On first blush, the revised federal budget has improved according to the MYEFO (Mid-Year Economic and Fiscal Outlook) released by the Treasurer today. But consumers are the weak link, and wage growth and consumption a problem – no wonder there is now talk of tax cuts for consumers! In addition, more savings are forecast, including an extension of the waiting period for newly arrived migrants to access welfare benefits and a freeze on higher education funding.

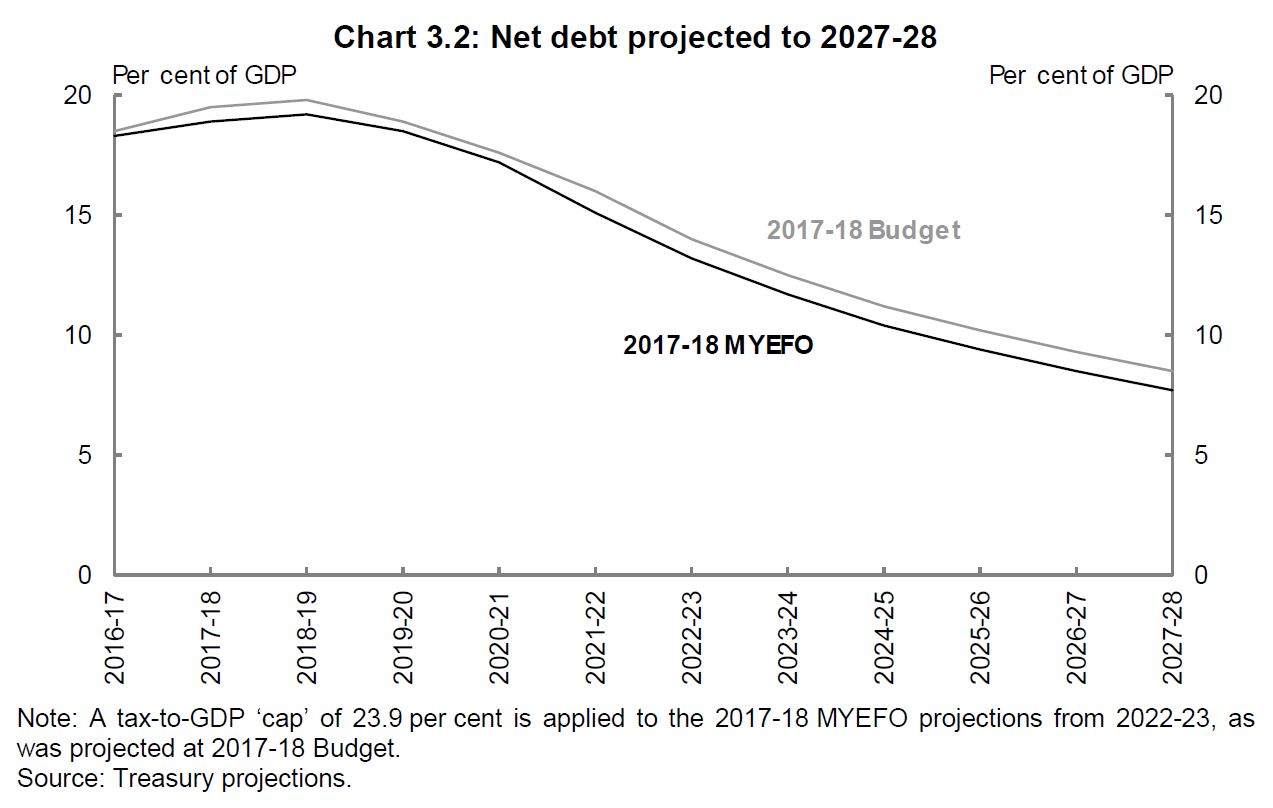

The budget is, they say, on track to return to balance in 2020-21, and overall debt as share of GDP is set to fall further. The latest projected surplus of $10.2 billion in 2020-21 is an improvement of $2.7 billion compared to May’s Budget estimate.

At the 2017-18 Budget, gross debt was projected to be $725 billion in 2027-28. Gross debt is now projected to reach around $684 billion by 2027-28 — a fall of around $40 billion. But absolute debt is still rising!

At the 2017-18 Budget, gross debt was projected to be $725 billion in 2027-28. Gross debt is now projected to reach around $684 billion by 2027-28 — a fall of around $40 billion. But absolute debt is still rising!

The improvement is driven by a rise in company profits, and company tax take. Commodity prices helped also, although they remain a key uncertainty to the outlook for the terms of trade and nominal GDP, especially in relation to the Chinese economy.

The improvement is driven by a rise in company profits, and company tax take. Commodity prices helped also, although they remain a key uncertainty to the outlook for the terms of trade and nominal GDP, especially in relation to the Chinese economy.

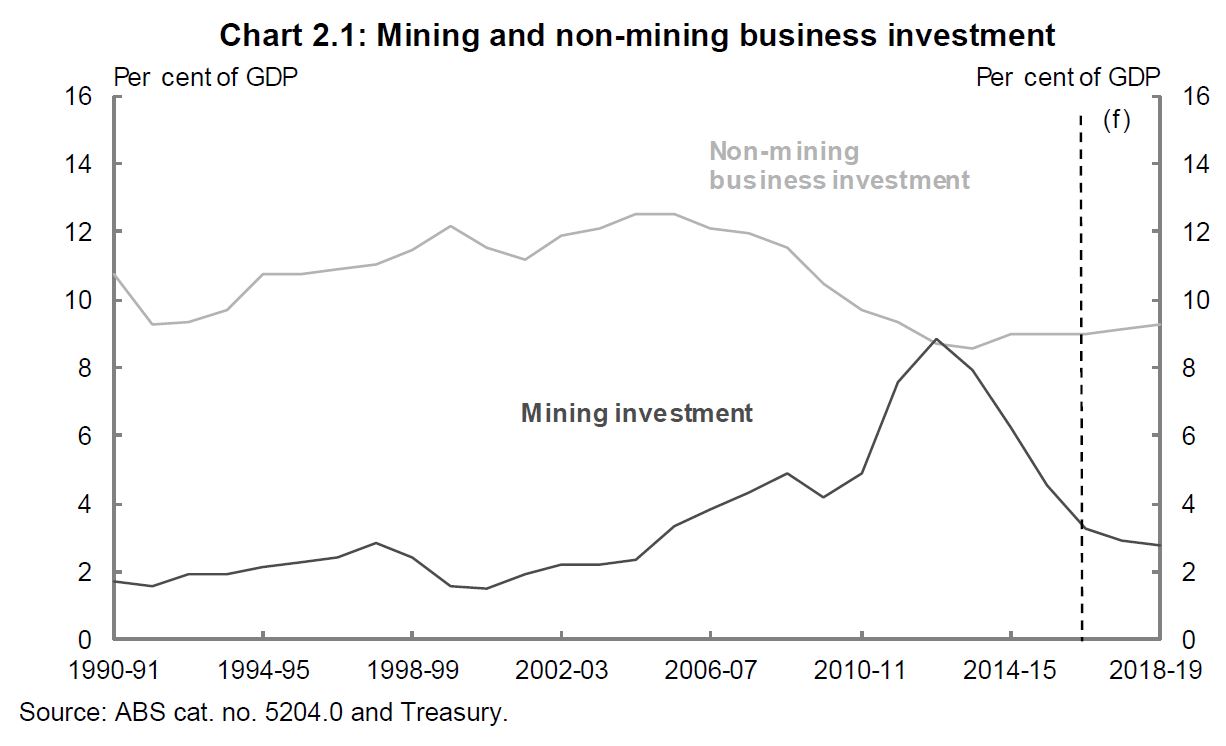

They say the fall off in mining investment is easing, while non-mining business investment is predicted to rise (a little), but we think overall business investment remains an issue.

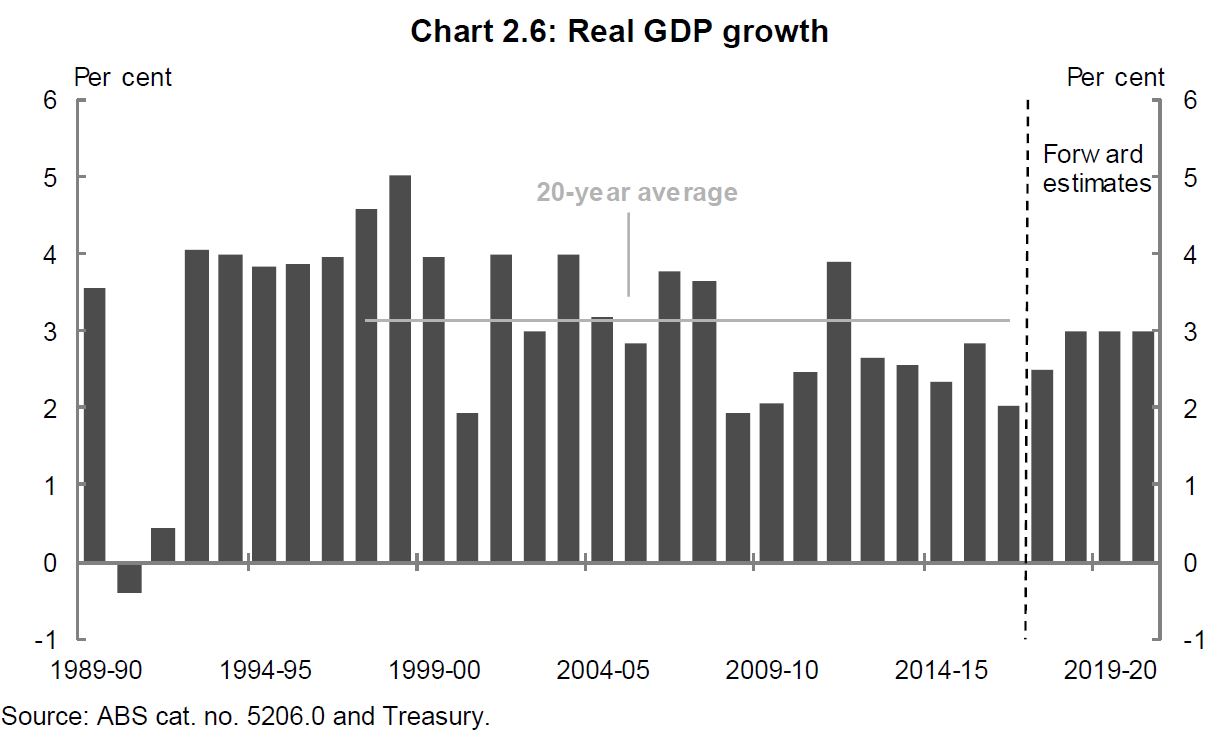

Real GDP is forecast to grow by 2.5% in 2017-18, lower than at budget time (2.75%). Beyond that, real GDP is forecast to grow at 3% in 2018 19, per the original budget.

Real GDP is forecast to grow by 2.5% in 2017-18, lower than at budget time (2.75%). Beyond that, real GDP is forecast to grow at 3% in 2018 19, per the original budget.

The 2017-18 forecast is lower driven by anemic outcomes for wage growth and domestic prices. More than 360,000 jobs at a rate of 1,000 jobs a day having been created in 2017. Yet, wages are now forecast to remain lower for longer, with index growth of 2.25% in June 2018, 0.25% lower than at budget time, and 2.75% to June 2019. They admit wages growth is lower than expected, but they still hope lifting economic momentum will lift wages, eventually – despite the very high levels of underemployment, and structural changes in working patterns. This lower forecast for wages is expected to weigh on personal income tax receipts and slow household consumption.

The 2017-18 forecast is lower driven by anemic outcomes for wage growth and domestic prices. More than 360,000 jobs at a rate of 1,000 jobs a day having been created in 2017. Yet, wages are now forecast to remain lower for longer, with index growth of 2.25% in June 2018, 0.25% lower than at budget time, and 2.75% to June 2019. They admit wages growth is lower than expected, but they still hope lifting economic momentum will lift wages, eventually – despite the very high levels of underemployment, and structural changes in working patterns. This lower forecast for wages is expected to weigh on personal income tax receipts and slow household consumption.

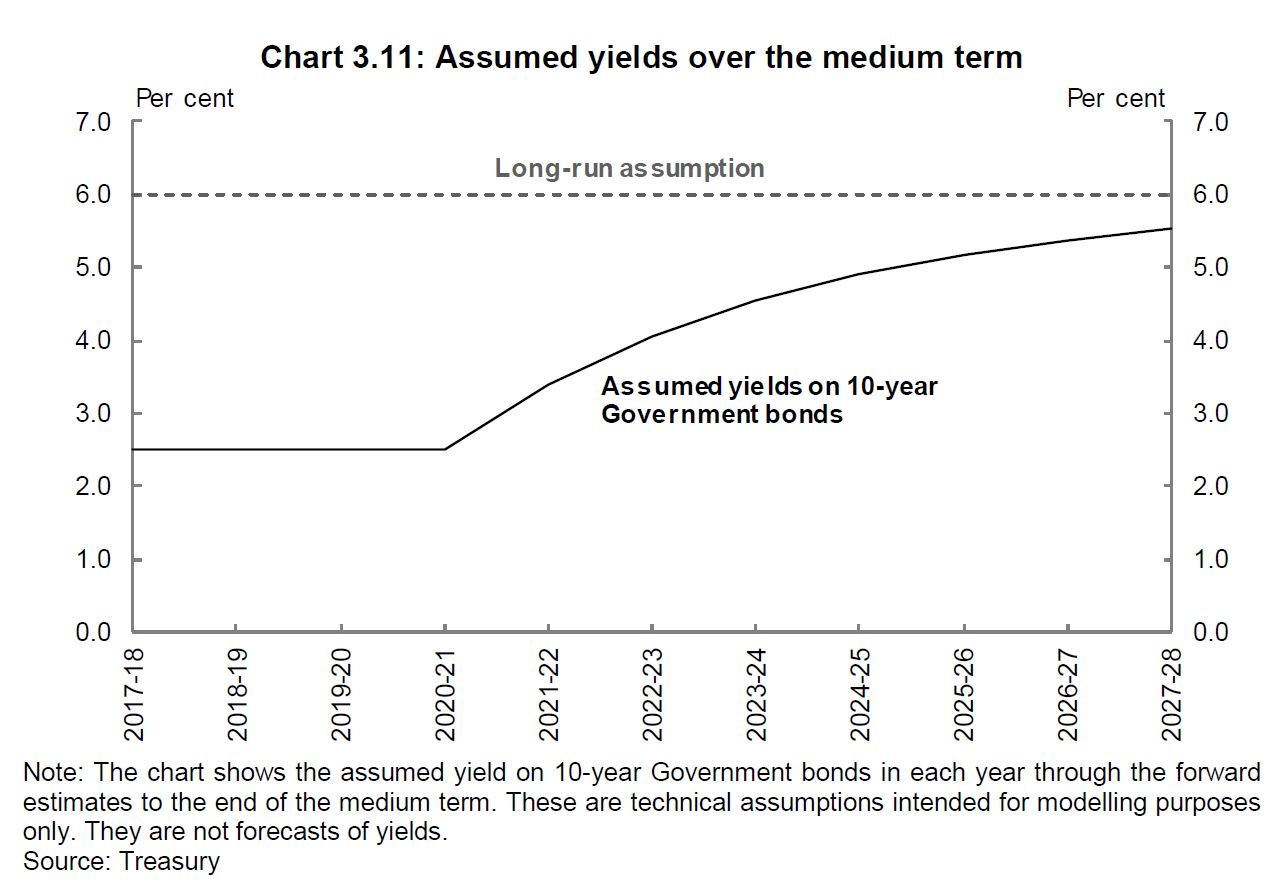

Finally, the assumed Treasury yields are set quite low, for modeling purposes. Rising rates in the USA and elsewhere may lift rates faster.