Australia’s fiscal stimulus package to protect the economy against the impact of the coronavirus may run as high A$10 billion. Via Bloomberg.

The Sunday Telegraph newspaper reported that the package was likely to be $5 billion while broadcaster Sky News said the stimulus could be up to

twice this amount. Australia is expected to reveal details of its plans

on Tuesday, when Prime Minister Scott Morrison and his Cabinet meet.

Governments around the world have already pledged more than US$54 billion in budget support to counter the virus’s impact. Morrison has yet to put a figure on his plan, which he has said will be “targeted, measured and scalable,” with an emphasis on protecting business cash flow and jobs.

Initial estimates of the

coronavirus’s impact from the nation’s Treasury and central bank suggest

the economy is likely to suffer a quarterly contraction

for the first time in nine years. For Australia, the blow is coming hot

on the heels of a summer of devastating wildfires that were already

expected to crimp growth.

While

the country had only reported 74 confirmed cases of the virus as of

Sunday, including three deaths, its economy is particularly exposed to

China, the center of the outbreak. China is Australia’s key market for

commodity exports and a vital source of tourists and students for the

services sector.

The Australian Financial Review reported the package may feature tax breaks to spur emergency investment by big businesses while the Australian newspaper said stimulus could include cash payments to households.

The

Sunday Telegraph report said the government was looking at wage

subsidies and payments for small businesses. It also said the government

may encourage pensioners to spend more by lowering the amount they are

allowed to earn from financial assets before receiving government

assistance

The latest edition of our weekly finance and property news

digest with a distinctively Australian flavour.

Contents:

00:20 Introduction

00:54 US Markets

02:10 Federal Reserve Actions

03:40 Federal Reserve Tools

06:00 Negative Rates

09:00 China

09:40 Japan

10:40 UK

11:20 Global Debt crisis

14:05 Australian Section

14:10 RBA Cuts

15:00 Retail Sales

15:50 Economic Outlook – U shaped

17:00 Markets

18:00 Bank Profitability

19:45 Property Markets

Transcript (by popular demand).

Hello again, its Martin North from Digital Finance Analytics, welcome to our

latest post covering finance and property news with a distinctively Australian

flavour. In the review of this week’s news, we look at the market gyrations,

central bank responses and the limitations of monetary policy. As normal we

start with the global scene, but if you want to jump direct to the Australian

section, the time is shown below. And a

quick reminder, due to YouTube’s restrictions, I will only discuss the current

medical situation obliquely, to avoid demonetisation using the term “Panic Not

101”.

In the

US, Stocks closed in the red on Friday, but well-off lows thanks to some

late-day buying in what was another hectic final hour of trading. At the close

in NYSE, the Dow Jones Industrial Average lost 0.98% to 25,866, while the S&P 500 index

lost 1.71% to 2,971, and the NASDAQ Composite index fell 1.87% to 8,575. But then Stocks moved back

close to their lows of the day in late trading with investors likely nervous

about staying long into a weekend that will be packed with medical related

headlines. Losses in the Oil & Gas, Basic Materials and Financials sectors

led shares lower.

Volume on

U.S. exchanges was 14.2 billion shares, compared to the 10.54 billion average

for the full session over the last 20 trading days.

Data

showing a robust pace of hiring in February largely went ignored, given that

the data captured little of the impact from the “Panic Not 101”. A sharp

downturn in later economic and corporate earnings data would likely strike a

further blow to U.S. markets, analysts said.

The U.S.

Federal Reserve has begun quarantining physical dollars that it repatriates

from Asia before recirculating them in the U.S. financial system as a

precautionary measure against spreading the virus. Regional Fed banks that help

manage the money supply will set aside shipments of dollars from Asia for seven

to 10 days before processing and redistributing them to financial institutions.

The policy, first reported by Reuters, was implemented on Feb. 21. Is this another covert front in the war on

cash? On average, the Fed distributes $34 billion in paper notes every year,

according to the San Francisco Fed.

A bill

signed by President Donald Trump on Friday will provide US$8.3 billion to

bolster the country’s capacity to test for “Panic Not 101” . Trump signed the

legislation at the end of a week in which the virus began to disrupt daily life

for many Americans. As stocks plunge and U.S. companies grapple with the

economic fallout, his administration is also weighing tax relief for the

cruise, travel and airline industries.

The S&P 500 posted its 10th decline in 12 sessions as crippled

supply chains prompted a sharp cut to global economic growth forecasts for

2020. Since its record closing high on Feb. 19, the benchmark index has lost

more than 12%, wiping out $3.43 trillion from its market capitalization.

Even so,

for the week the S&P 500, along with the Dow Jones Industrial Average and the Nasdaq, posted a modest

gain as stocks on Friday pared losses late in the session. Comments from

Federal Reserve officials about the possibility of using other tools in addition

to interest rate cuts to blunt the economic impact of the “Panic Not 101”

helped stocks ease declines. The S&P 500 gained 0.6%, the Dow added 1.8%

and the Nasdaq rose 0.1%. But we still in correction territory, and the markets

have no means of assessing the emerging global uncertainties.

The

central bank has begun to grapple with what measures it would use if the

outbreak of the illness worsens in the United States and causes a severe economic

downturn.

Federal Reserve regional bank president Eric Rosengren, participated in the Shadow

Open Market Committee economics conference in New York.

“We

should allow the central bank to purchase a broader range of securities or

assets,” Rosengren said in prepared remark, noting it would require a

change to the Fed’s mandate as set by Congress.

The Fed of

course slashed its key overnight lending rate by half a percentage point on

Tuesday to a target range of between 1.00% and 1.25% in an emergency move to

mitigate the effects of the escalating global “Panic Not 101” outbreak on the

U.S. economy. Investors are predicting further U.S. rate cuts in the near

future.

Rosengren

said such an approach would be necessary because if the Fed was forced to slash

rates to effectively zero, the circumstances could have changed, which would

limit the effectiveness of purchasing only Treasury and mortgage-backed

securities, as the central bank did in the 2007-2009 recession. Those

large-scale asset purchases or quantitative easing (QE), aim to stimulating the

economy.

What

changed is the drop in the 10-year U.S. Treasury yield. It fell to a record low

of 0.66% earlier on Friday, on pace for its largest daily fall since October

2011 during the depths of the euro zone sovereign debt crisis, amid concerns

the Panic Not 101 outbreak could cause a global recession. It ended at 0.773

down a massive 16.4%. The 3-month rate dropped even more, down 18.16% to 0.51 –

so the yield curve is not inverted, for now.

“There

would be little room for the Federal Reserve to lower rates through large

purchases of long-term Treasury securities – like it did to make conditions

more accommodative in and after the Great Recession – if a recession occurred

in this rate environment,” Rosengren said.

If the

Fed did change its policy, it should be accompanied by agreement from the U.S.

Treasury to indemnify the central bank against losses, Rosengren added. He did

not specify what types of other securities or assets the Fed would buy.

Rosengren

also said he remained skeptical about introducing negative interest rates to

the United States. Other central banks including in Europe in Japan, have

pushed rates below zero. “In my view, negative interest rates poorly

position an economy to recover from a downturn,” Rosengren said.

In perfect timing the IMF just released a paper “How

Can Interest Rates Be Negative?” in which they discuss the negative interest

rate experiment. Note this chilling comment in their penultimate paragraph “But

the concern remains about the limits to negative interest rate policies so long

as cash exists as an alternative”. So,

here clearly is the link between the ban of cash, and monetary policy – no

conspiracy theory, – plain fact.

The

European Central Bank introduced negative interest rates in 2014 and the Bank

of Japan followed in 2016. The German 10-year was up 1.92% to minus 0.7144. It is

within striking distance of its record low set last September near minus 74 bp. Now of course in Japan, the

Central Bank there has been buying up a range of securities, including stocks,

bonds, and frankly anything with value, as they take the rate negative. Two-year notes in Japan currently yield minus -0.28%.

If

longer-dated U.S. Treasury yields hover near zero, some see a risk that a new

wave of buying could turn shorter-dated ones negative, even without the Fed

adopting a negative policy. So monetary policy madness prevails.

The CBOE

Volatility Index, which measures the implied volatility of S&P 500

options, was up 5.86% to 41.94 a new 5-year high. This underscores the

uncertainty in the markets.

Gold Futures for April delivery was up 0.38% to $1,674.35, so traders are

placing their faith in the yellow metal, Gold jumped almost 7% on the week, its

biggest weekly gain in 11 years. but elsewhere in commodities trading WTI crude

oil fell 9.35% to hit $41.61 a barrel, after OPEC and Russia failed to come up with

a deal expected to cut 1.5 million barrels per day off global supply

The US Dollar Index Futures was down 0.75% at 96.060 while the EUR/USD was

up 0.40% to 1.1284.

Bitcoin was up 0.55% to 9,140, as more investors seek out places to store

cash.

Investors lowered bearish bets on the Chinese yuan as a U.S.

rate cut gave Chinese bonds a yield advantage. Aided by a weakening dollar,

short positions on the Chinese yuan stood at their lowest since early January

2019. The yuan immediately jumped after the rate cut to its highest level since

Jan. 23 and erased all losses it had clocked since the Lunar New Year holiday.

It stood at 6.9373 at the close. The Shanghai index stood at 3,034.51, stronger

than recently.

Weakness in consumption in Japan to start the year lends credence to ideas that the world’s third-largest economy is contracting for the second consecutive quarter.Household spending fell 3.9% year-over-year, nearly matching economists’ projections, after a 4.8% decline in December. It is the fourth straight decline. Durable goods have been especially hard hit, led by a 10.7% decline in January auto sales after an 11.1% decline in December. Some daily data suggest that after the school closures were announced in late February, there may have been some a surge in necessity purchases. Labor cash earnings rose 1.5% year-over-year after a 0.2% fall in December. Yet, details may not be as favorable as the optics. Base pay did accelerate, but the real action came from the 10.2% jump in bonuses. Lastly, the January leading economic indicator fell from 91.0 to 90.3, its lowest level since 2009. The Japanese market dropped to a six-month low, with 97% of shares on the Tokyo exchange’s main board in the red.

In London, Europe’s financial capital, the Canary Wharf district was

unusually quiet. S&P Global’s large office stood empty after the company

sent its 1,200 staff home, while HSBC asked around 100 people to work from home

after a worker tested positive for the illness. The Footsie dropped a

further 3.62% on Friday to 6,462, while the financials index fell 3.84% to

699.80 and the pound US Dollar rose 0.74% to 1.3049.

As I see things, the global uncertainty will hit hard and debt will be the

centre of the storm. According to the Institute of International Finance, a

trade group, the ratio of global debt to gross domestic product hit an all-time

high of over 322 per cent in the third quarter of 2019, with total debt

reaching close to US$253 trillion. Much of the debt build-up since the global

financial crisis of 2007-08 has been in the non-bank corporate sector where the

current disruption to supply chains and reduced global growth imply lower

earnings and greater difficulty in servicing debt. In effect, the Panic Not 101

raises the extraordinary prospect of a credit crunch in a world of ultra-low

and negative interest rates.

As the OECD puts it “In a downturn, some of the disproportionately large

recent issuance of BBB bonds — the lowest investment grade category — could end

up being downgraded. That would lead to big increases in borrowing costs

because many investors are constrained by regulation or self-imposed

restrictions from investing in non-investment grade bonds. The deterioration in

bond quality is particularly striking in the $1.3tn global market for leveraged

loans, which are loans arranged by syndicates of banks to companies that are

heavily indebted or have weak credit ratings. Such loans are called leveraged

because the ratio of the borrower’s debt to assets or earnings is well above

industry norms. New issuance in this sector hit a record $788bn in 2017, higher

than the peak of $762bn before the crisis. The US accounted for $564bn of that

total. Much of this debt has financed mergers and acquisitions and stock

buybacks. Executives have a powerful incentive to engage in buybacks despite

very full valuations in the equity market because they boost earnings per share

by shrinking the company’s equity capital and thus inflate performance related

pay. Yet this financial engineering is a recipe for systematically weakening

corporate balance sheets. Exactly. And

more central bank liquidity actually will not help, indeed it expands debt even

more. Perhaps we are approaching that

Minsky moment. We will see.

So to the local market.

Of course, the RBA cut the cash rate this past week, in response to recent

events putting the cash rate at a record-low 50 bp. Because the Fed cut more,

in fact the Ozzie Doller is looking a little stronger, having dropped to record

recent lows. It ended at 66.50, up 0.56%. That is a problem, in that the RBA

needs to dollar to go lower, to help protect the local economy, and this may in

fact signal they should have cut harder. But then again, with only 0.25% in the

locker before practically speaking hitting zero bounds (because of the RBA’s

rate corridor) they are caught now. We

are now expecting a further “emergency” cut, and even QE in short order, to try

to support the economy.

And if you want to understand why that support is needed, you should watch my recent show “The State of the Economy in ~ 10 Slides” There we discuss Australia’s retail sales which unexpectedly fell in January by 0.3% after the 0.7% decline at the end of last year. It is the first back-to-back decline in retail sales since July-August 2017. Weak wages, the peak of the wildfires, and high household debt levels are the likely culprits.

The Australian reported that Australia faces an “unprecedented” fall in

international visitor arrivals from key countries as the Panic Not 101 outbreak

feeds a record number of holiday cancellations and a 36 per cent fall in

bookings since December. Tourism

Australia data revealed a wipe-out in international airline bookings from key

tourism markets, including China, Britain, Canada, the US, India, Japan and

Singapore. The travel ban on China, Australia’s biggest tourism market with

about 1.4 million international visitors each year, has triggered a paralysis

in bookings and a flood of forward cancellations from Chinese tourists.

Belatedly they are trying an advertising blitz in Europe and the USA, but too

little too late.

S&P cut their growth forecast for Asia pacific to 4%, assuming what they

call a U-shaped recovery, and they said that Australia is quite vulnerable, with

growth in 2020 expected to touch 1.2%, well below trend. “Australia’s

most-disrupted sectors employ a large share of workers which will weaken both

the labor market and consumer confidence,” S&P said. Services account for

almost 80% of employment with accommodation and catering, sensitive to tourism

and discretionary consumer spending, alone making up over 7%. We expect the

Reserve Bank of Australia to cut rates once more to 0.25%. Of course no-one can tell for how long the

disruption will run. Our modelling suggests the Australian economy is on the

verge of a six-month shut down. There won’t be much internal movement. The

borders will remain closed, at first by us and then by everyone else as they recover,

but we get sicker. The private sector will hunker down. And the public sector

will enter a valiant struggle with the threat.

The ASX 100 dropped 2.8% to 5157.90, while the ASX financials dropped 4.8% to 5,397.60. Bank stock prices were hit hard this week. ANZ was down 4.73% to 22.14, as it announced further job cuts. CBA slipped 3.67% to 73.93, NAB dropped 5.22% to 22.075 and Westpac was down 4.04% to 21.35, and confirmed that John McFarland will take the Chair at the bank from 1st April. Regionals were crunched, with Bank of Queensland down 4.02% to 6.93, Suncorp down just 2.18% to 11.20 and Bendigo Bank down 8.15% to 7.78. Bendigo did a capital raising, recently and remains under pressure. Elsewhere AFG, the aggregator slid 7.08% to 2.23 and Macquarie fell 4.07% to 131.93.

Lower rates of course crush margins, and most lenders passed on the full 25

basis point cut to mortgage borrowers. They are busily trimming deposit rates further

– savers once again a silent victim in all this. The RBA is of course are assuming

that the banks can lend more as rates fall (to drive more consumption) but

consumers and businesses are not confident at the moment, and household debt is

very high. In addition, many deposit returns are already so close to zero that

they cannot recover another 25 basis points. So net, net rate cuts are eating

into bank profits, dividends will be lower, and risks of default are rising

among consumers and businesses as the economy supply side shocks kick in. We

think there are limited tools to support the market from here, and in fact, QE

will not do much, when it comes. Welcome to a Japanisation of the economy.

Fitch reported little change in mortgage arrears in the last quarter of

2019, Australia’s 30+ days mortgage arrears were down 1bp to 1.06% in 4Q19 from

the previous quarter, and 1bp higher from the year earlier; 30+ days arrears

have now been below 1.2% for the past two and a half years. They make the point

that the bushfires occurred in remote or regional areas with low population

levels, while the mortgage portfolios typically securing RMBS notes are

concentrated in densely populated areas that were not directly affected by the

bushfires. The Panic Not 101 outbreak could indirectly affect arrears

performance due to lower incomes stemming from a fall in tourist numbers

following the implementation of travel restrictions.

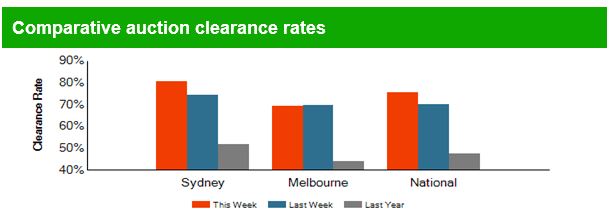

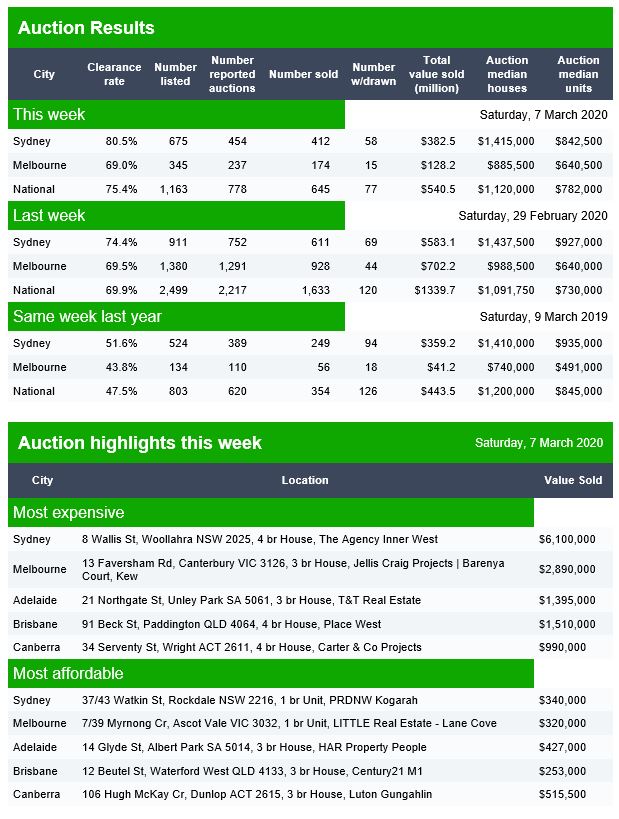

Last Saturday we saw significant auction results, with 2,933 listed and 1,592

cleared according to Corelogic, giving a 77.1% weighted average clearance.

Sydney was at 81% and Melbourne at 77%.

A year ago there were 2,301 listed and 50.4% cleared.

Their home price index was up again, with weekly rises of 0.4% in Sydney,

0.3% in Melbourne and 0.12% in Adelaide. Perth managed a 0.08% rise and

Brisbane just 0.06%. As a result, there are average quarterly rises of 4.55% in

Sydney and 3.82% in Melbourne. From peak

though Perth is down 21.0% and Sydney is still also in negative territory

(before any inflation adjustments are applied). And again, these are averages,

prices on the ground vary considerably, with many areas still lower than a year

back. Rises are weighted towards more expensive property, which had dropped the

most earlier.

Corelogic also said that Darwin home prices have fallen for 68 months and is

32.7% below its May 2014 peak. In inflation-adjusted terms, Darwin’s dwelling

values have declined by around 36% from peak. Perth is the other housing market

that is yet to stage any meaningful recovery, even though it rebounded

marginally over the past quarter. Its dwelling values are still 21.0% below

their June 2014, or around 27.0% lower in real terms.

They also reported in their quarterly rental report that annual rental

growth nationally (1.3%) remains below inflation (1.8%), with national capital

city rental growth (0.8%) even weaker. Sydney’s rental growth (0.5% QoQ; -0.6%

YoY) remains especially weak, which pulled down rents nationally. While there

are some variations across locations and between houses and units, property

investors are in for a torrid time. Recent price growth in both Sydney and

Melbourne against soft/negative rental growth has driven gross rental yields

into the gutter, with both Sydney and Melbourne house yields well below 3% –

near the lowest level on record. Net returns are even worse.

And SQM research released its Stock on Market report for February, which

revealed that property listings rose by 0.2% over the month but were still down

13.8% year-on-year. But listings in Sydney and Melbourne bounced, jumping by

9.9% and 10.0% respectively in February.

We think home prices will react to the recent uncertainty, and rising

supply. It is just a timing issue.

The S&P/ASX 200 VIX, which measures

the implied volatility of S&P/ASX 200 options, was up 20.47% to 26.687 a

new 3-years high. Risk is on. The Euro

Aussie Dollar was at 1.6973, the Aussie Gold cross was down 0.41% to 2,519.20

and the Aussie Bitcoin cross was down 0.26% to 13,812.9

So, in summary, the uncertainty in the outlook is looking decidedly dark.

There are few places to hide, and the question now is how soon will property

prices slide back – we are expecting some fiscal stimulus and it will be

interesting to see if it is directed at the property sector – is should not be,

as there are more immediate needs among small businesses, but then again the

Government does appear to love property. We will see.

Volume is significantly down from last week – possibly a function of the Melbourne long weekend, or perhaps the hit of doubts regarding the Covid-19? Still higher than last year at this time.

Canberra listed 23 auctions, reported 15 and sold 11, with 1 withdrawn and 4 passed in to give a Domain clearance of 69%.

Brisbane listed 76 auctions, reported 43 and sold 26, with 1 withdrawn and 17 passed in to give a Domain clearance of 59%.

Adelaide listed 44 auctions, reported 29, and sold 22, with 2 withdrawn and 7 passed in.

Hot off the press – How Can Interest Rates Be Negative? – we get the latest missive from the IMF which confirms precisely what we have been saying.

But the concern remains about the limits to negative interest rate policies so long as cash exists as an alternative.

Here is the article. Read, and weep….

Money has been around for a long time. And we have always

paid for using someone else’s money or savings. The charge for doing this is

known by many different words, from prayog in ancient Sanskrit to interest in

modern English. The oldest known example of an institutionalized, legal

interest rate is found in the Laws of Eshnunna, an ancient Babylonian text

dating back to about 2000 BC.

For most of history, nominal interest rates—stated rates

that borrowers pay on a loan—have been positive, that is, greater than zero.

However, consider what happens when the rate of inflation exceeds the return on

savings or loans. When inflation is 3 percent, and the interest rate on a loan

is 2 percent, the lender’s return after inflation is less than zero. In such a

situation, we say the real interest rate—the nominal rate minus the rate of

inflation—is negative.

In modern times, central banks have charged a positive

nominal interest rate when lending out short-term funds to regulate the

business cycle. However, in recent years, an increasing number of central banks

have resorted to low-rate policies. Several, including the European Central

Bank and the central banks of Denmark, Japan, Sweden, and Switzerland, have

started experimenting with negative interest rates —essentially making banks

pay to park their excess cash at the central bank. The aim is to encourage

banks to lend out those funds instead, thereby countering the weak growth that

persisted after the 2008 global financial crisis. For many, the world was

turned upside down: Savers would now earn a negative return, while borrowers

get paid to borrow money? It is not that simple.

Simply put, interest is the cost of credit or the cost of

money. It is the amount a borrower agrees to pay to compensate a lender for using

her money and to account for the associated risks. Economic theories

underpinning interest rates vary, some pointing to interactions between the

supply of savings and the demand for investment and others to the balance

between money supply and demand. According to these theories, interest rates

must be positive to motivate saving, and investors demand progressively higher

interest rates the longer money is borrowed to compensate for the heightened

risk involved in tying up their money longer. Hence, under normal

circumstances, interest rates would be positive, and the longer the term, the

higher the interest rate would have to be. Moreover, to know what an investment

effectively yields or what a loan costs, it important to account for inflation,

the rate at which money loses value. Expectations of inflation are therefore a

key driver of longer-term interest rates.

While there are many different interest rates in financial

markets, the policy interest rate set by a country’s central bank provides the

key benchmark for borrowing costs in the country’s economy. Central banks vary

the policy rate in response to changes in the economic cycle and to steer the

country’s economy by influencing many different (mainly short-term) interest

rates. Higher policy rates provide incentives for saving, while lower rates

motivate consumption and reduce the cost of business investment. A guidepost

for central bankers in setting the policy rate is the concept of the neutral

rate of interest : the long-term interest rate that is consistent with stable

inflation. The neutral interest rate neither stimulates nor restrains economic

growth. When interest rates are lower than the neutral rate, monetary policy is

expansionary, and when they are higher, it is contractionary.

Today, there is broad agreement that, in many countries,

this neutral interest rate has been on a clear downward trend for decades and

is probably lower than previously assumed. But the drivers of this decline are

not well understood. Some have emphasized the role of factors like long-term

demographic trends (especially the aging societies in advanced economies), weak

productivity growth, and the shortage of safe assets. Separately, persistently

low inflation in advanced economies, often significantly below their targets or

long-term averages, appears to have lowered markets’ long-term inflation

expectations. The combination of these factors likely explains the striking

situation in today’s bond markets: not only have long-term interest rates

fallen, but in many countries, they are now negative.

Returning to monetary policy, following the global financial

crisis, central banks cut nominal interest rates aggressively, in many cases to

zero or close to zero. We call this the zero lower bound, a point below which

some believed that interest rates could not go. But monetary policy affects an

economy through similar mechanics both above and below zero. Indeed, negative

interest rates also give consumers and businesses an incentive to spend or

invest money rather than leave it in their bank accounts, where the value would

be eroded by inflation. Overall, these aggressively low interest rates have

probably helped somewhat, where implemented, in stimulating economic activity,

though there remain uncertainties about side effects and risks.

A first concern with negative rates is their potential

impact on bank profitability. Banks perform a key function by matching savings

to useful projects that generate a high rate of return. In turn, they earn a

spread, the difference between what they pay savers (depositors) and what they

charge on the loans they make. When central banks lower their policy rates, the

general tendency is for this spread to be reduced, as overall lending and

longer-term interest rates tend to fall. When rates go below zero, banks may be

reluctant to pass on the negative interest rates to their depositors by

charging fees on their savings for fear that they will withdraw their deposits.

If banks refrain from negative rates on deposits, this could in principle turn

the lending spread negative, because the return on a loan would not cover the

cost of holding deposits. This could in turn lower bank profitability and

undermine financial system stability.

A second concern with negative interest rates on bank deposits

is that they would give savers an incentive to switch out of deposits into

holding cash. After all, it is not possible to reduce cash’s face value (though

some have proposed getting rid of cash altogether to make deeply negative rates

feasible when needed). Hence there has been a concern that negative rates could

reach a tipping point beyond which savers would flood out of banks and park

their money in cash outside the banking system. We don’t know for sure where

such an effective lower bound on interest rates is. In some scenarios, going

below this lower bound could undermine financial system liquidity and

stability.

In practice, banks can charge other fees to recoup costs,

and rates have not gotten negative enough for banks to try to pass on negative

rates to small depositors (larger depositors have accepted some negative rates

for the convenience of holding money in banks). But the concern remains about

the limits to negative interest rate policies so long as cash exists as an

alternative.

Overall, a low neutral rate implies that short-term interest rates could more frequently hit the zero lower bound and remain there for extended periods of time. As this occurs, central banks may increasingly need to resort to what were previously thought of as unconventional policies, including negative policy interest rates.

No, central banks are taking us down a blind alley!

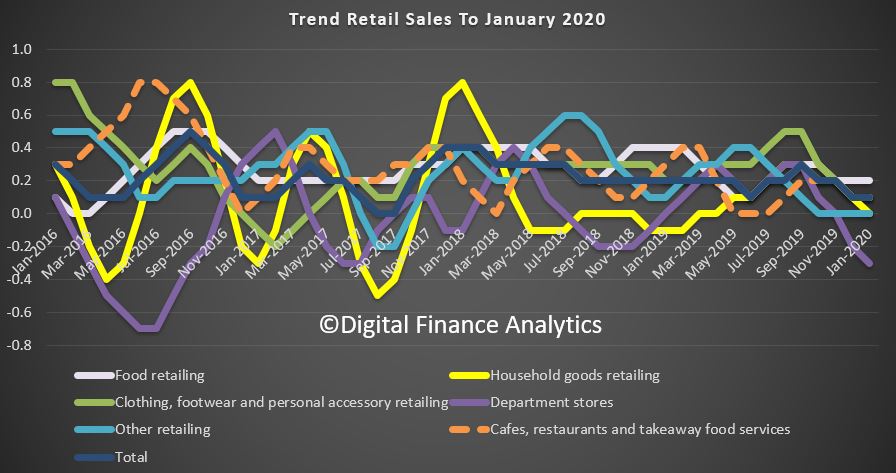

The trend estimate rose 0.1% in January 2020. This follows a rise of 0.1% in December 2019, and a rise of 0.2% in November 2019.

The seasonally adjusted estimate fell 0.3% in January 2020. This follows a fall of 0.7% in December 2019, and a rise of 1.0% in November 2019.

In trend terms, Australian turnover rose 2.3% in January 2020 compared with January 2019.

Compared to January 2019, the trend estimate rose 2.3 per cent.

The following industries rose in trend terms in January 2020: Food retailing (0.2%), Cafes, restaurants and takeaway food services (0.1%), and Clothing, footwear and personal accessory retailing (0.1%). Household goods retailing (0.0%), and Other retailing (0.0%) were relatively unchanged. Department stores (-0.3%) fell in trend terms in January 2020.

The following states and territories rose in trend terms in January 2020: Queensland (0.3%), Victoria (0.2%), Tasmania (0.7%), and the Northern Territory (0.1%). South Australia (0.0%), and Western Australia (0.0%) were relatively unchanged. New South Wales (-0.1%), and the Australian Capital Territory (-0.2%) fell in trend terms in January 2020.

“Bushfires in January negatively impacted a range of retail businesses across a variety of industries” said Ben James, Director of Quarterly Economy Wide Surveys. “Retailers reported a range of impacts that reduced customer numbers, including interruptions to trading hours and tourism.”

There were falls for household goods retailing (-1.1 per cent), department stores (-2.2 per cent), clothing, footwear and personal accessory retailing (-1.1 per cent), cafes, restaurants and takeaway food services (-0.3 per cent), and other retailing (-0.1 per cent). These falls were partially offset by a rise in food retailing (0.4 per cent).

In seasonally adjusted terms, there were falls in Western Australia (-1.1 per cent), Victoria (-0.2 per cent), the Australian Capital Territory (-2.3 per cent), New South Wales (-0.1 per cent), Queensland (-0.1 per cent), Tasmania (-0.5 per cent), and the Northern Territory (-0.5 per cent). South Australia (0.1 per cent) rose in seasonally adjusted terms in January 2020.

Online retail turnover contributed 6.3 per cent to total retail turnover in original terms in January 2020. In January 2019, online retail turnover contributed 5.6 per cent to total retail.

Chief Economist for the ABS, Bruce Hockman, said: “The economy has continued to grow and picked up through the year, however the rate of growth remains below the long run average.”

Domestic demand remained subdued with 0.1 per cent growth in the December quarter. A pick up in household discretionary spending and continued increases in the provision of government services was dampened by falls in dwelling and private business investment.

Falls in dwelling investment continued, declining 3.4 per cent during the quarter, the sixth consecutive fall. This fall was consistent with the decline in construction industry value added, falling 2.3 per cent. The housing market recovery is evident in the increase in ownership transfer costs, rising 12.3 per cent during the quarter to be up 6.5 per cent through the year.

Household income remained steady with compensation of employees recording its twelfth consecutive rise, increasing 1.0 per cent during the quarter. This reflects a rise in the number of wage and salary earners as well as a steady increase in the wage rate. Non-life insurance claims contributed to household income reflecting increased claims attributed to natural disaster occurrences in the quarter. The household saving to income ratio was 3.6 per cent, driven by the subdued consumption coupled with steady increases in wages and a boost in insurance claims.

The Mining industry provided additional strength to the economy, with growth in production volumes of 1.6 per cent, strengthening through the year to 7.3 per cent. This was reflected in the growth in mining exports and inventories.

Falling prices for key export commodities impacted the terms of trade in the December quarter, which fell 5.3 per cent. This reduced nominal GDP, which fell 0.3 per cent, as lower coal, iron ore and gas prices contributed to more subdued company profits. Mining profits declined 2.6 per cent for the quarter.

Real net national disposable income declined 0.9 per cent. “Fluctuations in commodity prices have significant effects on the Australian economy in terms of export revenues and real income,” added Mr Hockman.

But the real question is, does the GDP really tell us anything useful? I discuss the GDP question with American in OZ Salvatore Babones, Associate Professor, University of Sydney.

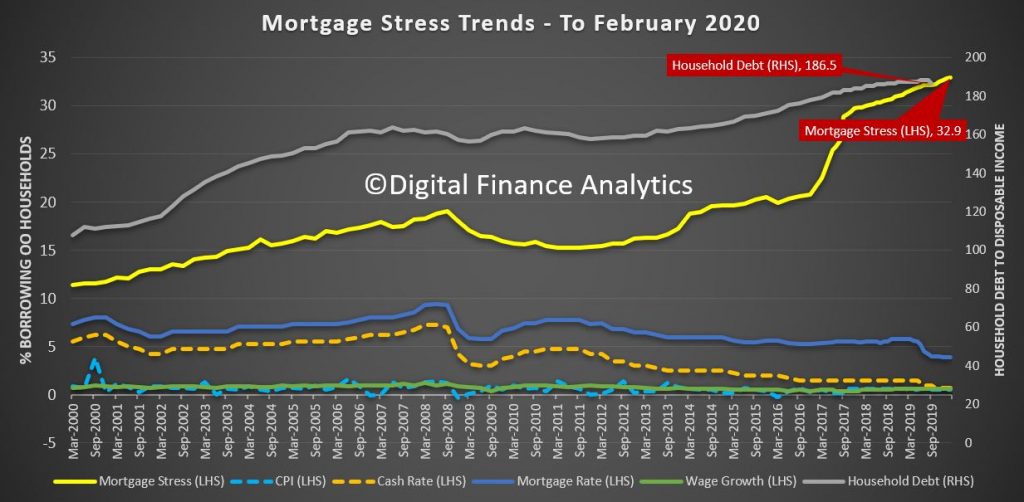

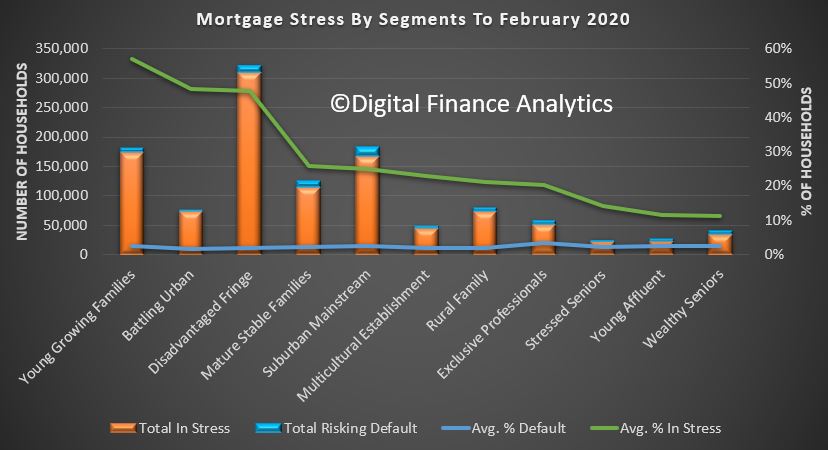

The official story is that lower interest rates are translating to reduced financial stress in the community. The true story, as revealed in the latest edition of our mortgage stress analysis is that more households are up against it, with a record 32.9% of mortgages households wrestling with cash flow issues. This translates to 1.08 million households in stress, and more than 82,000 risking default in the months ahead.

Many households are chasing their tails, in that while mortgage repayments are dropping – for some, rising living costs and flat real incomes are compounding their financial pressures. There was a sharp downturn in take home pay, thanks to bushfires and the virus is beginning to hit businesses, (who in turn are less able to pay and retain staff, especially those on “flexible” contracts).

Across our master household segments, the highest proportion of households under pressure are “Young Growing Families”, which includes many recent first time buyers, “Battling Urban” – those older households living in the main urban corridors, and “Disadvantaged Fringe” households, those living in the often new fringe developments are also at the top of the list. That said, stress takes no prisoners, in that even some wealthy households, and more mature families are also under pressure.

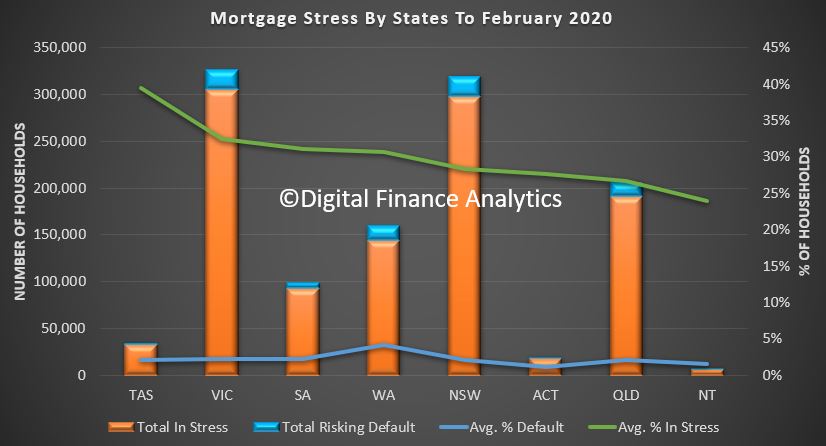

Across the states, the highest proportion of households are in Tasmania, where the recent run up in prices, against high costs and low wages is a nasty cocktail. As yet though defaults remain low here. Western Australia has a significantly higher level of defaults, because the financial pressures have been running for years. The largest counts of stressed households are located in Victoria and New South Wales, with Queensland also seeing a further rise. Defaults are expected to rise again.

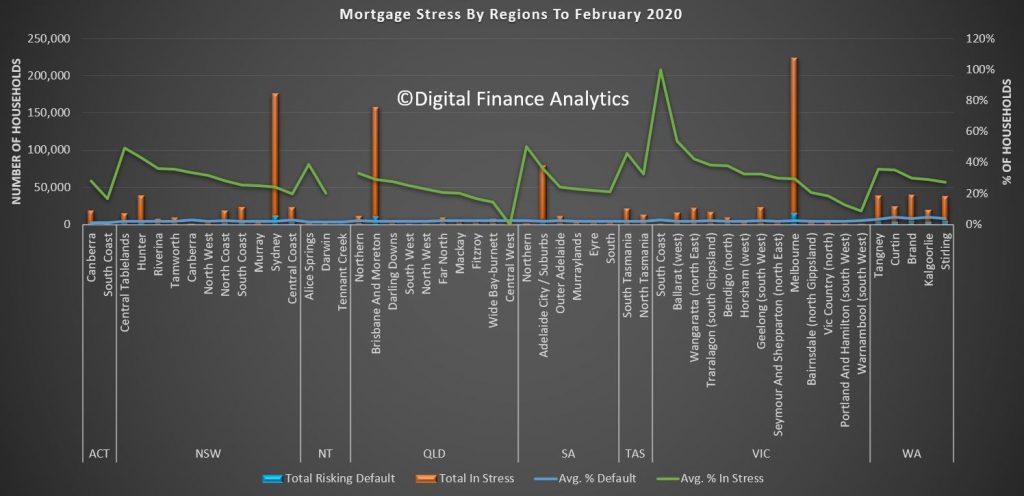

Across the regions, there are considerable variations, with a significant spike in some areas following the recent bushfires.

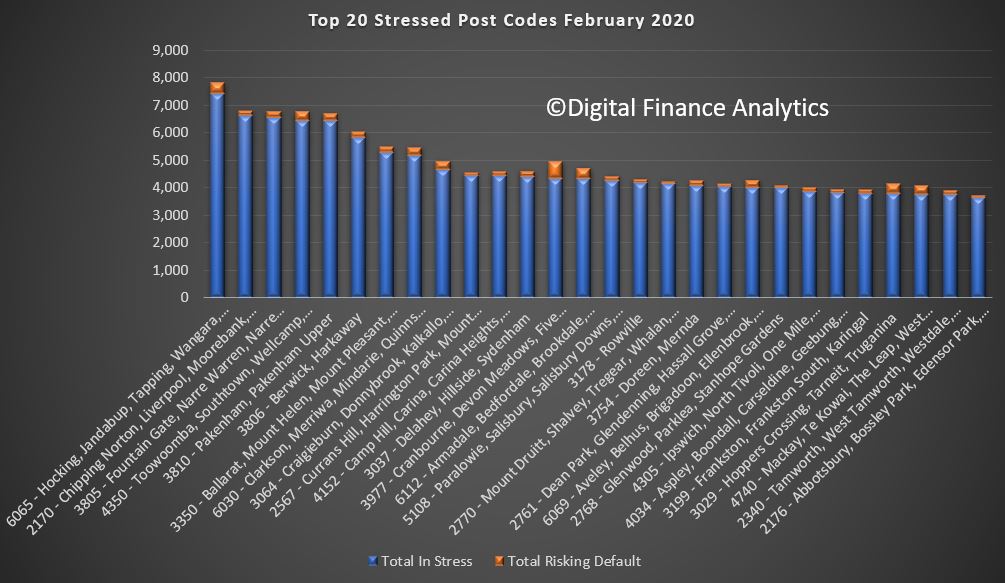

The top 20 post codes reveals that WA post code 6065 which includes Tapping and Hocking tops the list this month, with more than 7,000 households impacted. Liverpool, 2170, in New South Wales, Narre Warren 3805 in Victoria and Toowoomba 4350 in Queensland are all at the top of the list. The common theme here is significant and recent higher density development, large mortgages and over priced real estate (and supported by insufficient infrastructure).

As always we remind households that maintaining a cash flow record is an essential tool to managing a household budget – there are good tools available on ASIC’s Money Smart Web Site. Less than half of the households surveyed know their financial status. Careful prioritisation, and repaying higher interest debts first often makes the most sense, especially when wages growth will remain sluggish (and before the economic impact of the virus really hits). Finally, refinancing may provide short term relief, but without a change in behaviour this will not be long lasting.

The US Federal Reserve Board on Wednesday approved a rule to simplify its capital rules for large banks, preserving the strong capital requirements already in place.

The “stress capital buffer,” or SCB,

integrates the Board’s stress test results with its non-stress capital

requirements. As a result, required capital levels for each firm would

more closely match its risk profile and likely losses as measured via

the Board’s stress tests. The rule is broadly similar to the proposal

from April 2018, with a few changes in response to comments.

“The stress capital buffer materially

simplifies the post-crisis capital framework for banks, while

maintaining the strong capital requirements that are the hallmark of the

framework,” Vice Chair for Supervision Randal K. Quarles said.

The SCB uses the results from the Board’s

supervisory stress tests, which are one component of the annual

Comprehensive Capital Analysis and Review (CCAR), to help determine each

firm’s capital requirements for the coming year. By combining the

Board’s stress tests—which project the capital needs of each firm under

adverse economic conditions—with the Board’s non-stress capital

requirements, large banks will now be subject to a single,

forward-looking, and risk-sensitive capital framework. The

simplification would result in banks needing to meet eight capital

requirements, instead of the current 13.

The SCB framework preserves the strong

capital requirements established after the financial crisis. In

particular, the changes would increase capital requirements for the

largest and most complex banks and decrease requirements for less

complex banks. Based on stress test data from 2013 to 2019, common

equity tier 1 capital requirements would increase by $11 billion in

aggregate, a 1 percent increase from current capital requirements. A

firm’s SCB will vary in size throughout the economic cycle depending on

several factors, including the firm’s risks.

To reduce the incentive for firms to take

on risk and further simplify the framework, the final rule does not

include a stress leverage buffer as proposed. All banks would continue

to be subject to ongoing, non-stress leverage requirements.

Large banks have substantially increased

their capital since the first round of stress tests in 2009. The common

equity capital ratio of the banks in the 2019 CCAR has more than doubled

from 4.9 percent in the first quarter of 2009 to 12.2 percent in the

fourth quarter of 2019, with total capital doubling to more than $1

trillion.

Also on Wednesday, the Board released the

instructions for the 2020 CCAR cycle. The instructions confirm that 34

banks will participate in this year’s test. CCAR consists of both the

stress tests that assess firms’ capital needs under stress and, for the

largest and most complex banks, a qualitative evaluation of the

practices these firms use to determine their capital needs in normal

times and under stress. Results will be released by June 30.