The Australian Securities and Investments Commission (ASIC) and

Australian Prudential Regulation Authority (APRA) have committed to

strengthen engagement, deepen cooperation and improve information

sharing.

The agencies today published an updated Memorandum of Understanding (MoU).

The updated MoU follows on from the recommendations of the Royal

Commission into Misconduct in the Banking, Superannuation and Financial

Services Industry[1]. APRA and ASIC are also working closely with Government on the legislative changes required to implement these recommendations.

ASIC Chair James Shipton said the updated MoU builds on the open and

collaborative relationship across all levels of the agencies.

‘ASIC and APRA will continue to proactively engage and respond to

issues efficiently to deliver positive outcomes for consumers and

investors.

‘The MoU facilitates more timely supervision, investigations and

enforcement action and deeper cooperation on policy matters and internal

capabilities.’

APRA Chair Wayne Byres said enhanced cooperation reinforced the twin

peaks model of regulation that has operated in Australia for more than

20 years.

‘ASIC and APRA share an interest in protecting the financial

wellbeing of the Australian community and achieving a fair, sound and

resilient financial system,’ Mr Byres said.

‘Strengthening engagement is a key priority of the ASIC Commissioners

and APRA Members. We will continue to work closely together to enhance

regulatory outcomes and achieve our respective mandates.’

This MoU, which will be reviewed on a regular basis, is only one

aspect of how ASIC and APRA are establishing closer cooperation. Led by

ASIC Commissioners and APRA Members, the agencies are regularly meeting

under a revised engagement structure and working together on areas of

common interest, including data, thematic reviews, governance and

accountability. Both agencies are committed to detecting prudential and

conduct issues early and working to revolve them efficiently and

effectively.

The updated MoU is available on the ASIC website here.

The final best interests duty bill for mortgage brokers has been tabled in Parliament, outlining the role brokers need to take when helping a borrower from 1 July 2020. From The Adviser.

The amended Financial Sector Reform (Hayne Royal Commission Response—Protecting Consumers (2019 Measures)) Bill 2019 has been tabled in Parliament today (28 November).

The key features of the new law are:

mortgage brokers must act in the best interests of consumers in relation to credit assistance in relation to credit contracts;

where

there is a conflict of interest, mortgage brokers must give priority to

consumers in providing credit assistance in relation to credit

contracts;

mortgage brokers and mortgage intermediaries must not accept conflicted remuneration;

employers,

credit providers and mortgage intermediaries must not give conflicted

remuneration to mortgage brokers or mortgage intermediaries; and

the circumstances in which these bans on conflicted remuneration apply are to be set out in the regulations.

Notably,

the duty to act in the best interests of the consumer in relation to

credit assistance is a principle-based standard of conduct that applies

across a range of activities that licensees and representatives engage

in.

As such, what conduct satisfies the duty will depend on the

individual circumstances in which credit assistance is provided to a

consumer in relation to a credit contract.

The duty does not

prescribe conduct that will be taken to satisfy the duty in specific

circumstances. Instead, it is the responsibility of mortgage brokers to

ensure that their conduct meets the standard of “acting in the best

interests of consumers” in the relevant circumstances.

However, the new duty will mean that there could be circumstances

where the mortgage broker may not have acted in a consumer’s best

interests even if the responsible lending obligations were complied

with. For example, even if a home loan product is ‘not unsuitable’,

recommending it to the consumer might not be in the consumer’s “best

interests”, the accompanying documentation reads.

The penalty for breaking this duty for both credit representatives and licensees is 5,000 penalty units.

Examples of the duty in action – white label called in question

In the explanatory materials, there are examples of steps that may need to be taken for this new duty. These include:

prior to recommending any home loan product or other credit contract to a consumer based on consideration of that consumer’s particular circumstances, the mortgage broker may need to consider a range of products (including the features of those products), form a view about which products are in the consumer’s best interests and then inform the consumer of the range and the options it contains;

any recommendations made would be expected to be based on consumer benefits, rather than benefits that may be realised by the broker; that is, a broker should not recommend a loan by prioritising factors that cannot be substantiated as delivering benefits to that particular consumer (such as the broker’s relationship with the lender), over factors and features which affect the cost of the product or are more relevant to the consumer;

in cases where critical information is not obtained when inquiring about a consumer’s circumstances, the broker could be expected to refrain from making a recommendation about a loan where there is a consequent risk that the loan will not be in the consumer’s best interests.

Interestingly, the new duty also

outlines that “a broker would not suggest, from their aggregator’s

panel of lenders, a white label home loan that has the same features as a

branded product from the same lender, but with a higher interest rate,

because it would not be in the best interests of the consumer to pay

more for an otherwise similar product”.

The explanatory materials go on to outline that during a periodic review, a broker “would not suggest that the consumer remain in a credit contract without considering whether this would be in the consumer’s best interests”.

“For

example, it may be a breach of the duty if the broker suggested the

consumer remain in their current home loan when they could refinance to a

cheaper product as the broker did not want to incur the consequent

liability to the lender when their commission payments were clawed

back,” it reads.

Helping consumers understand their decision implications

The

materials also outline that there may be situations where the

consumer does not properly understand the implications of different

choices and so the broker may have to assist them to understand why a

particular loan is or is not in their best interests, which could inform

the brokers’ actions.

An example given is if a consumer asks the

broker if they should take out an interest-only home loan on a property

they are looking to buy. The home loan will have a higher interest rate

than a principal and interest home loan. The broker helps the consumer

to understand the difference in cost of the two home loans, and other

differences in the way in which they operate, including that the

consumer will only build equity if the property’s value increases or

they make additional repayments, and the implications of moving to

higher repayments at the end of the interest-only period.

Another

example is if a consumer asks the broker if they should take out a home

loan with an offset account as they have heard this can save them money,

even though the interest rate is slightly higher. The broker helps the

consumer to understand what is in their best interests, based on the

difference between the higher interest rate and the savings that

consumer could reasonably expect through utilisation of the offset

account.

Comments from Frydenberg

At the second reading this afternoon (28 November), Treasurer Josh Frydenberg said: “[T]he

bill introduces a best interests duty for mortgage brokers that will

ensure that consumers’ interests are prioritised when a mortgage broker

provides credit assistance, as regulated by the National Consumer Credit

Protection Act 2009. In practice this will mean that, in accordance

with Commissioner Hayne’s recommendations, a duty will apply in relation

to the provision of consumer credit assistance and not business

lending.

“The

government is also reforming mortgage broker remuneration, and the bill

provides for a regulation making power to this end. The regulations will

require the value of upfront commissions to be linked to the amount

drawn down by borrowers instead of the loan amount; ban campaign and

volume based commissions and payments; and cap soft dollar benefits.

“Further,

the period over which commissions can be clawed back from aggregators

and mortgage brokers will be limited to two years, and passing on this

cost to consumers will be prohibited.

“After

careful consideration, the government decided to delay consideration of

aspects of Commissioner Hayne’s recommendations for mortgage

brokers—namely moving to a borrower-pays remuneration structure. We will

be doing a review with the Council of Financial Regulators and the

Australian Competition and Consumer Commission (ACCC). That will be

carried out in three years time.

“Implementation

of these reforms, as recommended by the royal commission, is a critical

component of restoring trust and confidence in Australia’s financial

system and is part of the Morrison government’s plan for a stronger

economy.”

The government will also introduce the Financial

Sector Reform (Hayne Royal Commission Response – Stronger Regulators

(2019 Measures)) Bill 2019. The Bill implements a further four

additional commitments the Government announced at the time of

responding to the Royal Commission and will ensure that ASIC can

effectively enforce existing laws.

“The government is taking

action on all 76 recommendations contained in the Final Report of the

Royal Commission and, in a number of important areas, is going further.

Restoring trust in Australia’s financial system is part of our plan for a

stronger economy,” Mr Frydenberg said.

Broadcast on Thursday 28th November 2019, Nucleus Wealth’s Head of Investment Damien Klassen, Head of Operations Tim Fuller, and founder of Digital Finance Analytics, Martin North discuss “Australia’s Housing Market Dilemma.”

According to an article in InvestorDaily, RBA Governor Philip Lowe has poured water on the prospects of quantitative easing (QE), saying Australia “shouldn’t forget about fiscal policy” to prevent a recession.

“QE is not on the agenda at this time,” Governor Lowe told at the annual dinner of the Australian Business Economists.

Interest

rates will have to hit 0.25 per cent before the RBA considers QE –

something that economists are predicting by mid-2020. But Governor Lowe

doesn’t think QE will be necessary, saying that the Australian economy

is in a good position and that the RBA will achieve its goals.

“At

the moment, though, we are expecting progress towards our goals over

the next couple of years and the cash rate is still above the level at

which we would consider buying government securities.”

However,

Governor Lowe hinted again that he would prefer the use of fiscal policy

rather than monetary policy to ward off a recession, citing a report

from the Committee on the Global Financial System (CGFS), which he

recently chaired.

“The

report also notes that there may be better solutions than monetary

policy to solving the problems of the day,” Governor Lowe said.

“It

reminds us that when there are problems on the supply-side of the

economy, the use of structural and fiscal policies will sometimes be the

better approach. We need to remember that monetary policy cannot drive

longer term growth, but that there are other arms of public policy than

can sustainably promote both investment and growth.”

Governor Lowe

also said that the willingness of central banks to provide liquidity

could reduce the incentive for financial institutions to hold their own

adequate buffers and create an “inaction bias” from prudential

regulators or fiscal authorities.

“If this were the case, it could lead to an over-reliance on monetary policy,” he said.

The

sentiments about quantitative easing have been echoed by fund managers.

Sarah Shaw, chief investment officer at 4D infrastructure and Chris

Bedingfield, principal at Quay Global Investors have urged the

government to instead allocate investment in infrastructure to create

jobs and boost productivity.

Ms Shaw noted the need to replace

roads, bridges and other structures with better planned

“forward-thinking” infrastructure is high.

“If you think about the

need for infrastructure spend that I’m talking about, if you put a

number on it, it’s maxed at $4 trillion by 2040 of infrastructure

capacity that’s needed,” she said.

“If you think about that and

you’re in an interest rate environment as low as it is today, if you’re

not borrowing to invest in a much-needed infrastructure, then there’s

something wrong.”

She added she looks for companies that are

locking in fixed term bet to invest for future cash flows, because “now

is the time to do it” with the current low cash rate.

“Why shouldn’t countries be doing that?” Ms Shaw queried.

“I’ll

give you an example: China during the GFC, biggest form of quantitative

easing – 35,000 kilometres of high-speed rail. That’s the sort of

quantitative easing that we should be looking at here in Australia.”

VanEck has predicted there will be more rate cuts in 2020.

As discussed with John Adams in our recent post, we did not come away with the same conclusion, and Westpac, for example is forecasting QE will hit during 2020.

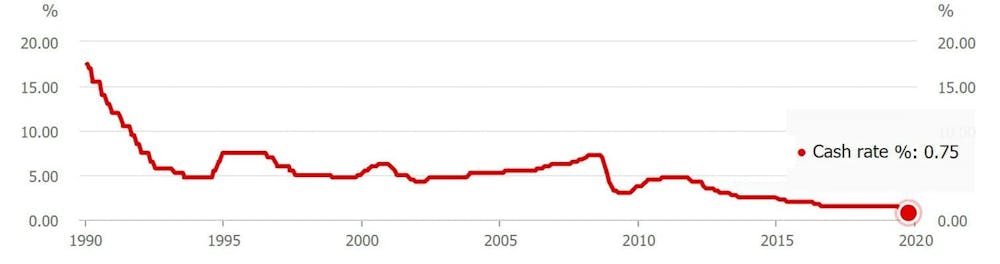

Last night, in a much anticipated speech broadcast live on the Reserve Bank’s website, Governor Phil Lowe laid out in very clear terms the circumstances in which the bank would resort to quantitative easing and the way in which it would implement it. Via The Conversation.

Quantitative easing is simply a change in the way it eases monetary policy when the official interest rate approaches zero.

Usually it does it by cutting the so-called cash rate, which is the rate banks pay each other for money deposited overnight.

Eight years ago the cash rate was 4.5%. Three years ago it was 1.5%.

After the most recent three cuts in June, July and October, it is just

0.75%

Last night, Governor Lowe said the effective lower bound was 0.25%.

Rather than let the cash rate get any lower or negative (an option he

explicitly ruled out), the bank will push down other longer-term rates

by buying government bonds.

It’s the “quantitative easing” approach adopted by the US Federal Reserve between 2009 and 2014.

Government bonds are sold by governments in return for money, a means

of borrowing. The buyer gets guaranteed interest payments and a

guarantee that their money will be returned in full after three, five,

ten or even 20 years depending on the length of the bond.

Once issued, bonds can be traded on a market, and the price at which

they change hands can be expressed as an implied interest rate, which

becomes the risk-free rate against which all other interest rates are

benchmarked.

How quantitative easing would work

Buying bonds from investors would push down that risk-free rate, pushing down the entire structure of long-term interest rates.

All other things being equal, this should also push down the exchange

rate by reducing the return on Australian dollar denominated financial

investments.

Governor Lowe indicated he might buy state government bonds as well as Commonwealth bonds.

Importantly, he argued that although the bank would be mindful of the

need to ensure private banks had enough access to the bonds they needed

to hold for regulatory purposes, those holdings would not be an

impediment to quantitative easing.

He ruled out buying residential mortgage-backed securities and other

private assets given that those markets are currently functioning well

and Reserve Bank purchases could distort them.

The approach borrows heavily from the US Fed.

As in the US, Lowe says quantitative easing would be complemented by

“forward guidance,” where the Reserve Bank would signal early how

long-term interest rates would be kept low and the circumstances in

which it expected to raise them again.

The guidance is designed to influence market expectations for future

interest rates, enhancing the effectiveness of cuts in long term

interest rates.

When it would happen

In addition to “how,” Governor Lowe spelled out “when” – the economic

circumstances in which the bank would resort to quantitative easing.

It would do it when the cash rate was at 0.25% and inflation and unemployment were moving away from its objectives.

The bank targets 2-3% inflation on average over time and has recently

identified 4.5% as the “full employment” unemployment rate.

Importantly, Lowe emphasised that the Australian economy has not yet

reached the point where a cash rate as low as 0.25% would be needed and

argued quantitative easing was unlikely to be needed in future.

The cash rate is at present 0.75%. Setting 0.25% as the effective

lower bound gives the Governor 0.5 percentage points left to cut before

implementing quantitative easing.

Implicitly, Governor Lowe is saying that those cuts of 0.5 percentage points will be enough to stabilise the economy.

A pause for a breath at 0.25%

Lowe also indicated the bank would not seamlessly transition to quantitative easing.

He implied there was an additional hurdle or threshold that would

need to be crossed, suggesting he would be reluctant to make the

transition.

His big problem is that neither inflation nor the unemployment rate are moving in the right direction.

The bank has undershot its inflation target since the end of 2014,

giving the economy a weak starting point going into an emerging global

downturn.

My research

on the US experience for the United States Studies Centre shows that

the main problem with is quantitative easing was that it was not done

soon enough or aggressively enough.

It might be better to be bold

While quantitative easing was effective, it could have been made more so had what was going to happen been made clearer.

The Fed went out of its way to limit the transmission of quantitative

easing to the rest of the economy, fearful it would be too potent and

lead to excessive inflation.

Those concerns proved misplaced. By pulling its punches, the Fed

ended up being less effective and having to pursue quantitative easing

for longer than if it had used it more aggressively.

Governor Lowe’s very obvious reluctance to go down the quantitative easing route suggests the Reserve Bank is in danger of making the same mistake, but it is not too late to learn from what happened in the US.

Author: Stephen Kirchner Program Director, Trade and Investment, United States Studies Centre, University of Sydney

The ABS released their preliminary data today. Tasmania apart, construction chain measures continue to fall. Trend estimate for residential building work done fell 3.0% this quarter and has fallen for four quarters.

The trend estimate for total construction work done fell 1.6% in the September quarter 2019.

The seasonally adjusted estimate for total construction work done fell 0.4% to $50,849.7m in the September quarter.

The trend estimate for total building work done fell 1.8% in the September quarter 2019.

The trend estimate for non-residential building work done rose 0.2% and residential building work fell 3.0%.

The seasonally adjusted estimate of total building work done fell 0.5% to $29,703.6m in the September quarter.

The trend estimate for engineering work done fell 1.1% in the September quarter.

The seasonally adjusted estimate for engineering work done fell 0.2% to $21,146.2m in the September quarter.

Trend percentage change: Total construction

The trend estimate for total construction work done fell 1.6% this quarter and has fallen for five quarters.

Trend percentage change: Engineering

The trend estimate for engineering construction work done fell 1.1% this quarter and has fallen for six quarters.

Trend percentage change: Building

The trend estimate for total building work done fell 1.8% this quarter and has fallen for four quarters.

Trend percentage change: Residential

The trend estimate for residential building work done fell 3.0% this quarter and has fallen for four quarters.

Trend percentage change: Non-residential

The trend estimate for non-residential building work done rose 0.2% this quarter and has risen for five quarters.

Chain volume measures – Trend estimates

New South Wales Victoria

Construction work done in New South Wales has fallen for four quarters.

Construction work done in Victoria has fallen for four quarters.

Queensland

Western Australia

Construction work done in Queensland has fallen for six quarters.

Construction work done in Western Australia has fallen for eight quarters.

South Australia

Northern Territory

Construction work done in South Australia has fallen for five quarters.

Construction work done in the Northern Territory has fallen for eight quarters.

Tasmania

Australia Capital Territory

Construction work done in Tasmania has risen for seven quarters.

Construction work done in the Australian Capital Territory has fallen for four quarters.

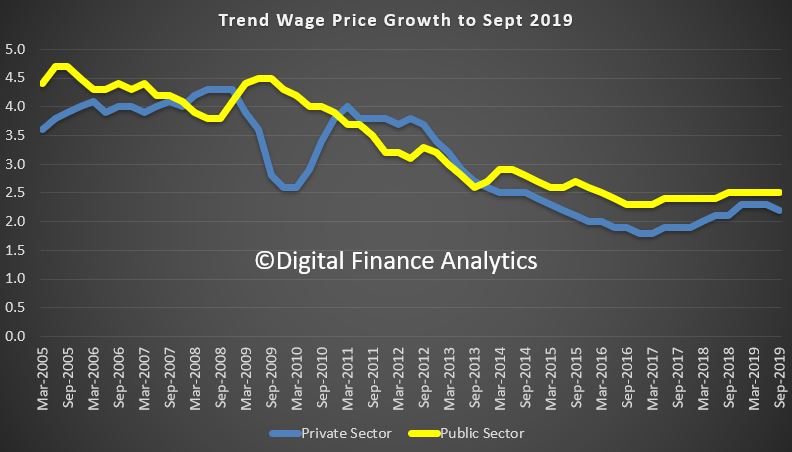

In the RBA’s Governor’s speech last night there was a reference to lower wages growth for longer, referring back to an earlier outing by Guy Debelle, Deputy Governor.

Debelle’s speech at Australian Council of Social Service (ACOSS) National Conference revealed at least to me that the RBA has no real idea as to why wages growth is so slow. They appear to have all but accepted it will be so. ” This increase in labour supply has meant that the strong employment outcomes in recent years has not generated the pick-up in wages growth that might otherwise have occurred. At the same time, I have highlighted the increased prevalence of wages growth in the 2s across the economy”.

We think the structural changes to the labour market (gig jobs, part-time work, multiple-jobs, etc) plus technological changes and globalisation all have a role to play. And the migration factors and temporary working visas are also playing into the mix. Finally, the balance between employee and employer seems to have shifted. Public sector wages are a little stronger.

He said: Over much of the past three years, employment has grown at a healthy annual pace of 2½ per cent. This has been faster than we had expected, particularly so, given economic growth was slower than we had expected. Employment growth has also been faster than the working-age population has been growing. As a result, the share of the Australian population employed is around its all-time high, which is a good outcome. Normally, we would have expected this strong employment growth to lead to a decline in the unemployment rate. But the unemployment rate has turned out to be very close to what we had expected and has moved sideways around 5¼ per cent for some time now.

So what is going on here? Strong employment growth but little change in the unemployment rate means

that the strength in labour demand has been met by strong growth in labour supply. This increase in

labour supply has come from more people joining the labour force and from some of those with jobs

putting off leaving the labour force. These trends have been particularly pronounced for females aged

between 25 and 54 and older workers of both sexes.

The surprising strength in labour supply has been one of the factors that has contributed to wages

growth being slower than we had expected. But at the same time, the lower growth in wages has probably

contributed to the strength in employment growth. My undergraduate honours thesis at Adelaide Uni

examined the aggregate labour demand curve in Australia which was a much debated topic at the time.[1] So more

than 30 years on, I will discuss similar issues today.

I will look at the rise in participation rates of females and older workers and discuss some of the

factors that have been contributing to it. I will also look briefly at what jobs have been created. In

doing so, I will make use of the micro data in the monthly labour force survey (LFS) as well as micro

data from the HILDA survey.[2] That is, we are examining the micro data to understand the macro trends in the

labour market.

By and large, the new jobs created over the past few years have been representative of the existing

stock of jobs. There have been low wage and high wage, lower skilled and higher skilled jobs created,

but about average on both counts. The jobs growth has been in household services jobs such as health

care, social assistance and, education, as well as in business services. Two-thirds of the employment

growth over the past two years has been in full-time jobs.

Then I will look at wages growth and show that the lower average wage outcomes of the past few years

have reflected the increased prevalence of wages growth in the 2s across the economy.

Finally, I will look forward and talk about the RBA’s forecasts for the labour market. Two of the

critical influences on that forecast are how much further labour supply will increase and how entrenched

are wage outcomes.

Participation

An increase in the number of people in employment can be met either by an increase in people entering

from outside the labour market or a decline in unemployment. The increase in people coming from outside

the labour force, causing an increase in the participation rate, is known as an ‘encouraged

worker’ effect – when economic conditions improve, there is a tendency for people to enter

or defer leaving the workforce.[3] Historically more of the increase in employment has translated into a reduction

in the unemployment rate than by a rise in the participation rate.

However, the past couple of years have been unusual. The increase in employment has been met

disproportionately by an increase in the number of people participating in the labour force

(Graph 1). The share of the population participating in the labour force is at a record high. The

two main groups contributing to this rise in participation are females and older workers. I will discuss

each of these in turn and some of the forces driving the outcomes over both the recent past and from a

longer perspective. An understanding of these forces can help us assess how much further these trends

are likely to continue.

Graph 1

Female participation

Female employment growth has accounted for two-thirds of employment growth over the past year. The

female participation rate is now at its highest rate, and the gap between female and male participation

is now the narrowest it has ever been (Graph 2).

Graph 2

The female participation rate has steadily increased over recent decades (from 40 per cent in

1970 to 61 per cent in 2019), and a similar upward trend is evident across other advanced

economies. Changing societal norms and rising educational attainment have contributed to more women

moving into paid employment or employment outside the home. Female participation has also been

influenced by the increasing flexibility of working-time arrangements, the availability and cost of

child care and policies such as parental leave.

Nearly half of employed females work part time, often to care for children. Over recent decades, the

participation rate of mothers with dependent children has trended higher, rising by 10 percentage

points since the early 2000s to 73 per cent. Over the past decade, the rise in participation

has been most pronounced for mothers with children aged between 0 and 4 (Graph 3). Of those

returning to work within two years after the birth of a child, an increasing majority are citing

‘financial reasons’ as their main reason for doing so. Other mothers returning to work

cite ‘social interaction’ or to ‘maintain career and skills’ as their main

reason. Financial reasons could be capturing a number of different considerations including low income

growth, the rise in household debt or child care costs.

Graph 3

Research suggests the cost and quality of child care does have a significant effect on the labour

supply of women.[4] Data from the HILDA survey show that the share of households using formal child care

for young children has increased notably over the past decade (Graph 4). However, access to child

care places and financial assistance with child care costs remain ‘very important’

incentives for females currently outside the labour force.

Graph 4

Another factor that is linked to higher rates of female participation over recent decades is the

increase in the level of mortgage debt of home owners (Graph 5). The rise in debt levels has

broadly coincided with the increase in the participation rate of females. However, it is difficult to

establish which way causality is going. Are debt levels higher because more households have two incomes

and can afford to borrow more? Or does the need to borrow more to afford housing drive the decision to

participate more? Or is it the case that the low level of income growth in recent years has meant that

households have more debt than they anticipated and need to work longer to pay it down? Research to

establish causality has usually found some evidence of a causal relationship running from higher debt

levels to higher participation.[5] However, the analysis indicates that the effects are not that large at an

aggregate level.

Graph 5

The rollout of the National Disability Insurance Scheme (NDIS) may also have encouraged increased

participation of female carers. We know from a detailed survey of NDIS participants and their families

that parents of those with disabilities work fewer hours on average and are more likely to be in casual

employment.[6] It is probably too early in the rollout of the scheme to see a material increase in the

number of parents re-entering the labour market. The survey suggests there has been a slight increase in

the average number of hours worked since the start of the scheme, but the percentage of families/carers

of NDIS participants who wanted to work more hours has not changed.

Thus two significant drivers of the increase in participation rates of females aged between 25 and

54 over a long period of time are child care costs and other financial factors. The open question

is how much more the participation rate of this group will rise.

Older workers

The share of the Australian population aged between 15 and 64 years has continued to decline,

and is expected to continue to decline. This is due to the ongoing transition of baby boomers into

retirement ages. All else being equal, an ageing population will result in a fall in the supply of

labour, since the generation retiring is larger than the generation entering the workforce. But there

has been a long-term trend for each cohort to participate more than previous cohorts did at the same

age. That trend has accelerated recently, and more than offset the effect of ageing on its own. The

share of 55 year olds and older that are employed is 35 per cent, compared to

22 per cent 20 years ago.

This cohort effect is particularly clear in the third panel of Graph 6. The much larger rise in

female participation than males over the past two decades is a stark illustration of the effect, as the

other drivers of participation in this age group should have similar influences on both male and female

participation.

Graph 6

Why are older people working longer?[7] One contributing factor is improved health. People are

working longer because they can, both because of their own health and also because the nature of work

has changed over the years towards services and away from manual work, which means most people are in

less physically demanding jobs.

It used to be the case that many older workers would have to choose between working full time and

retiring. From a labour economics point of view, the labour/leisure trade-off has much more choice than

it used to.[8] In the past, it was often an all or nothing decision. As the labour market has become

more flexible over recent decades, older workers may be able to reduce their hours but still participate

in the labour market. Indeed, around one-third of workers aged 55 years and older are working part

time, with over half doing so because they prefer to do so. The ABS Retirement and Retirement Intentions

survey suggests that of people aged 45 years and older, around one-third of workers intend to cut

down from full-time work to part-time work as they get older.

As people live longer, they may want to work longer voluntarily, depending on the value they get from

working. But they also may need to work longer to achieve the necessary income to support the standard

of living they would like in retirement.

Access to a retirement pension or superannuation is a very significant element in the decision to

retire. More than half of all retirees over 60 cite that reaching retirement age or becoming

eligible for the pension/superannuation as the main reason they retired from work. The male

participation rate begins to decline around age 50 and there is a noticeable change in the rate of

decline around 65; the historical pension age for men. For women there is a similar pattern, although in

the past there was also a change in the rate of decline around age 60.

Accordingly, announced and actual increases in pension ages are also likely to have contributed to

increased participation. This has been documented in the past for females after the government increased

the female pension age from 60 to 65 between 1996 and 2013 (in 6 month increments every

2 years).[9]

Currently the pension age is being raised to 67 years for both sexes; a process that began in

2017. The average age of job leavers over the age of 55 has increased slightly in recent years. Our

analysis of LFS micro data provides tentative evidence that the 2017 changes to the pension age had an

impact on workers’ retirement decisions. The participation rate of those born in 1952 and 1953 (who

were affected by the changes in 2017) does not decline as quickly when they turned 65, compared to the

earlier cohort groups that were not affected by the pension age increase.[10] In

aggregate, this analysis suggests that the pension changes boosted the participation rate by around

0.1 percentage point.

As I said above, some older workers are working for financial reasons. As we all know, one of the major

considerations for those contemplating retirement is their wealth and ability to fund their retirement.

Increasing house prices and share prices over much of the last decade are likely to have reduced

participation of older individuals.[11] The recent decline in house prices may have resulted in

some individuals delaying their retirement and not withdrawing their labour supply. However, the price

declines were modest compared to the earlier increase, so that those considering retirement would have

experienced a net gain in house prices and a decline in their debt.

Similar to females, the rise in the participation rate of persons aged 55 years or older is also

likely to have been related to developments in household debt. Over recent decades there has been a

trend towards greater indebtedness for these persons. The proportion of older households with

owner-occupied home loans has risen from around 20 per cent in the early 2000s to around

37 per cent today. The increase in debt has also been associated with a change in the

retirement intentions of older workers. Over time, the gradual shift towards later retirement has been

more noticeable for those with debt (Graph 7). As with the female participation story, there is a

question of causality. Are people working later in life because they have an unexpectedly high level of

debt? Or had they always intended to work longer and hence were more willing to borrow more and carry

more debt later in life?

Graph 7

To draw this together, participation rates have risen as employment has grown over the past three

years. This increase in supply has been unexpected, so it is important to try to understand what is

driving it to have some sense on how much further these trends are likely to run. The two major shifts

in participation have been amongst females aged 25–54 and older workers. These trends have

been there for a while and have been even stronger recently. I have presented some of the insights from

our analysis of various micro data sources but there is still more to understand. We will continue to

focus on this given its importance to the outlook, which I will come to later.

Employment

What sort of jobs have been created in recent years?

Some have assumed that the jobs that have been created in recent years are lower-skilled or lower-paid

jobs. However, when we break down the occupation-level data by skill type or pay level, this is not the

case. The strongest growth in employment over the past decade has been in highest-skilled (as defined by

the ABS) jobs. There has also been solid growth over the same period in lower-skilled jobs

(Graph 8). Similarly, the growth in employment has been broadly distributed across the pay spectrum

(Graph 9).

Graph 8

Graph 9

Another often stated view is that much of the job creation in recent years has been in the public

sector, rather than the private sector. According to the Labour Account data, the number of jobs created

in the private sector has far outnumbered the number of jobs created in the public sector

(Graph 10).[12] Private sector job creation has been particularly strong in health care and education

(which is partly, but a long way from entirely, due to government spending in these areas),

but also in business services and industries like construction and hospitality.

Graph 10

We have also used the micro data to look at the people that have moved into some of these growth areas.

For example, the share of employment in the health care & social assistance industry has increased

from 9 to 13 per cent over the past decade. Those entering or leaving health care and

social assistance tend to do so from a small number of other industries such as public administration,

support services, education and training and other services into health care and social assistance.

Around 10 per cent of people entering employment from outside the labour market are moving

into health care, while a slightly smaller share move into this sector from unemployment. A large share

of workers between the age of 55 and 69 years of age work in health care and social

assistance, so this is likely to be related to individuals delaying retirement.

Wages

Wages growth has declined noticeably since around 2012. As wages growth has fallen, the distribution of

wages growth has also become increasingly compressed. This fall in the dispersion in wages growth across

jobs mainly reflects a sharp fall in the share of jobs receiving ‘large’ wage rises. The

Bank has highlighted this previously, but I will update that analysis and illustrate the increased

pervasiveness of wage outcomes between 2 and 3 per cent across the labour market.[13]

The share of jobs that experience a wage change of more than 4 per cent has fallen from over

one-third in the late 2000s to less than 10 per cent of jobs in 2018 (Graph 11). Given

that firms are also unwilling or unable to reduce wages, this has meant that the vast majority of wage

growth observations in the labour market are now tightly clustered in the range of

0–4 per cent.

Graph 11

There is growing evidence to suggest that wage adjustments of 2 point something per cent have

now become the norm in Australia, rather than the 3–4 per cent wage increases that were

the norm prior to 2012. The rising prevalence of wage outcomes in the 2s can be seen in the official

data and in the Bank’s liaison with firms.

One notable example is the large increase in the share of enterprise bargaining agreements that provide

annual wage rises in the 2–3 per cent range. The share of such agreements has risen

from around 10 per cent over the 2000s to almost 60 per cent in 2019

(Graph 12). Over the same period, the proportion of agreements providing wage increases of

3 per cent or more has fallen sharply.

Graph 12

A similar picture emerges when we look at the job-level data that underlie the ABS’s wage price

index (WPI). These data, which also provide insights on wage outcomes for jobs where pay is set

according to individual arrangements, also show that the share of jobs getting wage rises in the

2–3 per cent mark has risen noticeably. The Bank’s liaison with firms also

confirms that the share of firms reporting wages growth of between 2 and 3 per cent has

increased to around 45 per cent in recent years. Prior to 2012, fewer than one in

10 firms were reporting wages growth in this range.

Another way to see this shift in wage setting over time is to look at the median rates of

wages growth across all jobs in the labour market (Graph 13). Unlike the mean, the median is less

affected by the large decline in ‘large’ wage rises in recent years and the changing

prevalence of wage freezes. Prior to 2012, median wages growth was firmly anchored at

4 per cent. In recent years, median wages growth has fallen to 2½ per cent, and

has remained at that level.

Graph 13

Different measures of wages growth capture slightly different concepts of labour costs. The WPI, which

is one of the main measures that the Bank monitors, tracks wage outcomes of individual jobs over time,

rather than tracking particular employees.[14] This feature of the WPI makes it useful for gauging

developments in wages growth after abstracting from any changes in the nature of work or the composition

of employment. However, this feature also means that the WPI does not capture wage rises that come from

getting promoted or changing firms.

But other surveys suggest that promotions can be a key source of earnings growth for individuals. On

average, a promotion leads to a 5 per cent boost in hourly wages, which is comparable to the

wage rise a worker gets when switching firms. Since 2012, there has been a broad-based decline in the

proportion of employees that are getting promoted at work or switching jobs (Graph 14). This means

that a smaller fraction of the workforce are receiving these wage rises.

Graph 14

Why have wage outcomes in the 2s become so prevalent?[15] One phenomenon that could explain it is the

well-known tendency for workers to resist reductions to their wages in real terms.[16] This

phenomenon, also known as ‘downward real wage rigidity’, leads to a clumping of

employees’ nominal wage changes in the vicinity of their expected rate of inflation, particularly

when nominal wages growth is tracking at a low level. In that sense, the RBA’s inflation target of

2–3 per cent on average over time provides a strong nominal anchor in wage

negotiations. When my colleagues looked at the job-level WPI data they did find evidence of a clumping

of wage outcomes either at, or just above, expected inflation.

While wage increases in the 2s have become very common for many employees, those whose wages are set

according to an award have generally been receiving wage increases in excess of 2 per cent in

recent years. This reflects the Fair Work Commission adjustments, which have provided support to wages

growth at the lower end of the skill distribution, given the prevalence of award-reliant jobs in this

part of the labour market. Wages growth for the least-skilled jobs has outpaced all other skill groups

since around 2013. This contrasts with the commodity price boom period, when wages growth was strongest

for higher-skilled jobs. Consistent with this, the ratio of average hourly earnings of award-reliant

employees to those of other employees has risen since 2012, largely reversing the falls seen in the

earlier period.

Outlook

The recent Statement on Monetary Policy provided the Bank’s latest forecasts for the

labour market and wages growth. GDP growth is forecast to gradually increase over the next couple of

years, which should result in a small decline in the unemployment rate from its current rate of

5¼ per cent. As Graph 15 shows, there is always uncertainty around that central

forecast. One of the key sources of uncertainty currently around the outlook for the unemployment rate

as well as wages growth, is whether labour supply will be as responsive to labour demand as it has been

in recent years. That is, will the expected increase in labour demand encourage as much participation as

it has most recently? How much further do some of these drivers of increased participation for older and

female workers have to run? That is a difficult question to answer.

Graph 15

The dynamics of participation and unemployment flows will have an important bearing on wages growth as

well as household income growth. We expect wages growth to remain largely unchanged at its current level

over the next couple of years.

Why don’t we think wages growth will pick up over the next couple of years? What we know from our

liaison program is that the proportion of firms expecting stable wages growth in the year ahead is

around 80 per cent and only around 10 per cent anticipate stronger wages growth. Of

those firms expecting stable wages growth, the share reporting wage growth outcomes of

2–3 per cent has steadily risen over time. This supports the case that lower wage rises

have become the new normal (Graph 16).

Graph 16

Recently there has been a rise in the proportion of new EBAs with a term of three years or more. The

lower wages growth incorporated in those agreements suggests that wages growth of around

2½ per cent for EBA-covered employees will persist for longer than in the past.

The more wages growth is entrenched in the 2s, the more likely it is that a sustained period of labour

market tightness will be necessary to move away from that. At the same time, I don’t think there is

much risk in the period ahead that aggregate wages growth will move any lower.

Conclusion

Today I have provided an overview of the current state of play in the labour market and the Bank’s

expectation about how it might evolve in the period ahead. I have highlighted some of the key forces

that have shaped these developments, in particular, the rise in the participation rates of female

workers and older workers. The Bank is trying to understand what has been driving these macro

developments using some newly available micro data sources. This greater understanding should help

inform our outlook for the labour market.

This increase in labour supply has meant that the strong employment outcomes in recent years has not

generated the pick-up in wages growth that might otherwise have occurred. At the same time, I have

highlighted the increased prevalence of wages growth in the 2s across the economy. A gradual lift in

wages growth would be a welcome development for the workforce and the economy. It is also needed for

inflation to be sustainably within the 2–3 per cent target range.

NAB has announced it will be taking part in the government’s first home loan deposit scheme, operational from 1 January 2020. Via Australian Broker.

The bank has been selected by the National Housing Finance and Investment Corporation (NHFIC) to offer mortgages under the scheme.

“We are proud to be chosen to partner with the federal government and

NHFIC,” said Mike Baird, NAB chief customer officer of consumer

banking.

“Every year our bankers help more than 15,000 Australians achieve

their dream of owning their first home. This scheme is a fantastic way

of helping even more customers, allowing them to potentially save

thousands of dollars on their mortgage.”

The scheme will provide 10,000 eligible Australians per year access

to a home loan with a deposit of as little as 5%. To implement the

scheme, the NHFIC will contract with a panel of selected lenders rather

than having direct contact with borrowers.

Before offering the guaranteed loans, lenders will need to update

their internal systems and train front-line lending staff on how to

apply the scheme eligibility criteria alongside regular considerations,

such as loan serviceability.

The NHFIC has communicated key considerations in its selection of

lender partners includes the loan products on offer, including interest

rates and other fees, as well as the quality of the customer experience.

According to Baird, NAB is the only major to have a special rate for

first homebuyers, which is currently 2.88% fixed for two years. The

major bank also emphasised it will not charge eligible customers higher

interest rates than equivalent customers outside of the scheme.

“We see this appointment as a great endorsement of NAB’s home loan

offering and our support of Australians looking to buy their own home

for the first time,” said Baird.

Before the scheme is live in the new year, customers are able to check their potential eligibility on the NHFIC website.