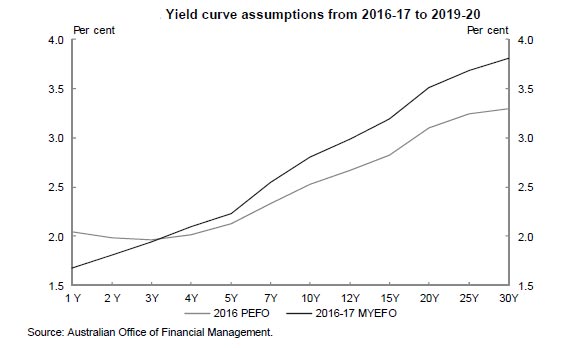

The MYEFO was released today. In essence, it has quite an optimistic tint, but fundamentally growth is too weak, so incomes, business investment and tax takes will be depressed. Whilst there is some chance of a “free-kick” from some commodity prices, the outlook is not great, and net government debt has yet to peak. The cost of debt will rise as shows by the yield curve assumption which has lifted compared with 2016 PEFO.

“The Government’s interest payments and expense over the forward estimates mostly relate to the cost of servicing the stock of Commonwealth Government Securities (CGS) on issue, and are expected to increase over the forward estimates as a result of the projected rise in CGS on issue”.

“The Government’s interest payments and expense over the forward estimates mostly relate to the cost of servicing the stock of Commonwealth Government Securities (CGS) on issue, and are expected to increase over the forward estimates as a result of the projected rise in CGS on issue”.

The key question is how will this translated to the mortgage rate, which we know will be rising through 2017, as global capital markets reprice yields post the Trump election? We think this will help to lift rates higher still.

The big risk is a AAA downgrade. Such a move would lift the costs of funding for the banks, and this would need to be passed on to consumers and small business customers. The probability has firmed for a downgrade, and so the expectation must be that mortgage rates will rise further and faster than previously expected. We still expect rates on average to be 50 basis points higher this time next year. Our mortgage stress analysis shows that some households are already under the gun.

Whilst there is certainly a chance the RBA may want to cut rates to assist next year, we still think this is unlikely, given the housing boom in the eastern states and the clear limitations of monetary policy when rates are this low. In any case the cash rates and mortgage rates have become decoupled.

Here is the ABC’s MYEFO summary:

- Budget deficit this financial year has shrunk by $600 million to $36.5 billion

- Deficits over the four year forward estimates have grown by more than $10 billion

- The Government is still projecting a return to surplus in financial year 2020-21

- Net debt as a proportion of economic output will peak at 19 per cent in 2018-19

- Real economic growth estimates have been revised down slightly

- MYEFO says “commodity prices remain a key uncertainty”

- Estimated tax receipts are down by $3.7 billion since the pre-election budget update

- Tax receipts are predicted to be $30.7 billion lower over four years

- Tax receipts are down despite recent bounces in key commodity prices

- Sluggish wage growth and and non-mining company profits are dragging down tax receipts

- The Government has confirmed it is scrapping the Green Army program, saving $224 million

- MYEFO reveals extra staff for crossbenchers and other politicians will cost $35.8 million over four years

- The Government is closing the Asset Recycling Fund

- A Commonwealth penalty unit will rise from $180 to $210

More broadly, the MYEFO says:

Household consumption is expected to continue to grow at a moderate rate, supported by further employment growth and low interest rates. The household saving rate is expected to continue to decline over the forecast period as consumption growth outpaces the modest growth in disposable incomes.

Dwelling investment is forecast to grow by 4½ per cent in 2016-17 before easing to ½ per cent in 2017-18, as the current pipeline of construction — which is evident in the data on building approvals and commencements — is completed.

Business investment is forecast to fall by 6 per cent in 2016-17 and to be flat in 2017-18. This reflects further large forecast falls for mining investment of 21 per cent in 2016-17 and 12 per cent in 2017-18. The impact of this decline in mining investment on the economy is expected to diminish over the forecast period.

Employment growth is expected to be supported by continued economic growth and subdued wage growth. Employment is forecast to grow at a slightly more moderate pace of 1¼ per cent through the year to the June quarter 2017, reflecting more subdued employment growth over recent months and slower output growth. Following the recent highs, which saw almost 300,000 jobs created in 2015, employment growth has been slower in 2016. Employment growth is expected to increase to 1½ per cent through the year to the June quarter 2018 as economic growth strengthens.

The unemployment rate has declined since its recent peak of 6.3 per cent in July 2015. The unemployment rate is forecast to remain around 5½ per cent in the June quarters of 2017 and 2018. While the unemployment rate has fallen, the underemployment rate has remained elevated. These developments suggest that spare capacity remains in the labour market. The forecast for the participation rate has been revised down since the 2016 PEFO and it is expected to be 64½ per cent in the June quarters of 2017 and 2018.

Consumer price inflation is low reflecting subdued wage growth and other factors such as heightened competition in the retail sector, slower growth in rents and lower import and petrol prices. There is also a subdued inflationary environment globally.

Consumer prices are expected to grow by 1¾ per cent through the year to the June quarter 2017, before picking up to 2 per cent through the year to the June quarter 2018. This is lower than forecast at the 2016 PEFO.Wage growth has also softened since the 2016 PEFO, in line with weaker consumer price outcomes and other factors such as spare capacity in the labour market. As with consumer prices, wage growth is expected to increase gradually over the forecast period to be 2¼ per cent through the year to the June quarter 2017

and 2½ per cent through the year to the June quarter 2018.Nominal GDP growth is forecast to be 5¾ per cent in 2016-17 and 3¾ per cent in 2017-18. The forecast for 2016-17 is stronger than the 2016 PEFO forecast, with higher commodity prices providing an offset to weaker wage growth and domestic price

pressures.