The Financial Markets Authority (FMA) and Reserve Bank of New Zealand (RBNZ) have completed their joint review of 16 New Zealand life insurers. This review follows the regulators’ bank review published in November 2018.

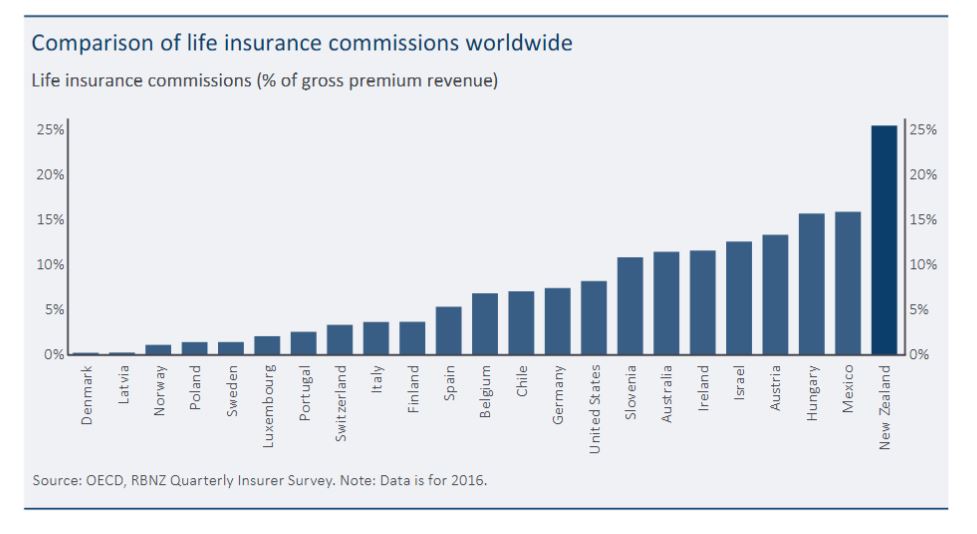

The findings appear to mirror the Australian Royal Commission, with a focus on shareholders rather than customers – sounds familiar? In addition commissions are extremely high in New Zealand.

Rob Everett, FMA Chief Executive said: “Overall the report shows the life insurance sector in a poor light. Life insurers have been complacent about considering conduct risk, too slow to make changes following previous FMA reviews and not sufficiently focused on developing a culture that balances the interests of shareholders with those of customers.”

The regulators found extensive weaknesses in life insurers’ systems and controls, with weak governance and management of conduct risks across the sector and a lack of focus on good customer outcomes.

Adrian Orr, Reserve Bank Governor said: “The industry must act urgently and undergo major change to address these weaknesses, as their services are vulnerable to misconduct and the escalation of issues that have been seen in other countries. Public trust in life insurers could be eroded unless boards and senior management transform their approach to conduct risk and achieve a customer-focused culture. Ultimately insurers need to take responsibility for whether customers are experiencing good outcomes from their products, regardless of how they are sold.”

Other key findings:

- Limited evidence of products being designed and sold with good customer outcomes in mind.

- Some insurers did little or nothing to assess a product’s ongoing suitability for customers.

- Sales incentives structures risk sales being prioritised over good customer outcomes.

- Where sales were through an intermediary, there was a serious lack of insurer oversight and responsibility for the sales and advice, and customer outcomes.

- Remediation of conduct issues is generally very poor, with insurers slow to respond to issues and in some cases not sufficiently remediating them.

The review did not find widespread cases of misconduct on the part of life insurance companies. However, there were several instances of poor conduct. There were also a small number of cases of potential misconduct (i.e.: breaches of the law) that are now subject to investigations by the appropriate regulator.

Some of the issues and themes are similar to those highlighted in the Australia Royal Commission, albeit on a smaller scale. The FMA and RBNZ are not confident that insurers themselves are aware of all the current issues. This creates a serious risk of further conduct issues arising.

Next steps

All 16 life insurers will receive individual feedback. By 30 June 2019, each insurer will need to report back to the regulators. They will need to provide an action plan that the regulators will review, including how they will address incentives based on sales volumes for internal staff and commissions for intermediaries. Regular reporting on progress and implementation will be required.

Concerns for consumers

Purchasing life insurance is one of the most important financial decisions people will make. Customers should be able to have confidence their insurance will do what the insurance company or their financial adviser has told them. Many customers do experience the benefits of their insurance policies every year.

A positive finding in the report showed that, in general, frontline claims teams were focused on good outcomes with a strong desire to do the right thing for their customers.

The purpose of the thematic review and the report’s recommendations are to ensure the industry responds with urgency to the issues identified.

Further information and guidance for consumers can be found on the FMA website, here fma.govt.nz/investors/life/

Regulatory issues

Insurer conduct is currently only regulated indirectly through the FMA’s regulation of financial advice, which is generally provided by intermediaries. No one regulator has oversight of insurers’ and intermediaries’ conduct over the entire insurance policy lifecycle.

The report sets out some areas where the regulators recommend that the Government consider addressing regulatory gaps, similar to those put forward in our review of banks. The regulators acknowledge further policy work will be required and that any additional regulation will need to drive better outcomes for customers.