The latest OECD Report – 2017 Economic Survey of Australia says whilst Australia’s economy has enjoyed considerable success in recent decades, the economy shares the global risk of a “low-growth trap”.

Living standards and well-being are generally high, though challenges remain in gender gaps and in greenhouse-gas emissions, and further challenges arise from population ageing.

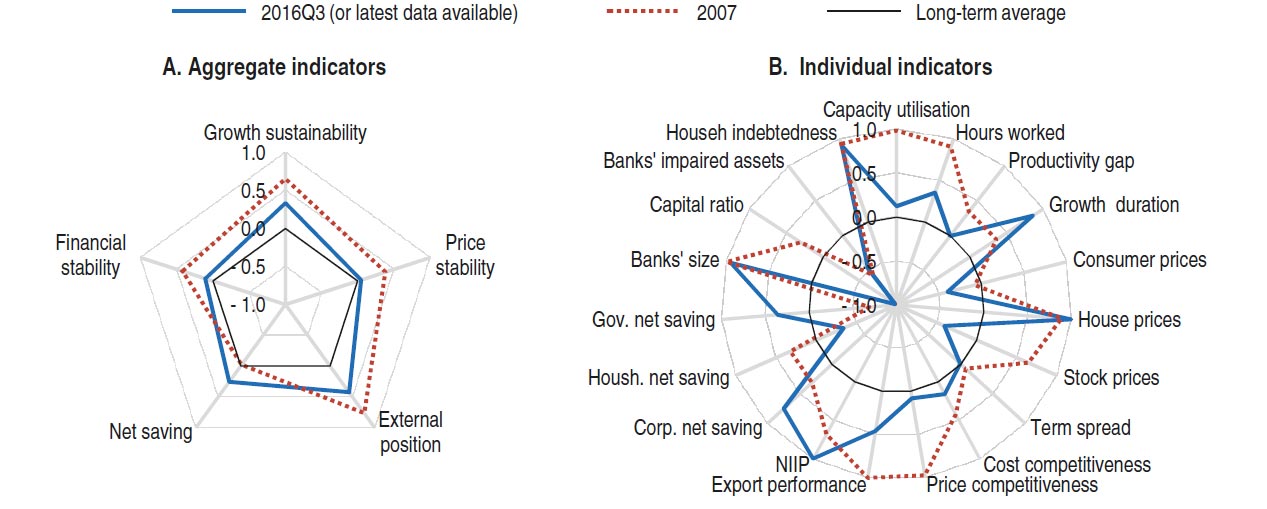

Low interest rates have supported aggregate demand but are also ramping up risk-taking by investors and driving house prices and mortgage lending to historical highs.

A fall in house prices and or demand could have significant macroeconomic implications. Specifically, the market may not ease gently but develop into a rout on prices and demand with significant macroeconomic implications.

Macrofinancial indicators underline the threat from the housing market, with house prices and related indicators (house indebtedness, bank size), pointing to continued vulnerability. Any impact will most likely be through aggregate demand than financial instability.

Macrofinancial indicators underline the threat from the housing market, with house prices and related indicators (house indebtedness, bank size), pointing to continued vulnerability. Any impact will most likely be through aggregate demand than financial instability.

They advocate tight macroprudential measures, improved housing supply, and reducing banks’ implicit guarantees by developing a loss absorbing and recapitalisation framework.

They support a cut in company tax, and an expansion of the GST, switching from transaction taxes (like stamp duty) to land taxes.

They say the economy is now rebalancing following the end of the commodity boom, supported by macroeconomic policies and currency depreciation. The strengthening non-mining sector is projected to support output growth of around 3% in 2018 and spur further reduction in the unemployment rate.

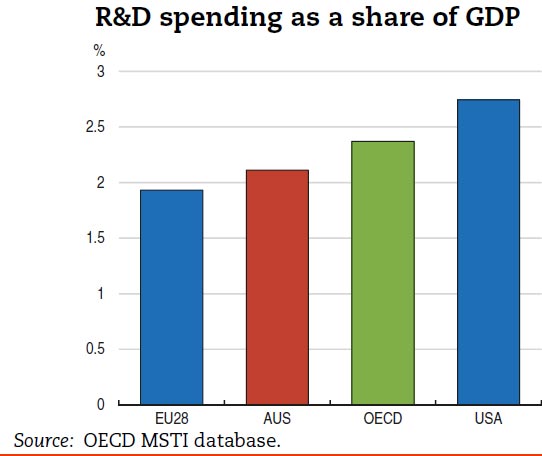

Improving competition and other framework conditions that influence the absorption and development of innovation are key for restoring productivity growth.

Improving competition and other framework conditions that influence the absorption and development of innovation are key for restoring productivity growth.

Innovation requires labour and capital markets that facilitate new business models. Productivity growth could be boosted through stronger collaboration between business and research sectors in R&D activity.

Australia’s adjustment to the end of the commodity boom has not been painless. Unemployment has risen, and there are increasing concerns about inequality.

Australia’s adjustment to the end of the commodity boom has not been painless. Unemployment has risen, and there are increasing concerns about inequality.

In addition, large socioeconomic gaps between Australia’s indigenous community and the rest of the population remain. Developing innovation-related skills will be important for the underprivileged and those displaced by economic restructuring, and can help reduce gender wage gaps.

Externally, Australia, as always, is exposed to the vagaries of global commodity markets and this might include a renewed plunge in prices (or, positively, a strong resurgence). Australia’s iron ore production is among the lowest cost in the world and therefore comparatively insulated from such developments, however its coal sector is relatively more exposed as its production is distributed across the cost curve. Interaction of downside scenarios is likely to exacerbate the negative macroeconomic outcomes.

Externally, Australia, as always, is exposed to the vagaries of global commodity markets and this might include a renewed plunge in prices (or, positively, a strong resurgence). Australia’s iron ore production is among the lowest cost in the world and therefore comparatively insulated from such developments, however its coal sector is relatively more exposed as its production is distributed across the cost curve. Interaction of downside scenarios is likely to exacerbate the negative macroeconomic outcomes.

For instance, a negative external shock could lift unemployment sharply which would result in significant fall in consumption and rising mortgage stress and falling house prices. The economy is well positioned to handle shocks. The speed and strength of the rebalancing processes in response to the end of the commodity boom auger well for the economy’s shock-absorbing capacity. In addition, Australia has more reserve capacity for monetary and fiscal stimulus than many other OECD economies.

The slideshow is available here.

One thought on “OECD Paints A Sanguine Picture Of The Australian Economy, Includes Housing Risks”