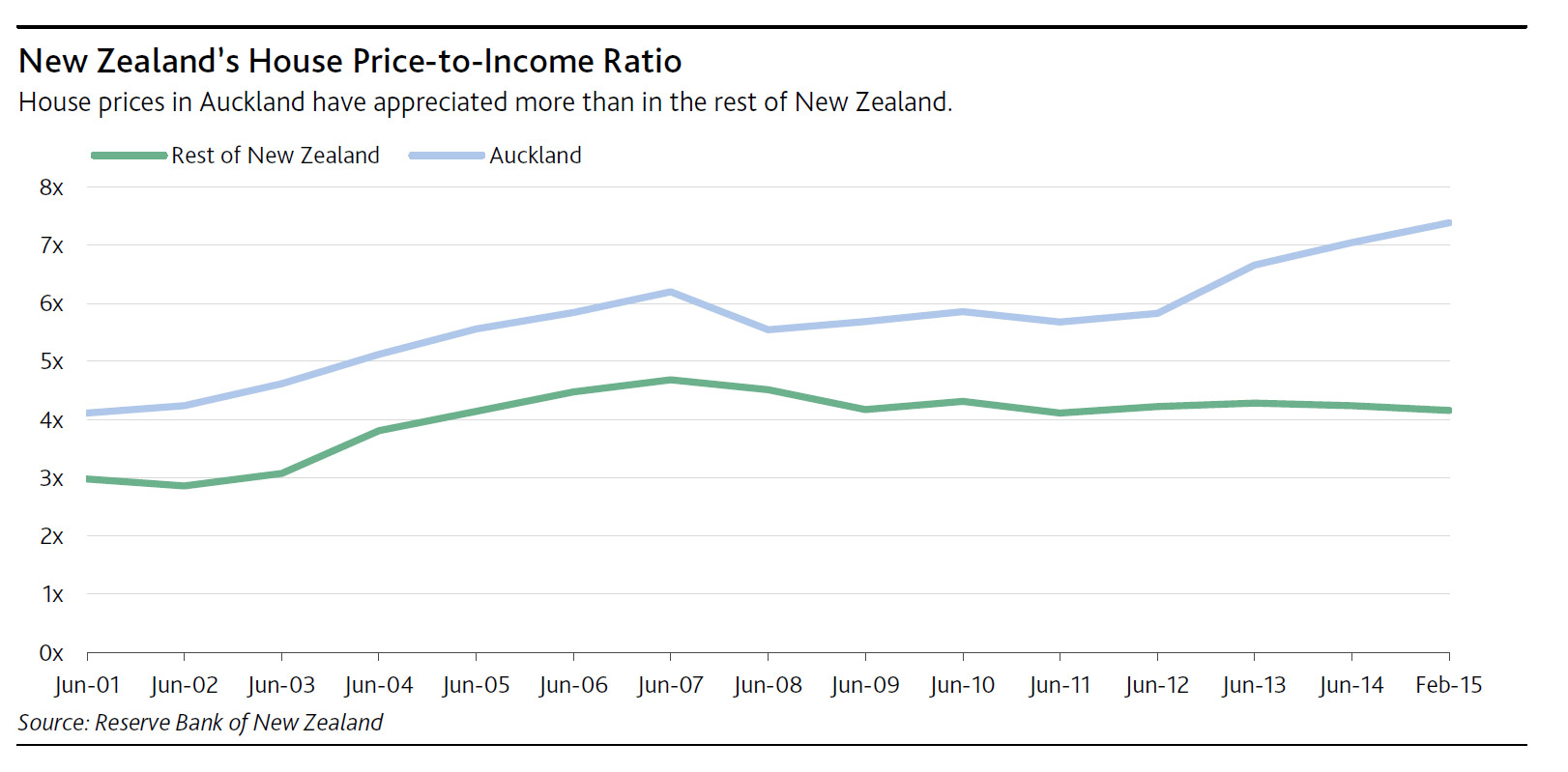

Last Wednesday, the Reserve Bank of New Zealand (RBNZ) announced that starting 1 October 2015 bank lending to home investors in Auckland, New Zealand, will be restricted to mortgages with loan-to-value ratios (LTVs) of less than 70%. The RBNZ also said it was raising the percentage of residential mortgage loans that can be originated outside of Auckland with LTVs of 80% or higher to 15% of all mortgage loans from 10%. These measures are credit positive for New Zealand’s banks because they will reduce banks’ exposure to riskier mortgage loans in Auckland, where house prices are at historical highs, having risen 14.6% in the 12 months to March 2015.

Moody’s says these steps would particularly benefit New Zealand’s four major banks, ASB Bank Limited (Aa3/Aa3 stable, a2 review for downgrade), ANZ Bank New Zealand Limited (Aa3/Aa3 stable, a3), Bank of New Zealand (Aa3/Aa3 stable, a3) and Westpac New Zealand Limited (Aa3/Aa3 stable, a3). These banks held approximately 86% of total system mortgages as of 31 December 2014. Additionally, Auckland, New Zealand’s largest city, constitutes the largest market for these banks, and the RBNZ reports that around 40% of mortgage originations in Auckland are to investors.

The introduction of an LTV limit on property-investor lending in Auckland will reduce the risk of recently originated mortgages experiencing negative equity, where the size of the loan exceeds the value of the property. Both house prices and household indebtedness in Auckland are at historical highs creating a sensitivity to increases in unemployment and interest rates. Although LTV restrictions are likely to dampen house price growth in Auckland, we expect the effect to bemarginal owing to supply shortages and the official cash rate, which the RBNZ sets to meet inflation targetsand remains accommodative by historical standards, continuing to support price gains. However, reducingbank exposures to high-LTV loans that are more exposed to a house price correction would benefit banks.

The LTV restrictions would not apply to loans to construct new residential properties, given the RBNZ’s focus on alleviating Auckland’s housing shortage. Although the new 15% cap on high-LTV loans outside Auckland will allow banks to lend more at higher LTVs, price growth outside of Auckland has been relatively subdued. By responding to current housing market developments and loosening restrictions, the RBNZ is making housing finance more accessible in areas of New Zealand where there are fewer risks of stimulating excessive price speculation.

The LTV restrictions would not apply to loans to construct new residential properties, given the RBNZ’s focus on alleviating Auckland’s housing shortage. Although the new 15% cap on high-LTV loans outside Auckland will allow banks to lend more at higher LTVs, price growth outside of Auckland has been relatively subdued. By responding to current housing market developments and loosening restrictions, the RBNZ is making housing finance more accessible in areas of New Zealand where there are fewer risks of stimulating excessive price speculation.

The proposals are the RBNZ’s latest in a series of steps aimed at reducing excess leverage in the financial system and reducing the threat of asset bubbles. In September 2013, the RBNZ raised the capital requirements for high-LTV lending and in October 2013 imposed a 10% cap on high-LTV loans. In March 2015, the RBNZ released a consultation paper indicating that banks would likely need to hold more capital against investor loans than against owner-occupied mortgages. The RBNZ intends to release a consultation paper later this month outlining its most recent announcement.