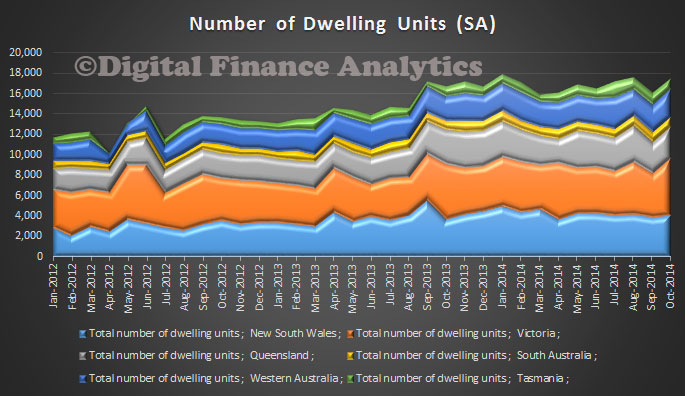

The ABS released their Building Approvals Data to October 2014. The trend estimate for total dwellings approved rose 0.6% in October and has risen for five months whilst the seasonally adjusted estimate for total dwellings approved rose 11.4% in October following a fall of 11.2% in the previous month.

The trend estimate for private sector houses approved was flat in October whilst the seasonally adjusted estimate for private sector houses fell 0.2% in October and has fallen for two months. The trend estimate for private sector dwellings excluding houses rose 1.6% in October and has risen for five months whilst the seasonally adjusted estimate for private sector dwellings excluding houses rose 31.3% in October following a fall of 24.5% in the previous month. The volatile unit sector is of course influenced by high demand for investment property.

The trend estimate for private sector houses approved was flat in October whilst the seasonally adjusted estimate for private sector houses fell 0.2% in October and has fallen for two months. The trend estimate for private sector dwellings excluding houses rose 1.6% in October and has risen for five months whilst the seasonally adjusted estimate for private sector dwellings excluding houses rose 31.3% in October following a fall of 24.5% in the previous month. The volatile unit sector is of course influenced by high demand for investment property.

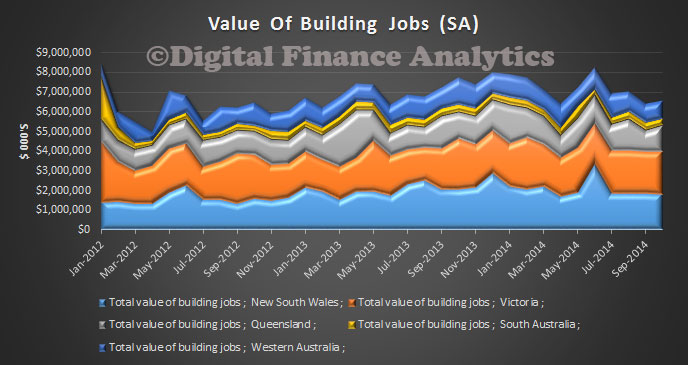

The trend estimate of the value of total building approved fell 1.2% in October and has fallen for 11 months whilst the value of residential building fell 1.1% and has fallen for four months. The value of non-residential building fell 1.3% and has fallen for 11 months. The seasonally adjusted estimate of the value of total building approved rose 0.2% in October following a fall of 10.0% in the previous month. The value of residential building rose 8.0% following a fall of 16.3% in the previous month. The value of non-residential building fell 14.1% following a rise of 4.7% in the previous month.

The trend estimate of the value of total building approved fell 1.2% in October and has fallen for 11 months whilst the value of residential building fell 1.1% and has fallen for four months. The value of non-residential building fell 1.3% and has fallen for 11 months. The seasonally adjusted estimate of the value of total building approved rose 0.2% in October following a fall of 10.0% in the previous month. The value of residential building rose 8.0% following a fall of 16.3% in the previous month. The value of non-residential building fell 14.1% following a rise of 4.7% in the previous month.

We wonder about the accuracy of the seasonally adjusted data, which appears to be moving significantly month by month. ABS states that:

seasonal adjustment is a means of removing the estimated effects of seasonal and calendar related variation from a series so that the effects of other influences can be more clearly recognised. It does not remove the effect of irregular or other influences (e.g. the approval of large projects or a change in the administrative arrangements of approving authorities). State/territory series are seasonally adjusted independently of the Australian series. In general, the sum of the state/territory estimates are reconciled to equal the Australian total estimates. Seasonally adjusted estimates are produced by a seasonal adjustment method which takes account of the latest available original estimates. A detailed review of seasonal factors is conducted annually, generally prior to the release of data for May. Trend estimates are created by smoothing seasonally adjusted series to reduce the impact of the irregular component of the seasonally adjusted series. Abnormally high or low values (outliers) are discounted or excluded from the trend estimates.

That said, the low interest rate environment does appear to be flowing through into construction, as the RBA hoped.