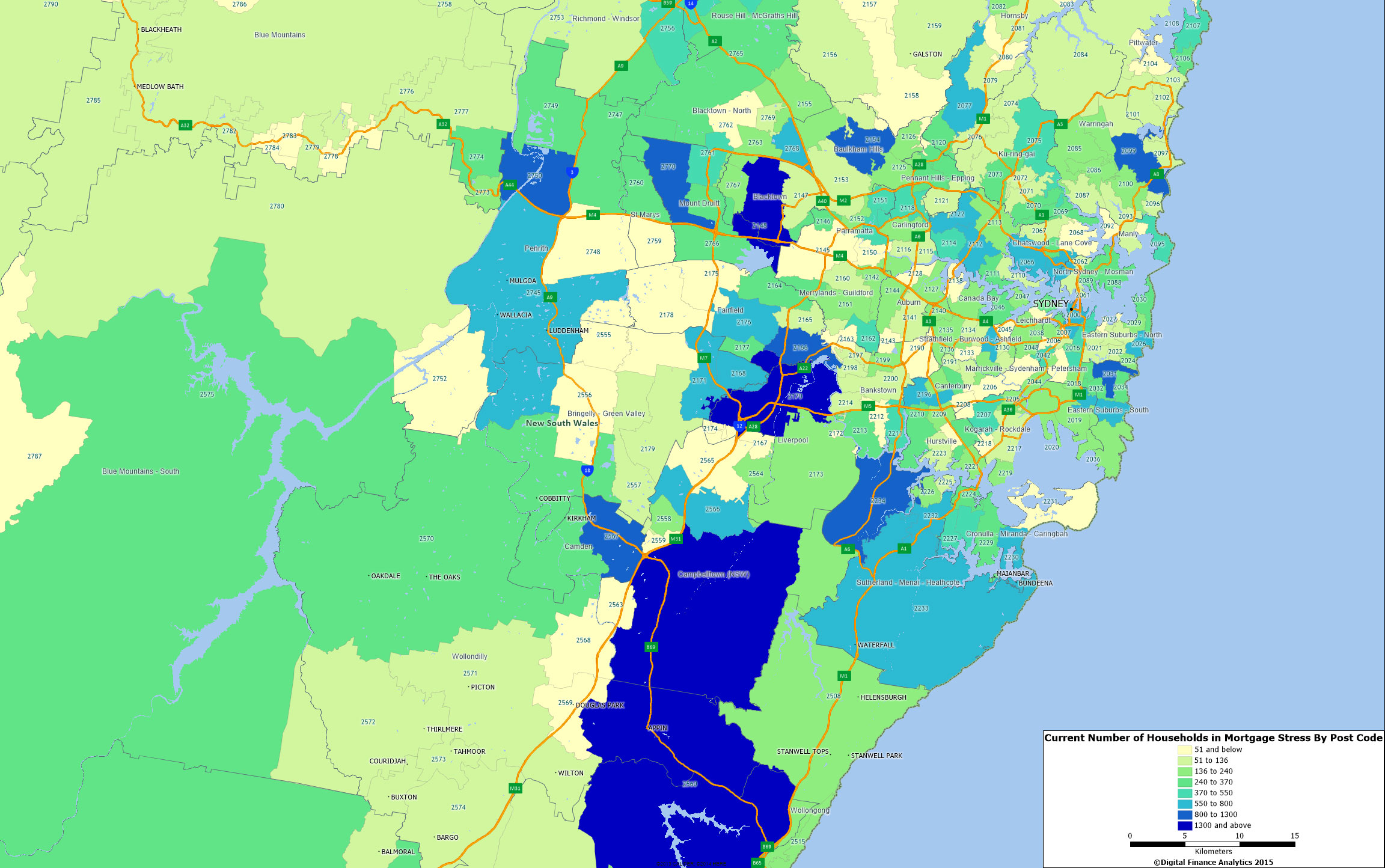

Continuing our analysis of mortgage stress (one of the drivers of our estimation of the probability of default), we have estimated the actual number of households in each post code who are experiencing stress currently. To recap, Mortgage stress is a poorly defined term. The RBA tends to equate stress with defaults (which remain at low levels on an international basis). A wider definition is 30% of income going on mortgage repayments (not consistently pre-or-post tax). This stems from the guidelines of affordability some banks used in 1980’s and 1990’s, when economic conditions were different from today. This is a blunt instrument. DFA does not think there is a good indicator of mortgage stress, so we use a series of questions to diagnose mortgage stress focusing on owner occupied households. Through these questions we identify two levels of stress – Mild and Severe.

- Mild = households maintaining repayments, but by reprioritising expenditure, borrowing more on loans or cards, and refinancing

- Severe = households who are behind with their repayments, are trying to sell, are trying to refinance, or who are being foreclosed

We maintain a rolling sample of 26,000 statistically representative households using a custom segment model nationally. Each month we execute omnibus surveys to 2,000 households. Our questions provide a current assessment of mortgage stress. We also model and project likely mortgage stress given the current and expected economic conditions. You can read about the methodology here. The map shows the number of households who are currently in mortgage stress.

This is an interesting view because it shows the absolute estimated number, not the percentage of households. We have not published this view before.

This is an interesting view because it shows the absolute estimated number, not the percentage of households. We have not published this view before.

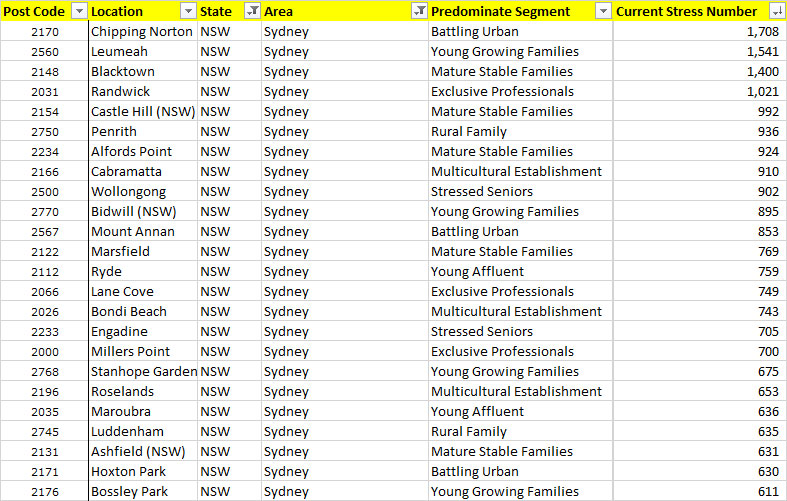

Most striking is the range of master household segments which are represented. An indication that stress is not directly correlated with affluence. We will post data for some of the other regions another time.

Most striking is the range of master household segments which are represented. An indication that stress is not directly correlated with affluence. We will post data for some of the other regions another time.