Containing our latest series on mortgage stress and probability of default, we look further at the distribution of mortgage stress and potential defaults, using data from our household surveys, which includes results up to the middle of December 2016.

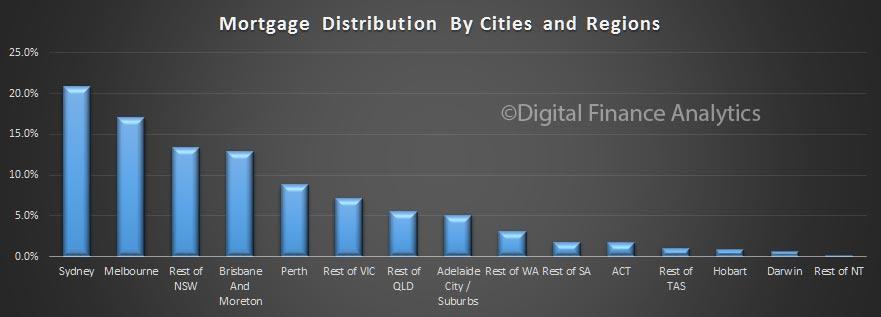

Building on the data we discussed yesterday, it is worth remembering that the bulk of mortgages reside in just a few zones across the country. This chart shows the number of loans in each of the major cities and regional areas, as a proportion of the total – we are looking here at owner occupied loans. The urban centres of Sydney, Melbourne and Brisbane hold the bulk of the loans, add in the rest of NSW and Perth, and you have more than 80% of all loans covered. So what happens in these areas is significant from a portfolio point of view. We include both loans from the banks (ADIs) and non-banks in this analysis.

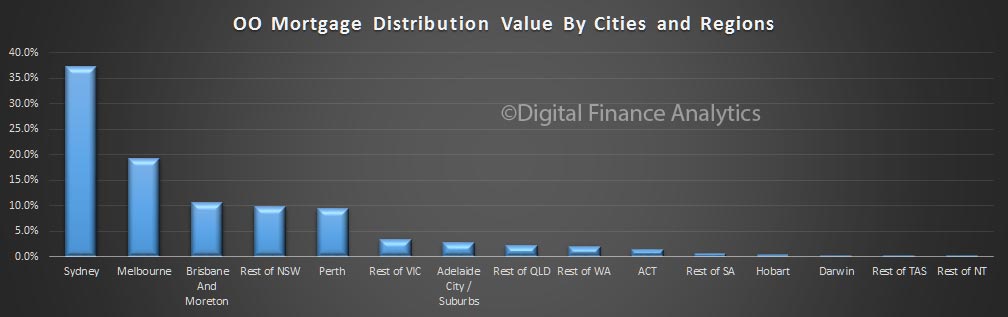

We can then look at the same analysis, but by loan value. Given the larger loans in Sydney, thanks to higher prices, the distribution based on value is more skewed, with more than 35% of loans in the greater Sydney region.

We can then look at the same analysis, but by loan value. Given the larger loans in Sydney, thanks to higher prices, the distribution based on value is more skewed, with more than 35% of loans in the greater Sydney region.

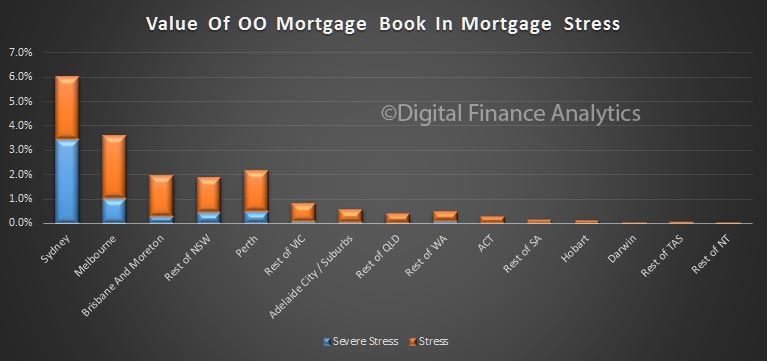

If we then overlay those households who are in mortgage stress, we see that in value terms, 6% of the portfolio in stress is in greater Sydney, 3.5% in greater Melbourne, and just over 2% in greater Perth.

If we then overlay those households who are in mortgage stress, we see that in value terms, 6% of the portfolio in stress is in greater Sydney, 3.5% in greater Melbourne, and just over 2% in greater Perth.

Total this up, and we conclude that in value terms, 18.5% of the current owner occupied loans are held by households in some degree of mortgage stress. This proportion has been rising over the past couple of years, as income growth slows, whilst household debt rises.

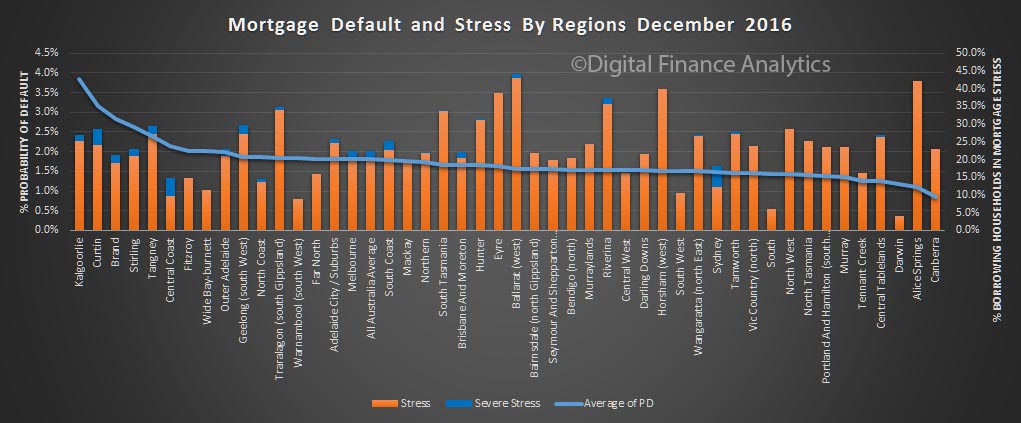

Another way to look at the data is by a more granular regional break down. Here is the probability of default by region, plus the latest reading on mortgage stress. The highest probability of default can be found in the Kalgoorlie, Curtin and Brand regions of WA. Regional WA probability of default sits at around 4%.

Another way to look at the data is by a more granular regional break down. Here is the probability of default by region, plus the latest reading on mortgage stress. The highest probability of default can be found in the Kalgoorlie, Curtin and Brand regions of WA. Regional WA probability of default sits at around 4%.

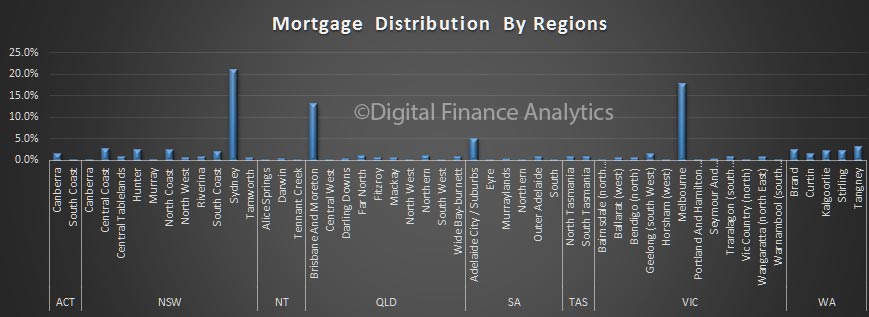

Ballarat, Horsham and Alice Springs has the highest rate of mortgage stress. But, when you look at the relative distribution of mortgages on the same basis, we see that the bulk of the mortgages reside in just a few regions. In other words, there may be high stress levels, but on low absolute volumes of loans. Once again, to see what is really going on, you need to get granular.

Ballarat, Horsham and Alice Springs has the highest rate of mortgage stress. But, when you look at the relative distribution of mortgages on the same basis, we see that the bulk of the mortgages reside in just a few regions. In other words, there may be high stress levels, but on low absolute volumes of loans. Once again, to see what is really going on, you need to get granular.

Next time we look at stress and default by our segmentation models.

Next time we look at stress and default by our segmentation models.

2 thoughts on “Mortgage Stress Covers 18.5% Of Book Value”