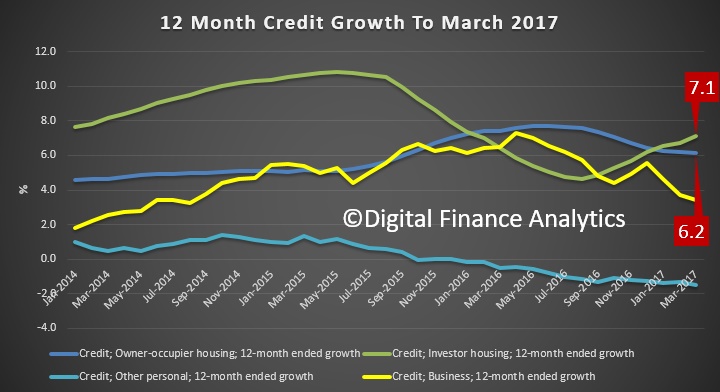

With the current balance of investor loans sitting at a record $577 billion, nearly 10% of the book has been switched to lower owner occupied rates. We of course cannot tell if this switching is legitimate, or opportunistic to get a lower interest rate and helpfully reduce the bank exposure to investor loans. The RBA data shows strong “corrected” investor growth of 7.1%, higher than owner occupied loans.

According to a report in the Australian today:

Responding to questions on notice from a Senate economic committee hearing, APRA said the switching “highlighted that some (lenders) have not had sufficiently robust practices” for monitoring the status of their borrowers and the data previously submitted to the regulator was “incorrect”.

APRA forced several banks to upgrade their reporting capabilities and, as a result, “some have strengthened their procedures”.

Tasmanian senator Peter Whish-Wilson, who asked APRA if its data was accurate, said the reclassification of loans was “concerning, whether it’s deliberate or not”.

He said: “I’d be loathe to see if any sort of systemic changes by the banks to loan classification were made to continue to grow loans to investors when it’s clear APRA is trying to crack down on what is potentially a very serious issue.”

One thought on “Mortgage Reclassification Still An Issue”