NAB has released their 2017 Half results. They reported cash earnings (“cash earnings” is calculated by excluding discontinued operations and certain other items) of $3.29 billion, up 2.3% compared to March 2016 half year.

There are some positives, with stronger contributions from markets and treasury (but of course less easy to replicate next time), net interest margin higher in the business sector, but lower momentum and margins in the home lending sector, rising delinquencies and higher provisions for commercial real estate. Capital ratios are strong, and funding well managed. Benefits from technology investments are flowing.

On a statutory basis, net profit attributable to the owners of NAB was $2.55 billion compared to a loss of $1.74 billion for the March 2016 half year. The improved result primarily reflects reduced losses from discontinued operations. Excluding discontinued operations, statutory net profit decreased 11.4%. The main difference between statutory and cash earnings relates to the effects of fair value and hedge ineffectiveness, and discontinued operations.

Revenue increased 1.8% benefitting from growth in lending, improved fee collection and stronger trading income.

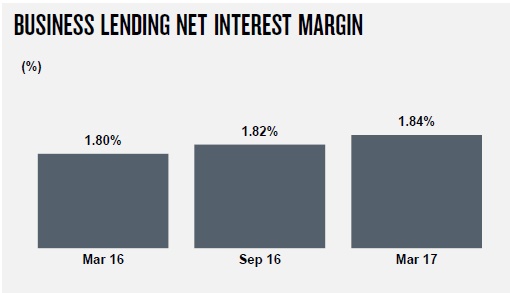

Group net interest margin (NIM) declined 11 basis points but excluding Markets and Treasury was down 4 basis points. Compared to the September 2016 half year NIM was stable at 1.82%.

Expenses rose 0.8% reflecting higher personnel costs including redundancy charges, and increased technology depreciation and amortisation charges, partly offset by productivity savings.

Expenses rose 0.8% reflecting higher personnel costs including redundancy charges, and increased technology depreciation and amortisation charges, partly offset by productivity savings.

The total charge for Bad and Doubtful Debts (B&DDs) was $394 million, up $19 million or 5.1%. The charge this period includes an increase in collective provision (CP) overlays of $89 million mainly for potential risks relating to the commercial real estate (CRE) portfolio. The Group’s total CP overlays for CRE, agriculture, mining and mining related sectors now stand at $291 million.

The ratio of Group 90+ days past due and gross impaired assets to gross loans and acceptances of 0.85% at 31 March 2017 was stable compared to 30 September 2016.

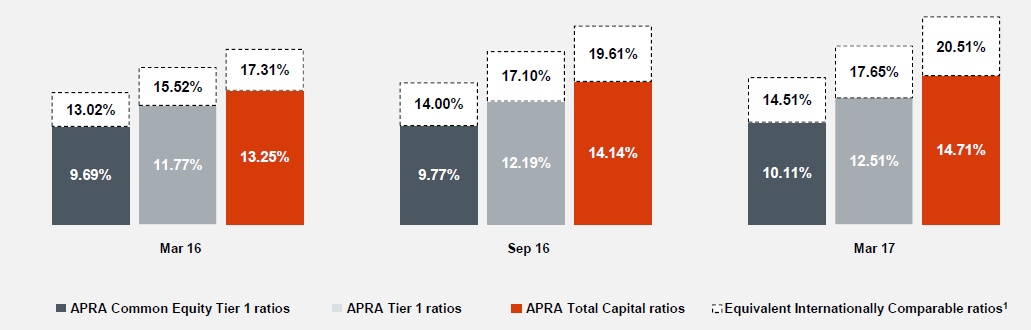

The Group’s Common Equity Tier 1 (CET1) ratio was 10.1% as at 31 March 2017, an increase of 34 basis points from 30 September 2016. The Group’s CET1 target ratio remains between 8.75% – 9.25%. On an internationally comparable basis3 the CET1 ratio increased 51 basis points from 30 September 2016 to 14.5%.

The interim dividend is 99 cents per share fully franked, unchanged from the 2016 interim and final dividends.

The interim dividend is 99 cents per share fully franked, unchanged from the 2016 interim and final dividends.

The Group says it maintains a well diversified funding profile and raised $18.8 billion of term wholesale funding in the March 2017 half year across a range of markets. The weighted average term to maturity of the funds raised by the Group over the March 2017 half year was 5.4 years. The net stable funding ratio (NSFR) was 108% at 31 March 2017.

The Group’s leverage ratio as at 31 March 2017 was 5.5% on an APRA basis and 5.9% on an internationally comparable basis.

The Group’s quarterly average liquidity coverage ratio as at 31 March 2017 was 122%.

Business & Private Banking grew cash earnings 2.5% to $1,368 million reflecting sound revenue growth and tight cost management, partly offset by higher B&DD charges. NIM improved and lending growth in specialised businesses such as Health and Agribusiness was strong.

Consumer Banking & Wealth cash earnings were stable at $764 million impacted by higher funding costs, increased competition in home lending, and reduced Wealth income. NIM stabilised compared to the September 2016 half year and more recent home lending market share trends are improving.

Consumer Banking & Wealth cash earnings were stable at $764 million impacted by higher funding costs, increased competition in home lending, and reduced Wealth income. NIM stabilised compared to the September 2016 half year and more recent home lending market share trends are improving.

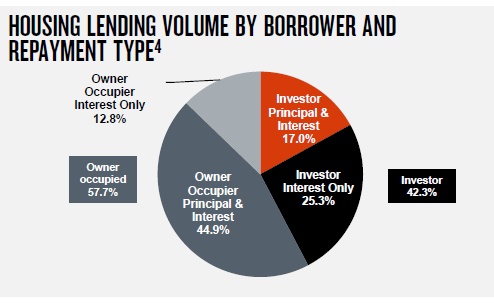

Looking at home lending, 42.3% are investor loans, and more than half of these are interest only.

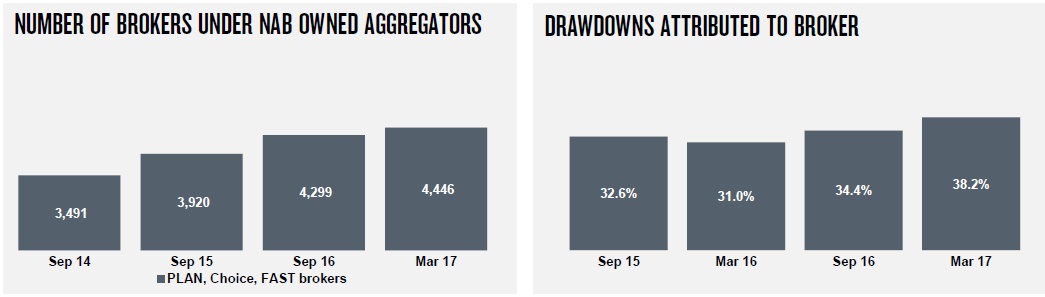

Drawdowns from brokers continued to rise, as did the number of brokers under NAB owned aggregators.

Drawdowns from brokers continued to rise, as did the number of brokers under NAB owned aggregators.

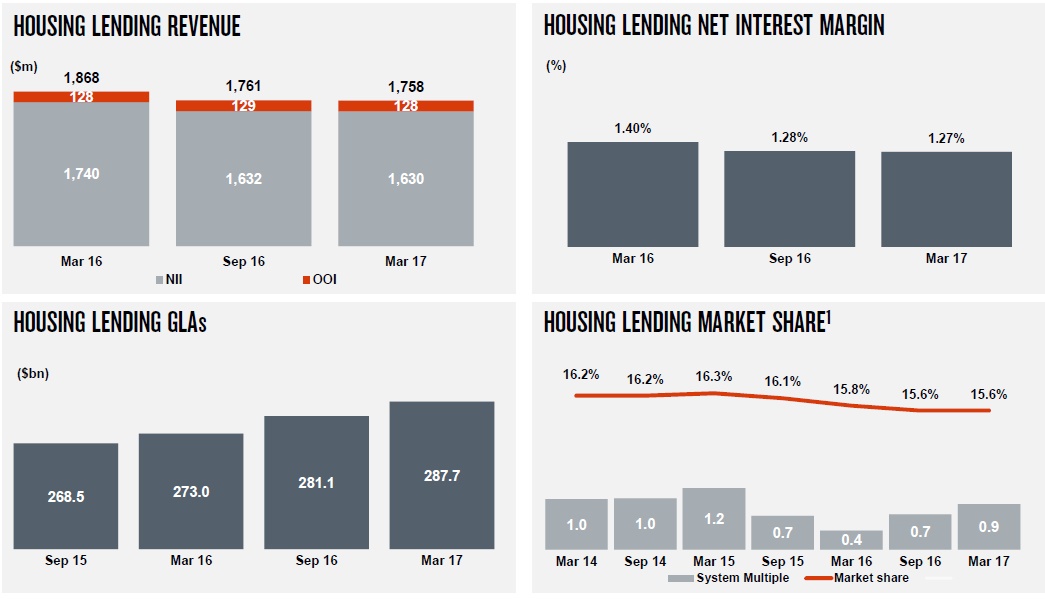

Housing net interest margin fell, as did home lending revenue. They are growing below system.

Housing net interest margin fell, as did home lending revenue. They are growing below system.

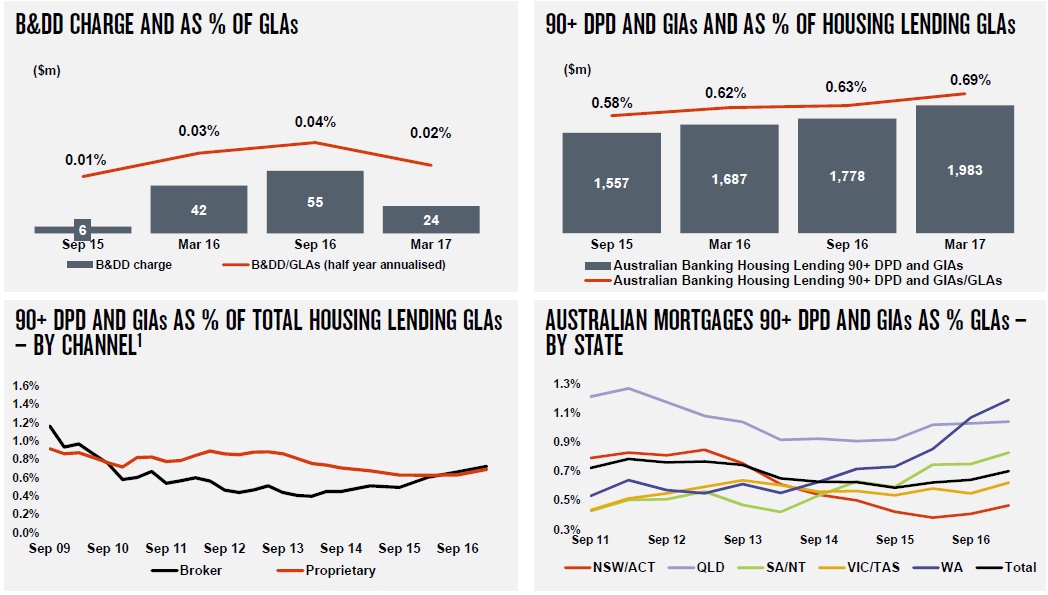

Delinquencies are rising across the portfolio. They have limited exposure to commercial real estate (but provisions are up), and to higher risk mining post codes.

Delinquencies are rising across the portfolio. They have limited exposure to commercial real estate (but provisions are up), and to higher risk mining post codes.

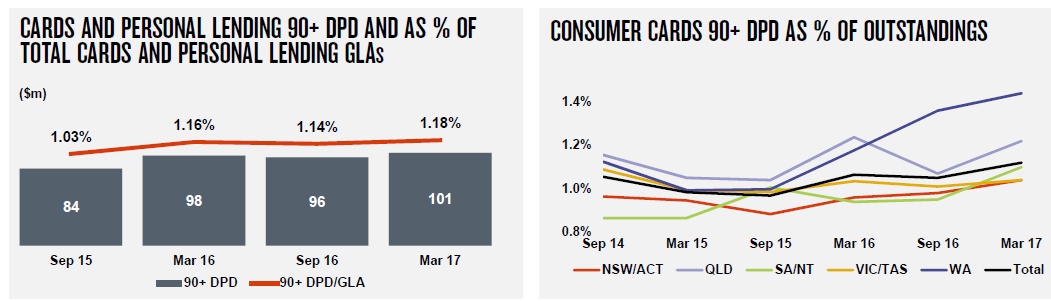

Card and personal lending delinquencies are also rising.

Card and personal lending delinquencies are also rising.

Corporate & Institutional Banking (CIB) cash earnings rose 17.9% to $791 million. This was a strong result underpinned by a disciplined focus on returns. Over the year to March 2017 CIB delivered revenue growth, lower costs, lower B&DD charges and a $15 billion reduction in risk weighted assets.

Corporate & Institutional Banking (CIB) cash earnings rose 17.9% to $791 million. This was a strong result underpinned by a disciplined focus on returns. Over the year to March 2017 CIB delivered revenue growth, lower costs, lower B&DD charges and a $15 billion reduction in risk weighted assets.

NZ Banking local currency cash earnings increased 10.4% to NZ$455 million. Improved economic conditions, and in particular a better outlook for the dairy sector, (provisions down ~90% compared with prior half) have resulted in lower B&DD charges. Strong growth in business and home lending reflect successful expansion in priority segments. NZ net interest margin fell.

NAB Group CEO Andrew Thorburn said:

NAB Group CEO Andrew Thorburn said:

“The rollout of the Net Promoter Score (NPS) system to all our front line teams is an important tool that helps bankers take greater ownership of the customer experience. Every branch, contact centre and business banking centre now receives localised weekly scores and real time customer feedback resulting in improved customer outcomes on our front line.

“Technology underpins our ability to serve customers better by becoming easier and simpler to deal with. Over the half we have made further progress embedding the Personal Banking Origination Platform (PBOP) into our network. Approximately 55% of customers are now receiving unconditional home loan approval within 5 days compared to 7% at September 2016.

“Disciplines in place to reshape our business, including use of automation and meeting more of our customers’ needs digitally, are delivering efficiency benefits. In 1H17 we achieved $102 million of productivity savings against an annual target of greater than $200 million. We remain confident of achieving positive ‘jaws’ over the full year as a number of initiatives gain further traction during the second half of 2017”.