Financial markets were recently visited by a rarity. During the past week, the VIX index closed under 10 points on May 8 and 9. Since its start in 1990, the VIX index has closed under 10 points on only 11, or 0.1%, of the span’s nearly 7,000 trading days.

Today’s very low VIX index reflects a great deal of confidence that there won’t be a deep sell-off by equities. Not only is there effectively little demand for insuring against a harsh correction, but sellers of such insurance are will to accept a low price for protection against a market plunge.

This insouciance seems odd given how richly priced the US equity market is relative to corporate earnings and the prospective returns from other assets such as corporate bonds. The current market value of US common stock — according to a model based on pretax profits from current production and Moody’s long-term Baa industrial company bond yield — exceeds its midpoint valuation by a considerable 24%. During 1999-2000’s memorable equity rally, the market value of US stocks first climbed 24% above its projected midpoint in 1999’s first quarter and would remain at least that high through 2000’s second quarter. During January 1999 through June 2000, the actual market value of US common stock exceeded its projected midpoint by 51%, on average.

Another comparison of the two periods shows a similarly striking difference between them. The earlier period averages of a 15.4:1 ratio for the market value of common stock to pretax operating profits and 8.05% for the long-term industrial company bond yield were far above the recent ratio of 11.7:1 and the latest Baa industrial yield of 4.68%.

In stark contrast to the current situation, during January 1999 through June 2000 the VIX index averaged a substantially higher 24.3 points when the market value of US common stock was at least 24% above its projected midpoint. Back then, the market had a greater appreciation of the considerable downside risk implicit in an overvalued equity market.

Two prior cases of a below-10 VIX index preceded vastly different outcomes

January 2007 and December 1993 were the two prior moments when the VIX index spent some time under the 10-point threshold. What followed them differed drastically.

January 2007 was merely 11 months before the December 2007 start to the worst recession since the Great Depression. In contrast, December 1993 was followed by 1994’s 4.0% annual advance by real GDP that was the first of a seven year span that had real GDP growing by a now unheard of 4.0% annually, on average. Far different was 2007’s 1.8% annual rise by real GDP that was at the start of what would be real GDP’s 0.9% average annual rise of the seven-years-ended 2013.

In the year following December 1993’s ultra-low VIX score, the market value of US common stock fell by -3.2% despite 1994’s 18.6% surge by pretax operating profits. A lift-off by the average 10-year Treasury yield from Q4-1993’s 6.13% to Q4-1994’s 7.96% was to blame for 1994’s short-lived drop by share prices. Nevertheless, partly because of 1994’s very strong showing by business activity, the earnings-sensitive high-yield bond spread narrowed from Q4-1993’s 438 bp to Q4-1994’s 350 bp.

For the year following January 2007’s brief stay by a less than 10-point VIX index, a drop by the 10-year Treasury yield from January 2007’s 4.64% to January 2008’s 4.00% failed to stave off a -3.4% drop by the market value of US common stock largely because of yearlong 2007’s -7.5% contraction of pretax operating profits. A swelling by the high-yield bond spread from January 2007’s 287 bp to January 2008’s 674 bp stemmed from the worsened outlook for business activity.

VIX Index and high-yield EDF differ drastically on yield spreads

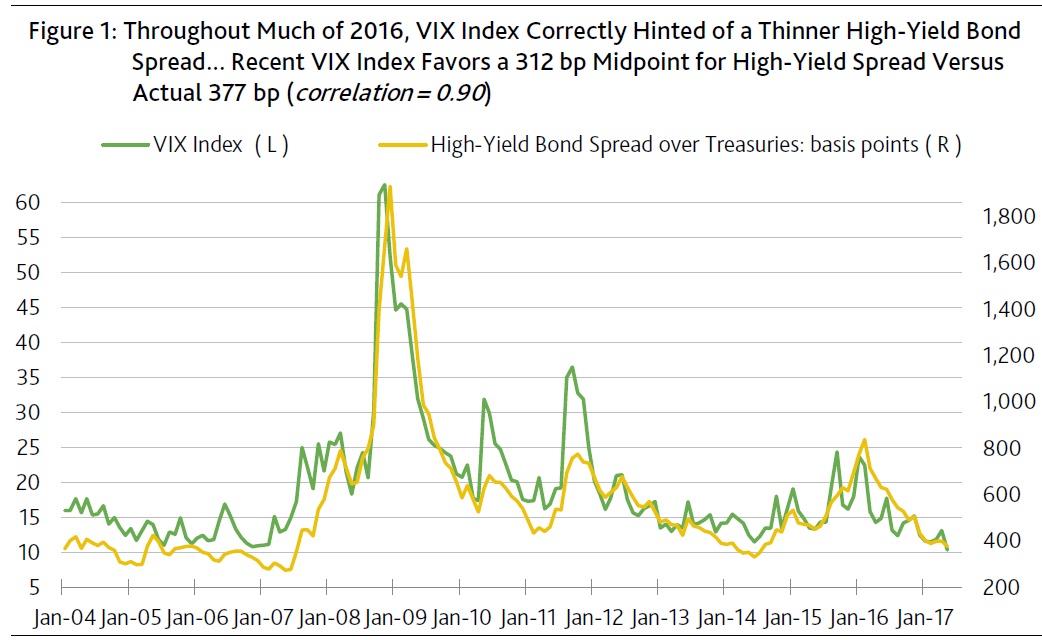

May-to-date’s average VIX index of 10.4 points favors a 312 bp midpoint for the high-yield bond spread, which is much thinner than the recent actual spread of 377 bp. Throughout much of 2016, the VIX index proved to be a reliable leading indicator of where the high-yield spread was headed. Nevertheless, if only because the VIX index now resides in the bottom percentile of its historical sample, a higher VIX index is practically inevitable. Once the VIX index approaches its mean, the high-yield spread will be much wider than the recent 377 bp. (Figure 1.)