Moody’s says on Thursday, the Norwegian government increased the country’s countercyclical capital buffer to 2.0% common equity Tier 1 (CET1) capital from 1.5%, effective 31 December 2017. In addition, last Wednesday, the Norwegian Ministry of Finance adopted a new regulation on residential mortgage loans.

Norway has a similar debt servicing ratio to Australia, according to recent data from BIS. So the steps they are taking to control their housing market are highly relevant to us. RBA please note.

Moody’s say this action is credit positive because it will press Norwegian banks to further strengthen their capital buffers, thereby protecting bondholders against potential shocks from a collapse in housing prices.

The requirement applies to banks, financial institutions and parent companies of financial non-insurance companies. Since Norway recognises the countercyclical buffers of other countries, the actual increase in capital requirements may be smaller than 50 basis points for banks with large foreign operations. For example, we estimate that the effect on DNB Bank ASA (Aa2/Aa2 negative, a37) would be an increase in its CET1 capital requirement of 30-40 basis points. DNB reported a CET1 ratio of 15.0% at the end of September 2016 and will have a 14.7% CET1 capital requirement at the end of 2016, which we estimate will increase to 15.0%-15.1% at the end of 2017. We expect DNB and most other banks to target a management buffer of around 100 basis points on top of the capital requirements.

We believe that most Norwegian banks are already well on their way to meeting these requirements, and therefore we do not expect significant capital raising among banks. However, the regulation is credit positive because it will discourage banks from releasing capital over the next 12-18 months for such things as dividend increases.

The increase follows a recommendation by the Norwegian central bank that the government raise the countercyclical capital buffer for Norwegian banks in response to the build-up of financial imbalances stemming from a growing credit-to-GDP ratio for the mainland economy, in excess of the long-term trend, and high house price inflation.

According to Statistics Norway, Norwegian household credit levels at the end of September were up 6.2% year on year. During the same period, residential real estate prices rose 8.0%, and by 17.9% in the area around the capital city of Oslo, outpacing nominal mainland GDP growth of 3.3% and inflation (adjusted for tax changes and excluding energy products) of 2.9% during the period. Norwegian banks’ loan books (excluding DNB), dominated by household mortgages, rose approximately 11% during the period, exposing Norwegian banks to a market-price correction if Norwegian home prices fall. Such a scenario would have negative repercussions on asset quality, and potentially capitalisation, which would negatively affect banks.

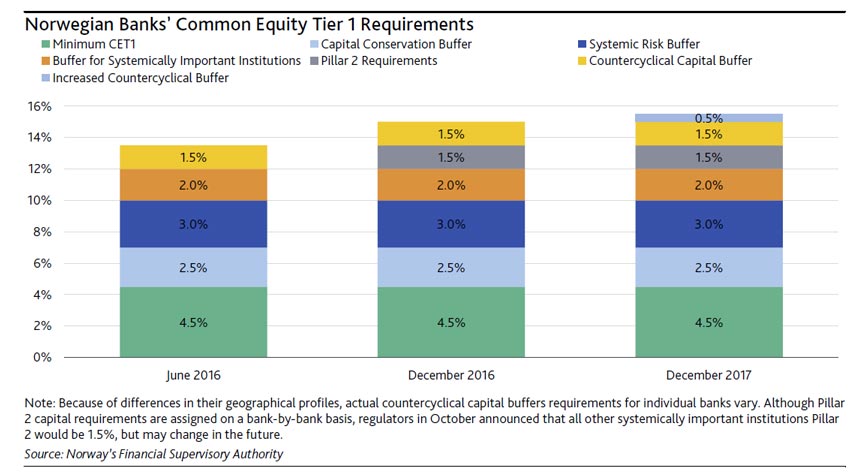

As shown in the exhibit above, the current CET1 requirement for Norway’s other systemically important institutions’ (O-SIIs) is 13.5%, rising to 15% at the end of December 2016 (although there are some differences based on geographical profile when applying the countercyclical buffer). At the end of December 2017, following the increase in the countercyclical buffer, the CET1 requirement will rise to 15.5% for Norway’s O-SIIs and to 12% plus institution-specific Pillar 2 requirement for non-systemically important institutions. The Norwegian central bank also warned that if the financial imbalances build up further, the buffer may increase.

In addition, last Wednesday, the Norwegian Ministry of Finance adopted a new regulation on residential mortgage loans that, as per the Norwegian Financial Services Authority’s (FSA) recommendation, lowers the maximum loan-to-value (LTV) ratio for home equity credit lines to 60% from 70%. This reduction is credit positive for banks because it will improve mortgage underwriting standards by containing borrower leverage. The new regulation takes effect on 1 January 2017 and will be in force until 30 June 2018.

Lenders will be able to maintain their underwriting standards by selecting customers with higher debt-servicing capacity. In addition to the requirement for home equity credit lines, the Ministry of Finance has kept the cap on the LTV ratio on residential mortgage loans unchanged at 85%, but, in line with the FSA’s recommendation, it now requires banks to assume a 5% interest rate increase when assessing a borrower’s debt-servicing capacity. The provision also limits borrowers’ aggregate debt to 5x gross annual income.

The Norwegian government retains the provision that allows part of a lender’s approved loans that do not meet all the requirements in the regulation. Outside Norway’s capital city of Oslo this quota is retained at 10% of the volume of a lender’s approved loans, whereas in Oslo the quota falls to 8%. Moreover, in Oslo the new regulation caps the LTV ratio on secondary homes at 60%, according to the Ministry of Finance.

We expect these measures to contain borrowers’ leverage and to contribute to containing speculation in some areas that we identified as more vulnerable in our recent Banking System Outlook on Norway. House prices in oil-focused regions of Norway, such as Stavanger, have fallen after many years of strong price appreciation, while in large metropolitan areas they have continued to increase, driven by Norway’s low interest rates and government stimulus such as lower taxes on individuals and corporates