From The Australian Financial Review.

The number of Australian families facing mortgage distress has soared by nearly 20 per cent in the past six months to more than 900,000 and is on track to top 1 million by next year, according to new analysis of lending repayments and household incomes.

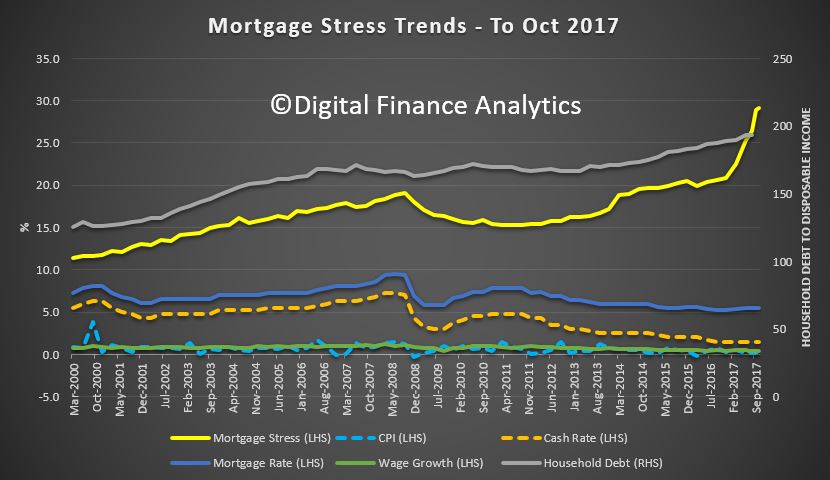

That means net incomes are not covering ongoing costs in nearly 30 per cent of the nation’s households, up from about 25 per cent in May, the analysis by Digital Finance Analytics, an independent commentator, shows.

Stagnant incomes, rising costs, unemployment, the likelihood that rates are more likely to rise than fall mean the number of families struggling to make ends meet is expected to continue increasing, the analysis shows.

Lenders’ recent attempts to build market share by lowering underwriting standards is also expected to begin appearing in the numbers as households struggle to repay jumbo loans, it shows.

“Risks in the system will continue to rise,” Martin North, DFA principal, said. “The numbers of households impacted are economically significant,” “Mortgage lending is still growing at three times income. This is not sustainable.”

Brendan Coates, a fellow at the Grattan Institute, a public policy think tank, said: “Even a relatively small rise in the interest rates paid by households would crimp their spending.

“If interest rates increase by 2 percentage points, mortgage payments on a new home will be less affordable than at any time in living memory, apart from a brief period around 1989 — an experience that scarred a generation of home-owners.”

Nearly 22,000 households, of which 11,000 are professionals or young affluent, are facing severe distress, which means they are unable to meet mortgage repayments from current income and are having to manage by cutting back spending, putting more on credit cards, refinance, or sell their home.

About 52,000 households risk 30-day default in the next 12 months, up 3000 from the previous month. A lender, or creditor, can issue a default notice to a borrower behind on debt.

Bank portfolio losses are expected to be around 3 basis points, rising to about 5 basis points in Western Australia.

Mr Coates said: “Growing household debt has made the Australian economy more vulnerable. But the debt situation is not as worrying as the aggregate figures suggest.

“Most debt is held by higher income households and Reserve Bank research shows that relatively few households have high loans-to-total-assets ratios.

“Stagnating house prices — still the most likely scenario over the next couple of years — wouldn’t be enough to significantly trouble the banks.”

Rather than a banking crisis, higher debts could cause a rapid fall in household spending in the event of a downturn, he said.

“Household consumption accounts for well over half of gross domestic product. Recent Reserve Bank of Australia research shows that households with higher debts are more likely to reduce spending if their incomes fall,” he said.

Economists generally argue mortgage stress, stagnant income growth and low inflation mean the Reserve Bank will be unlikely to raise interest rates any time soon.

But that could change if there was another disruption to international financial markets, such as the 2008 shock, which sharply increased banks’ funding costs and raised mortgage rates.