We look at a global study of superannuation (pensions) and see where Australia stands, and also discuss the elephant in the room – poor returns in a low rate environment.

https://www.monash.edu/business/monash-centre-for-financial-studies

"Intelligent Insight"

We look at a global study of superannuation (pensions) and see where Australia stands, and also discuss the elephant in the room – poor returns in a low rate environment.

https://www.monash.edu/business/monash-centre-for-financial-studies

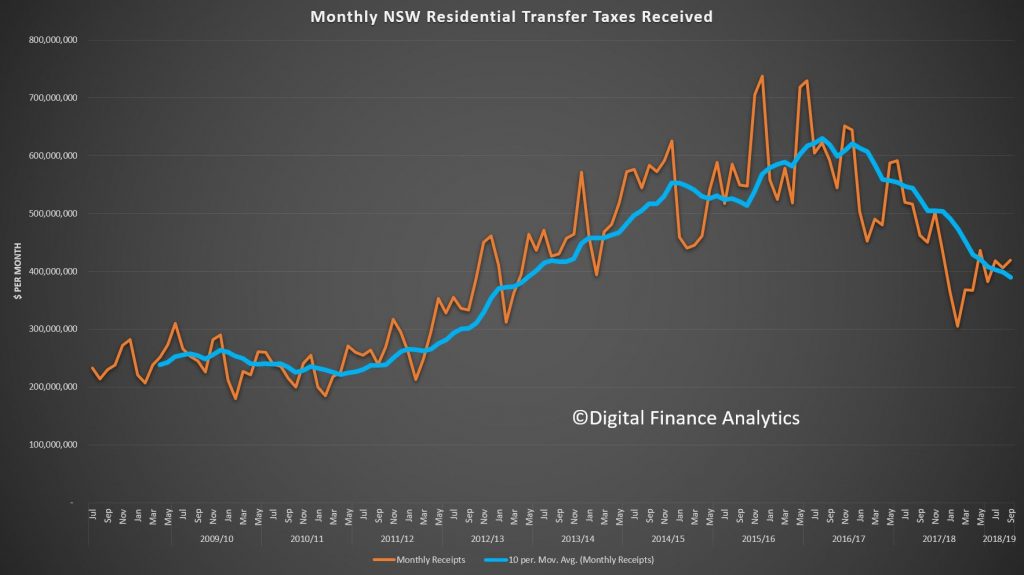

Revenue NSW released their data to end September today. Residential transfers are significantly down on recent trends.

This will put a hole in the state budget. They note:

Data as at 01 October 2019. Report includes all Land Related Transfer Duty documents lodged with Revenue NSW between 01-Jul-2009 and 30-Sep-2019.

Report includes all Land Related Property Sales excluding Fixed Duty and Exemptions (except FHPlus, First Home New Home and First Home Buyers Assistance).

Report is only as accurate as information provided by clients.

I caught up with world renowned economist Harry Dent, ahead of his latest visit to Australia next month, and we discussed the debt and housing bubbles and how this may play out.

As a valued-add, you can secure up to 2 complimentary tickets to Harry’s Australian events.

Melbourne: November 17th-18th

Sydney: November 19th-20th

Brisbane: November 21st-22nd

Perth: November 24th-25th

That’s right. By clicking on the special link below you won’t have to pay anything.

Simply click here to secure your complimentary tickets

I have to warn you though. I’ve only been given a total of 50 complimentary tickets to give away and once they’re gone, they’re gone.

[Note: I get no benefit from publicizing these events]

We discuss the additional questions we were not able to cover during our live stream last week – see below for original show (commences at 00:30).

The G7 warns against the early deployment of Stablecoins like Libra.

The latest edition of our weekly finance and property news digest with a distinctively Australian flavour.

Contents:

0:23 Introduction

1:18 US

2:21 US Retail

3:15 US Markets

4:10 China’s Growth

5:10 Brexit and UK Markets

07:05 Germany

09:00 Australia

09:05 Latitude Failed Float

10:10 Bank of Queensland Result

10:42 Regionals Under Pressure

11:10 Unemployment

11:32 RBA Comments

12:40 Property Auctions and Prices

14:05 Mascot Tower defects

14:35 Local Market

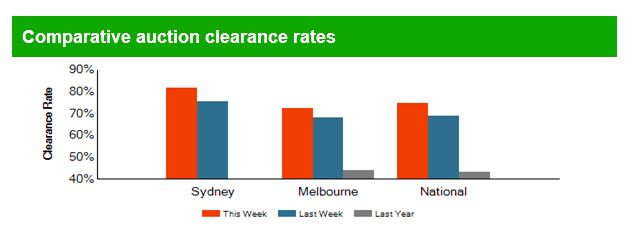

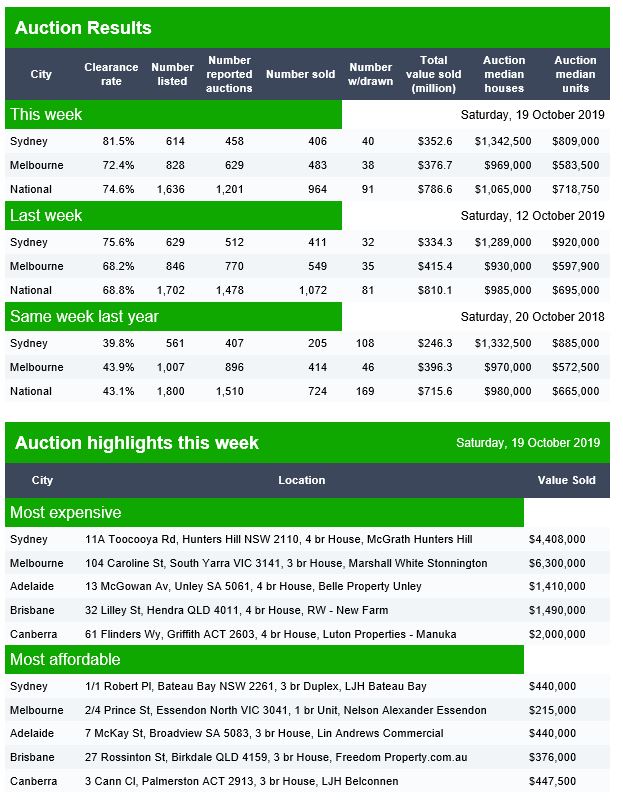

Domain published their preliminary results for today.

The listing count is lower than a year ago, though by not much, but sold volume is higher now.

Canberra listed 58 auctions, reported 46 with 32 sold, 2 withdrawn and 14 passed in to give a Domain result of 67%.

Brisbane listed 85 auctions, reported 40 with 23 sold, 8 withdrawn and 17 passed in to give a Domain result of 48%.

Adelaide listed 51 auctions, reported 28 with 20 sold, 3 withdrawn and 8 passed in to give a Domain result of 65%.

Against seemingly all the odds, we have a new Brexit deal. As an apparent vindication of UK prime minister Boris Johnson’s strategy to ramp up the threat of a no-deal departure from the EU and to force concessions from Brussels, one would imagine that Number 10 is rather happy right now. But that happiness will be tempered with caution, because some major issues lie ahead.

Negotiations in Brussels have produced legal texts on arrangements for Northern Ireland and on the political declaration, which outlines the broad outline of what the two sides want from their future relationship. These are the product of months of planning by the British government, so it’s reasonable to ask what has actually changed since former prime minister Theresa May struck her original deal.

Reading the text, the first impression is that there’s much more that hasn’t changed than has.

The protocol on Northern Ireland and Ireland has long been in the firing line. It proposes a backstop arrangement that would keep Northern Ireland in close alignment with the EU unless and until both UK and EU agreed to change that.

On that front, the introduction of a section on “democratic consent” is an important shift on the EU side. This provides a mechanism for the Northern Ireland Assembly to vote on whether to maintain the provisions of the protocol, with a requirement to have cross-community support. That means the UK is now no longer subject to the EU’s approval if it wants to end the backstop arrangement.

That said, a voting requirement to have majorities from both unionist and nationalist groupings makes it very hard to achieve – especially since the Northern Ireland Executive broke down several years ago and is still not in operation. While the Democratic Unionist Party (DUP) might control unionist voting, it can only do the same with nationalists if it creates a much more benign and cooperative environment. And even if that does happen and arrangements are voted down by Stormont, there is still a long phasing-out period, so things cannot move too quickly.

From the EU’s perspective, this arrangement provides a degree of security, mainly because any decision to overturn the system is not solely in the hands of the UK – which has not been the most reliable partner of late.

The other big change is on customs arrangements. Instead of creating a temporary customs area for the whole of the UK, the revised Protocol makes Northern Ireland a part of the UK’s customs territory. Because that would imply border controls, a rather convoluted system of custom duty collection is set out.

In essence, the system collects duties from businesses, dependent upon where goods are coming from and going to, with the possibility of various exemptions that will be agreed down the line.

It’s a much more complex system than before, but it does allow Johnson to argue that the entire UK is leaving the EU’s customs union, allowing it to benefit from any new trade deals that might be concluded.

Meanwhile, the political declaration, the main change is that the UK now suggests it is looking for a much looser future relationship, based on a free trade agreement, rather than anything that might include participation in the EU’s single market or customs union.

While these are all noteworthy, they do represent only a very small part of the totality of the withdrawal agreement, as agreed by May last November. The Protocol still kicks into effect at the end of a transition period and the effect is still that Northern Ireland is kept very close to EU’s regulatory standards for many years. The future relationship remains as aspirational as May’s plans – until such a document is negotiated and ratified, by some future British government, no one can be sure what it will look like.

Nor did this negotiation touch on citizens’ rights, financial liabilities, the power of the EU’s courts to issue definitive rulings on matters of dispute (an important matter for hard Brexit supporters in the Conservative Party) or the institutional arrangements for managing all of this. Even as Number 10 goes into its selling mode, those continuities from last year’s text will be present in many people’s minds.

The plan still seems to be for the government to present this deal to the UK parliament in a special Saturday sitting on October 19. We already know that the DUP has issues with the revised text because it places Northern Ireland in a different legal position to the rest of the UK, so winning that vote looks even harder than it already did. The government will hope that it can present the deal to MPs as the last, best hope for a Brexit settlement – but, with wobbles from the DUP, Johnson will struggle to get close to a majority.

Even if he does, the potential to keep that majority together for the subsequent passage of the Withdrawal Agreement Bill looks even less likely. And remember that, as things stand today, this text isn’t even signed off by the 27 EU member states – there’s now not really enough time for them to digest and approve something that moves them off their previous position.

In short, this might still fall apart for Johnson, just as it did for May.

Author: Simon Usherwood, Professor in Politics, University of Surrey

Here is a show about my submission to the Senate Inquiry into Audit in Australia, where I focus in on the key issues, show some of the gaps in the current system and suggest reform. Submission close on 28th October if you want to have your say!

Just remember the many banks which passed audit in 2018 and then failed, as this Guardian article at the time highlights.

On 1 August 2019 the Senate referred an inquiry into the regulation of auditing in Australia to the Parliamentary Joint Committee on Corporations and Financial Services for report by 1 March 2020.

Submissions close on 28 October 2019. DFA has made a submission.

We welcome the current inquiry and note the similar initiatives underway in several other jurisdictions. This is an important issue.

We believe there is a need to refocus the auditing practices which are currently deployed by the “big four” firms in particular and the industry more widely. We reach these conclusions, having analysed the financial sector for more than 30 years, as a consultant, financial firm employee and a partner within Arthur Andersen before its dissolution.

There are many threads to the argument, but, these large audit firms are in our opinion too close to management of large companies, as they both advise them on strategy and tax minimisation, and separately provide audit services. In addition, these big four firms are responsible for the evolution of accounting standards, including off-balance sheet minimisation, as well as providing advisory services to companies and Government, and they also offer auditing capabilities. Conflicts abound.

Whilst in theory audit practices should be separated from other commercial and advisory operations of the big four, I have seen examples when company account planning sessions have included cross discipline discussions, from advisory, consulting, services AND audit, to craft strategies to maximise the commercial benefits to the audit and consulting firm. This happened regularly at AA.

In addition, the audit of large companies are executed in a formulaic and superficial way, where the main test is the need to meet relevant accounting standards, not separately confirming independently that the business is functioning as advertised from a financial and compliance perspective. Who audits the auditors?

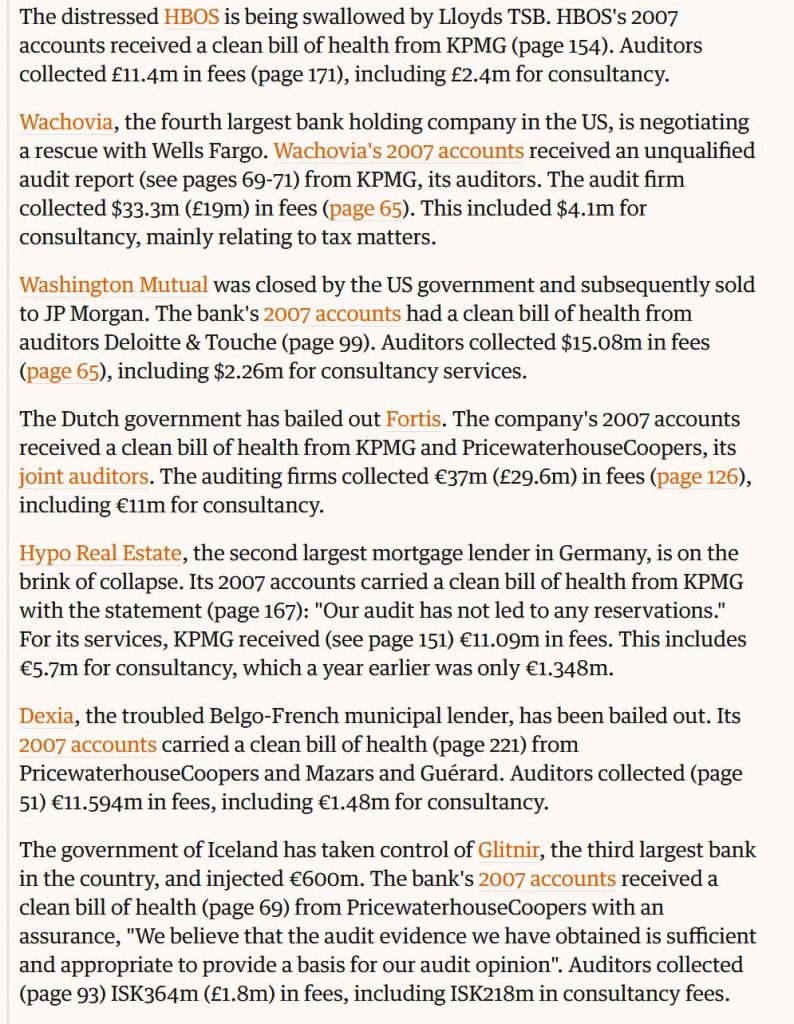

Remember that in 2008 several banks failed, despite having been given an unqualified audit in the months prior. Others required substantial Government bail-out or were absorbed by other industry players. Nothing has changed (other than the quantum of debt and other exposures have increased substantially) since then.

To illustrate the limitations of audit, I will highlight four areas, where from my research and experience current banking sector audits are deficient.

According to recent RBA data Australian banks have some $48 trillion of gross derivatives exposures. This will include services to client, but also position taking on a trading basis within the bank’s treasury operations. Recent BIS research highlighted that in a low interest rate environment, banks will tend to lend less and trade more to try to bolster profits[i]. Plus, some window-dress their books for quarter end.[ii]

Derivatives gross exposures dwarf the capital and assets held within banks. This gross exposure is not reported clearly within the accounts, because most is held off balance sheet. Moreover, the true net-exposure which a bank may face will be determined by market movements and relative trading positions. But even net exposures are not adequately reported. We only get a glimpse of the true positions (and risks) when capital is applied under the Basel rules, but this does not tell the full story, yet are within current accounting standards, and off-balance sheet rules. We see no evidence of auditors picking through the derivatives book and validating or reporting these gross exposures. In a crisis this may well hit the financial position of an individual bank, and trigger the need for a restructure, bail-in or bail-out. Current audit rules and approaches are designed to minimise disclosure and obscure the true risks. APRA does not provide an alternative route to disclose such risks.

Major banks can use their own “internal risk models” to estimate the amount of capital applied to the business, under the Basel rules. These models are complex and “tuned” by the institutions to enables institutions’ to maximise their use of capital. However, we are not convinced these models are functioning as intended, and they are not subject to regular audit, either by external auditors, or APRA. Thus, the data is taken as accurate from the “black-box” and this may lead to higher risks in the business than are disclosed. Again, the true position will not be exposed until a crisis hits.

Large financial companies hold significant portfolios of mortgages backed by residential property. An initial valuation is used in the underwriting process. However, unless there is a material refinancing event, subsequent portfolio adjustments, (because for example property prices move down) are applied only at an aggregate level (for example state level). As a result, there is a significant risk the property portfolio is overstating the real current value of the underlying security, and this may translate to bigger risks in a downturn. In addition, the amount of capital held under Basel rules could well be understated. There may be offsetting benefits in a rising market, but the standard portfolio analysis is not very accurate. But once again external auditors will be not examining the operation practices of portfolio valuations yet will sign off on the accounts as true and accurate.

Households often hold multiple loans across a lender or lenders. APRA only considers the status of individual loans. Reporting for audit purposes will be at a loan, not household level. Indeed, there are cases when loans are deliberately split to reduce the overall loan to value results. Once again this is an area where auditors will not tread, but the risks in the system are higher than those reported in the accounts. Again, the true position will not be exposed until a crisis hits.

These are just examples of pain points which the current audit processes will not adequately examine. There are many others.

The role of an auditor should be more than just checking with the accounting standards and signing off. They should be seeking out material issues, independently from management. But in the four cases above the results are wanting.

The solution would be to create an independent audit function, perhaps within the Auditor General’s domain, to provide accurate and independent analysis of large financial players. In addition, we believe that the audit functions of major firms should operate as separate service businesses and should NOT be also be allowed to offer creative accounting and off-balance sheet techniques as part of their service suite. The conflicts and limitations are obvious and concerning.

However, the true impact of such deficiencies would only be revealed in a crisis, mirroring 2008, by which time it is too late. Changing management and audit practices as suggested would place our important financial sector companies on a firming footing. Such changes could well benefit other industry sectors as well.

Changes to audit practice and structure are essential!

Martin North

Principal Digital Finance Analytics[iii]

October 2019

[i] The Real Problem With Low Interest Rates – https://youtu.be/LLUfzna5iys

[ii] https://digitalfinanceanalytics.com/blog/bis-confirms-banks-use-lehman-style-trick-to-disguise-debt-engage-in-window-dressing/

[iii] Digital Finance Analytics is a boutique research and advisory firm. More details are available via our Blog. https://digitalfinanceanalytics.com/blog/