The NZ Reserve Bank today left the Official Cash Rate (OCR) unchanged at 1.75 percent.

Core inflation is running 1.5-2%, and they believe they are on track to be within their 2-3% target range ahead. Wage growth remains sluggish, despite high participation rates.

The macroprudential policies (loan-to-value based) they have implemented have trimmed house price growth significantly, (nationwide monthly house price inflation has averaged 0.1 percent over the past five months, compared to 2.1 percent in the five months prior), although they said they also believe housing supply is important. The number of house sales nationwide has fallen by about 20 percent since its peak in April 2016. NZ regulators deserve recognition for their integrated and successfully implemented policies.

The steepening in wholesale rates has flowed through to rising fixed-term mortgage rates, with the 2-year mortgage rate rising by 45 basis points since their November Statement. They are also doing significant work on debt-to-income ratios, but have not yet implemented measures on this basis. The NZ Government wants to see a cost benefit analysis of these measures before they are implemented.

The recovery in commodity prices and more positive business and consumer sentiment in advanced economies have improved the global outlook. However, major challenges remain with on-going surplus capacity in the global economy and rising geo-political uncertainty.

Global headline inflation has increased, partly due to rising commodity prices. Global long-term interest rates have increased. Monetary policy is expected to remain stimulatory, but less so going forward, particularly in the US.

New Zealand’s financial conditions have firmed with long-term interest rates rising and continued upward pressure on the New Zealand dollar exchange rate. The exchange rate remains higher than is sustainable for balanced growth and, together with low global inflation, continues to generate negative inflation in the tradables sector. A decline in the exchange rate is needed.

Economic growth in New Zealand has increased as expected and is steadily drawing on spare resources. The outlook remains positive, supported by ongoing accommodative monetary policy, strong population growth, increased household spending and rising construction activity. Dairy prices have recovered in recent months but uncertainty remains around future outcomes.

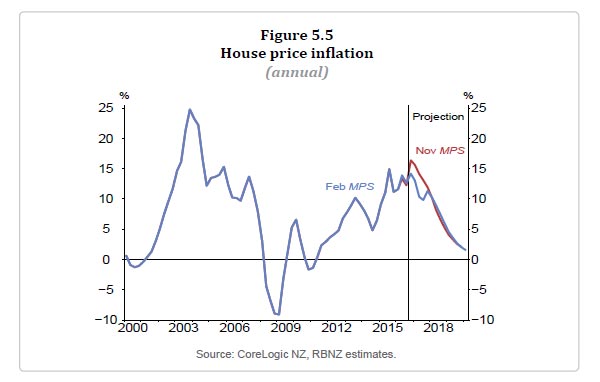

Recent moderation in house price inflation is welcome, and in part reflects loan-to-value ratio restrictions and higher mortgage rates. It is uncertain whether this moderation will be sustained given the continued imbalance between supply and demand.

Headline inflation has returned to the target band as past declines in oil prices dropped out of the annual calculation. Inflation is expected to return to the midpoint of the target band gradually, reflecting the strength of the domestic economy and despite persistent negative tradables inflation. Longer-term inflation expectations remain well-anchored at around 2 percent.

Monetary policy will remain accommodative for a considerable period. Numerous uncertainties remain, particularly in respect of the international outlook, and policy may need to adjust accordingly.