The Australian Prudential Regulation Authority (APRA) has

announced that it will proceed with proposed changes to its guidance on the

serviceability assessments that authorised deposit-taking institutions (ADIs)

perform on residential mortgage applications.

In a letter to ADIs issued today, APRA confirmed its updated

guidance on residential mortgage lending will no longer expect them to assess

home loan applications using a minimum interest rate of at least 7 per cent.

Common industry practice has been to use a rate of 7.25 per cent.

Instead, ADIs will be able to review and set their own minimum interest rate floor for use in serviceability assessments and utilise a revised interest rate buffer of at least 2.5 per cent over the loan’s interest rate.

APRA received 26 submissions after commencing a consultation in May on proposed amendments to Prudential Practice Guide APG 223 Residential Mortgage Lending (APG 223). The majority of submissions supported the direction of APRA’s proposals, although some respondents requested that APRA provide new or additional guidance on how floor rates should be set and applied.

Having considered the submissions, Chair Wayne Byres said APRA believes its amendments are appropriately calibrated.

In the prevailing environment, a serviceability floor of more than seven per cent is higher than necessary for ADIs to maintain sound lending standards. Additionally, the widespread use of differential pricing for different types of loans has challenged the merit of a uniform interest rate floor across all mortgage products,” Mr Byres said.

“However, with many risk factors remaining in place, such as high household debt, and subdued income growth, it is important that ADIs actively consider their portfolio mix and risk appetite in setting their own serviceability floors. Furthermore, they should regularly review these to ensure their approach to loan serviceability remains appropriate.”

Mr Byres said: “The changes being finalised today are not intended to signal any lessening in the importance APRA places on the maintenance of sound lending standards. This updated guidance provides ADIs with greater flexibility to set their own serviceability floors, while maintaining a measure of prudence through the application of an appropriate buffer that reflects the inherent uncertainty in credit assessments.”

The new guidance takes effect immediately.

Copies of the letter and the updated APG 223 are available on the APRA website here.

Like Australia, New Zealand is consulting on the capital requirements for its top banks, to mitigate their risk of failure. The Reserve Bank of New Zealand (RBNZ) received 160 industry submissions in the last round of consultation, including contributions from Australia’s major banks with Westpac voicing “significant concerns” around the advantages that could be handed to non-banks. Via AustralianBroker.

The submission not only highlighted the significant opportunity

created for non-banks by increasing the regulation on traditional banks,

but indicated that the changes would unfairly inhibit its participation

in the market.

It reads, “As the costs of credit rise, these [non-bank] alternatives

become more attractive to New Zealanders. And as digital capability

evolves to maturity, the potential for such models to emerge, and emerge

quickly, has increased materially.”

Westpac’s submission drilled down yet further, going on to question

the wisdom of instituting regulation “with the potential to re-ignite

the shadow banking system”.

“Should the capital requirements…increase, it creates an incentive

for other lenders outside of the registered banking system to provide

credit, because they can do so more cost effectively.

“The RBNZ’s proposals…may support the emergence of unregulated, less

capitalised entities which, as we have seen in past cycles, can weaken

the stability of the whole financial system.”

NAB communicated similar concerns in its response.

Its submission says that the steady increase in “regulatory burden”

being put on banks is responsible for over half (55%) of the growth

evidenced in the non-bank sector between 2007-2017, a statistic

attributed to Xavier Vives.

According to NAB, the conversation around competition is particularly

important given that New Zealand is operating on an open data system,

which allows consumers to move their transactions between institutions

with ease.

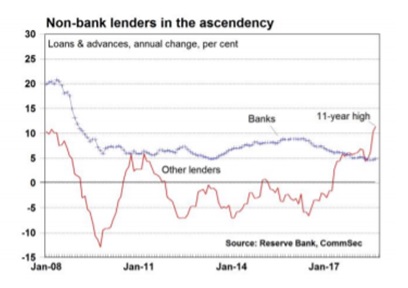

Crucially, this means there could be many lessons for Australia to take from New Zealand’s experience. As of October 2018, lending growth in Australia’s non-bank sector was occurring at a rate over 11% annually, the strongest since October 2007 according to RBA and CommSec data (see graph). Further, stage one of open banking launched on Monday and proposed revisions to the capital framework for ADIs are expected to go into effect from 1 January 2022, following another round of consultation.

Property Expert Joe Wilkes and I discuss the latest rule changes in New

Zealand, which impacts investment property – changes which the MSM media

have missed, so far.

Apartment owners in high-rise units are realising their properties are worth less than they paid for them as rampant oversupply and falling demand send real estate values plummeting. Via RealEstate.com and The Daily Telegraph.

Recent sales figures indicated multiple unit owners made a loss on

their investments, with some apartments in high rise buildings selling

for up to $150,000 below what the sellers paid.

Such sales were particularly prevalent in construction hubs such as the suburbs of North Ryde and Rosehill, near Parramatta.

The suburbs were among the few Sydney areas where average prices have

fallen below what they were in 2014, according to research from

CoreLogic.

Multiple units in this complex on Allengrove

Crescent in North Ryde have sold at a loss for the sellers, including

one for $150K less than the vendor paid.

Median unit prices in the suburbs were 2-5 per cent cheaper than they were five years ago.

Median prices in other suburbs with a high supply of new units such

as Hillsdale, in the Botany area, and inner west suburb Lewisham were

below their 2016 levels, along with Zetland and Kellyville.

Suburbs with such deep drops in prices remained rare considering real

estate values skyrocketed in the years between 2013 and 2017.

The Property Council of Australia believes a number of economic challenges remain for Australia’s property industry, despite new data showing increased confidence in the sector for the first time in 12 months, via The Recon Daily.

The latest ANZ/Property Council Survey for the September 2019 quarter

shows that industry confidence has picked up by 13 index points,

improving in all states and territories, except for the ACT.

Property Council of Australia Chief Executive Ken Morrison

said while there had been a series of positive developments within the

market since the election, residential construction activity was set to

continue its decline, impacting jobs and the economy.

“Following the federal election, we have had a quadrella of positive

policy news which translated into a strong sentiment bounce,” he said.

“These are very welcome steps and have led to much stronger

expectations of national economic growth and the availability of credit.

“However, the property sector is not immune from the challenges

facing the rest of the economy and a number of state governments have

just embarked on a range of investment-sapping tax increases.

“State budgets in Queensland, Victoria and South Australia have hit

the property industry with arbitrary and poorly designed tax increases

which will hurt investment and job creation, and risk undermining the

current sentiment turnaround.”

ANZ Head of Australian Economics, David Plank, said there had

been emerging signs of stability in the residential property market

across the past three months.,

“In particular, we noted the pace of house prices declines was

slowing and that the auction clearance rate was beginning to rise,” he

said.

“Over the past month lower interest rates, the proposed change to the

interest rate floor by the regulator, and the removal of uncertainty

around the impact of the possible tax policy changes have boosted

sentiment toward housing.

“The results of the latest ANZ/Property Council Survey capture this

shift, with most parts of the survey showing material improvement.”

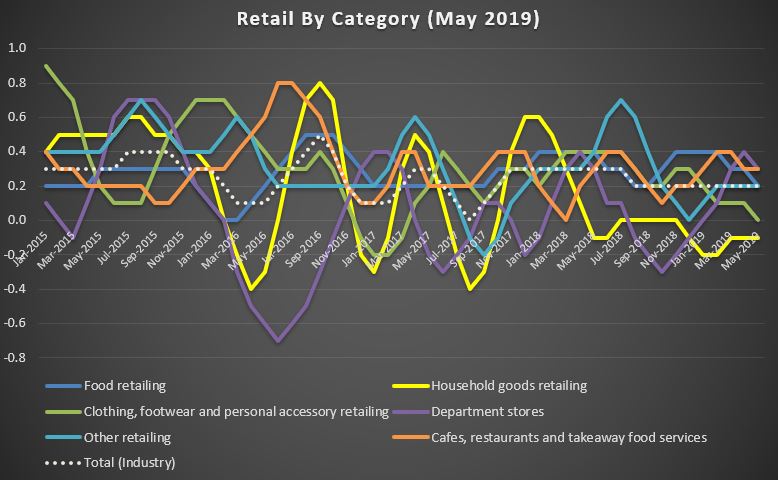

The trend estimate rose 0.2% in May 2019. This follows a rise of 0.2% in April 2019, and a rise of 0.2% in March 2019.

The seasonally adjusted estimate rose 0.1% in May 2019. This follows a fall of 0.1% in April 2019, and a rise of 0.3% in March 2019.

In trend terms, Australian turnover rose 2.7% in May 2019 compared with May 2018.

The following industries rose in trend terms in May 2019: Food retailing (0.2%), Cafes, restaurants and takeaway food services (0.3%), Other retailing (0.2%), and Department stores (0.3%). Clothing, footwear and personal accessory retailing (0.0%) was relatively unchanged. Household goods retailing (-0.1%) fell in trend terms in May 2019.

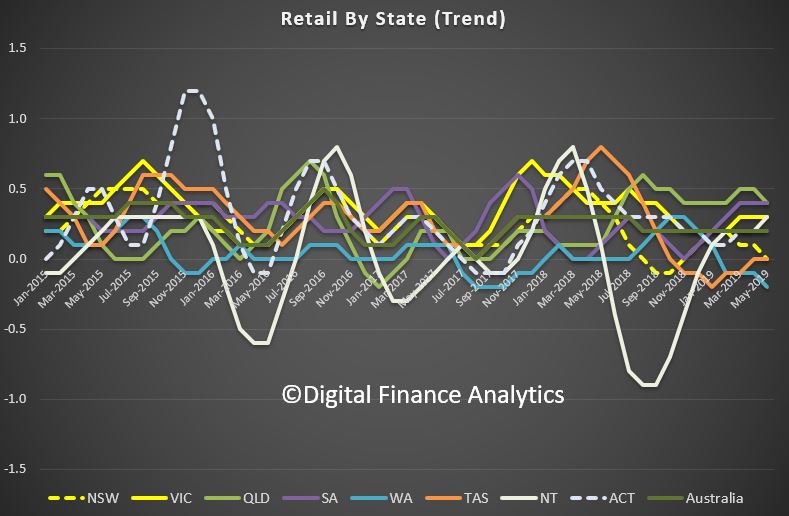

The following states and territories rose in trend terms in May 2019: Queensland (0.4%), Victoria (0.3%), South Australia (0.4%), the Northern Territory (0.3%), and the Australian Capital Territory (0.2%). New South Wales (0.0%) and Tasmania (0.0%) were relatively unchanged. Western Australia (-0.2%) fell in trend terms in May 2019.

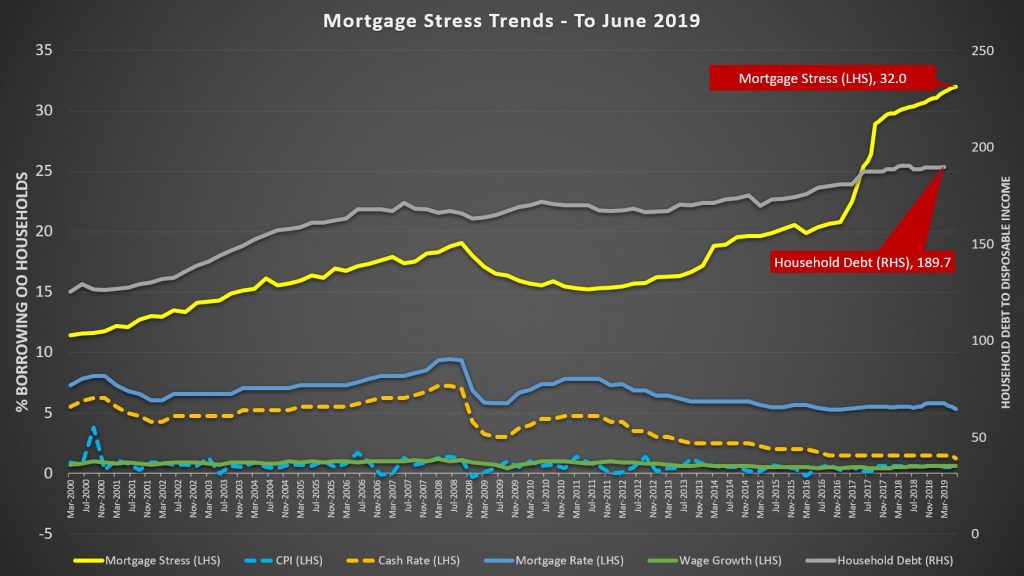

We have released the June 2019 mortgage stress results, based on our running 52,000 household surveys. We found that 32% of households are now dealing with mortgage stress, a record, meaning they are having cash flow issues managing their finances and mortgage repayments.

This translates into more than 1,063,000 households spread across the country, and nearly 71,000 risk default in the year ahead, even taking into account the fall in mortgage repayments represented by the recent rate cuts. Banks loses will rise.

This is because the costs of living continue to run ahead of incomes, while households have larger debts (and are being enticed to buy in the current complex risk environment).

The top post codes in stress are those in the outer suburban fringe areas, where many large estates are still being built, and households are super-highly leveraged.

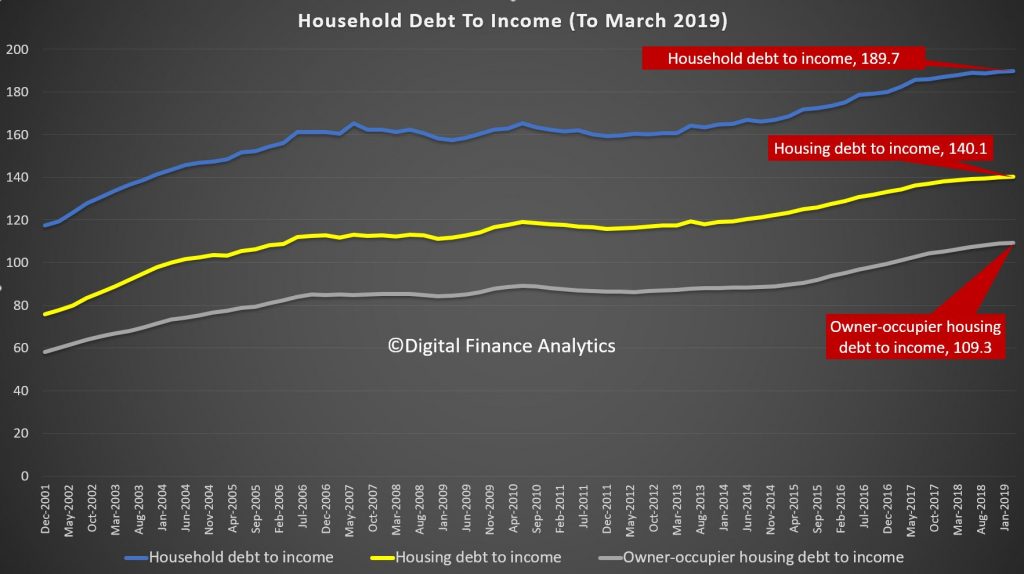

The RBA released their March 2019 data on household ratios. Whilst these series include small business finance, and include households not borrowing, the trends continue to tell the story of debt, and more debt.

The household debt to income ratio is at a record 189.7, while the housing debt to income ratio was 140.1, again a record and the owner occupied housing debt to income ratio was also up, to 109.3. These are high numbers, on a trend and international comparable basis. Households are drowning in debt.

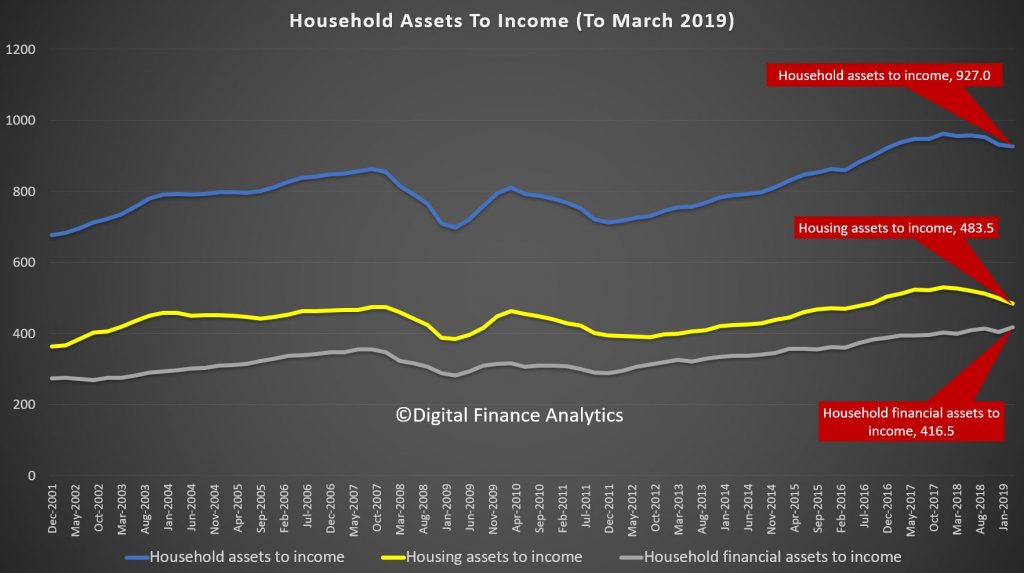

However the asset to income ratios tell another story. As home prices have fallen, so the ratio has decreased, assets are down relative to income. The exception are financial assets, which benefited from the rise in stock prices this year.

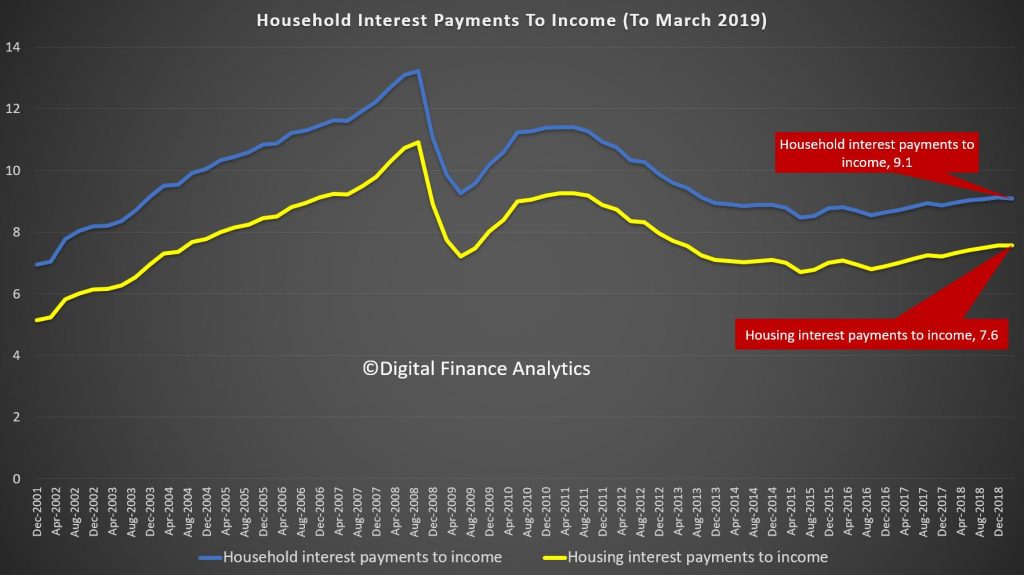

The ratio of interest to income continues to rise because households are borrowing at a faster rate than their incomes are growing, helped of course by lower interest rates. This ratio is below that before the GFC because rates have dropped. And this is the one ratio spruikers turn to to defend the high debt levels – but it is myopic, and going in the wrong direction.

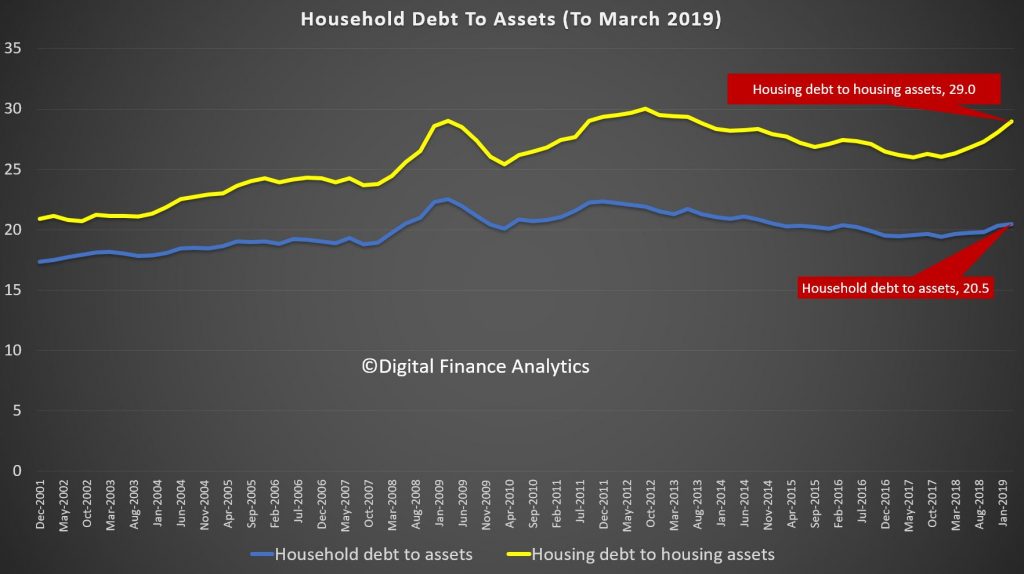

Finally, the RBA data debt to assets shows the pincer movement as home prices fall, and debt rises. This is now heading towards the highest we have seen.

The obvious conclusion is that the debt burden is too great, mortgage stress will go on rising, until the balance between debt and income is restored.

The recent loosening of lending standards simply pours more fuel on the fire. Households are being used a canon fodder in the vein attempt to keep the faltering economy afloat.

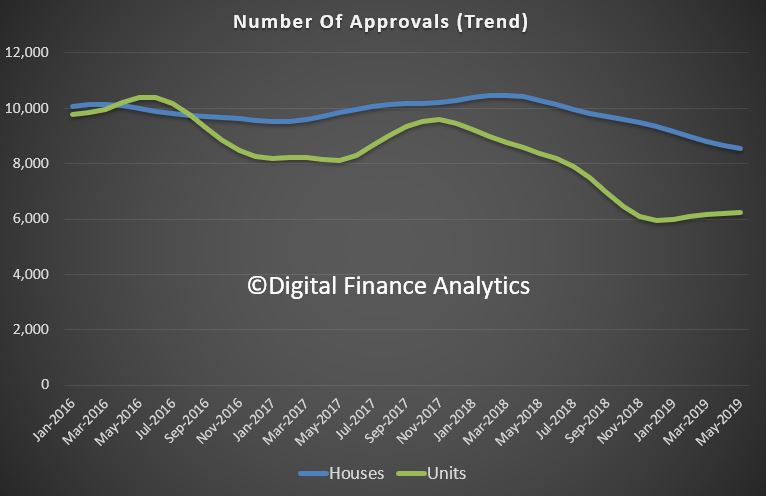

As you know DFA uses the trend series in our analysis and modelling.

However, most reports will pick the seasonally adjusted series and claim a “rebound” in approvals.

In fact, on both trend and seasonally adjusted measures, private sector house approvals fell, by 1.3% in trend terms and 0.3% in seasonally adjusted terms.

On the other hand, private sector dwellings excluding houses rose 0.6% in trend terms. while the seasonally adjusted estimate rose 1.2%.

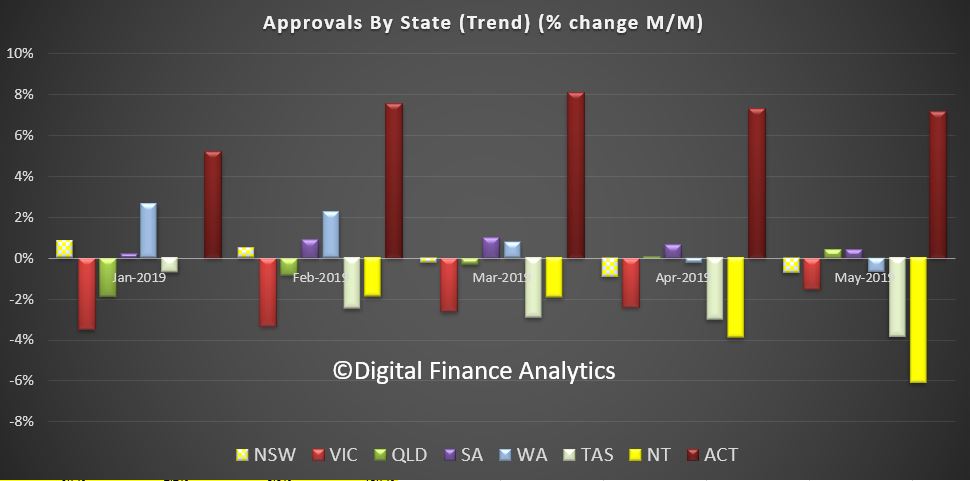

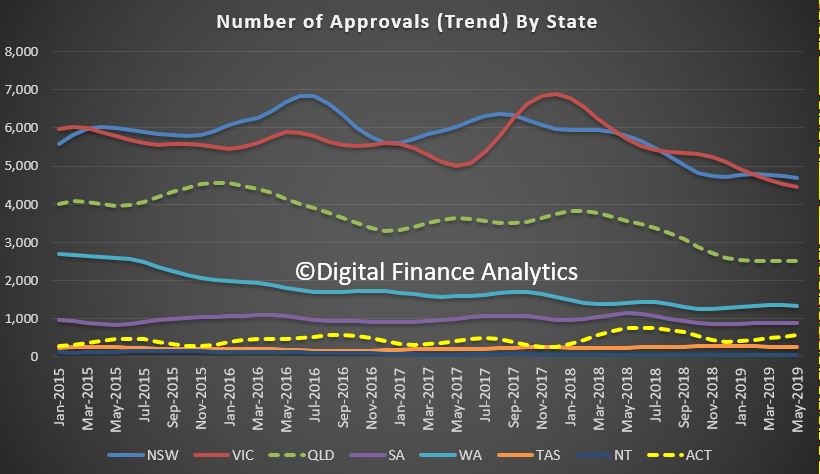

Across the states, total approvals rose a little in Queensland and South Australia, together with a big hike in Canberra (on small volumes), while there was a percentage fall in New South Wales and Victoria, as well as Western Australia and the Northern Territories.

The volume trends really highlight the declines in New South Wales and Victoria, which are not offsetting the small rises elsewhere, especially in the ACT.

In New South Wales the trend estimate for total number of dwelling units approved fell 0.7% in May, while the number of private sector houses fell 2.9%.

In Victoria the trend estimate for total number of dwelling units approved fell 1.5% in May, while the number of private sector houses fell 1.3%.

In Queensland, the trend estimate for total number of dwelling units approved rose 0.4% in May, while the number of private sector houses fell 0.1% in May.

And in South Australia, the trend estimate for total number of dwelling units approved rose 0.4% in May, while the number of private sector houses was flat in May.

Finally, In Western Australia, the trend estimate for total number of dwelling units approved fell 0.7% in May and the number of private sector houses fell 0.7% in May.

The trend estimate of the value of total building approved fell 0.2% in May and has fallen for three months. The value of residential building fell 0.6% and has fallen for 16 months. The value of non-residential building rose 0.3% and has risen for nine months.

The seasonally adjusted estimate of the value of total building approved fell 0.2% in May. The value of residential building rose 4.7%, while the value of non-residential building fell 6.7%.

The HIA said “The decline in dwelling approvals appears to be losing momentum. This is a welcome reprieve for the housing industry after the persistent declines measured throughout 2018”.

“Recent positive news relating to house prices and new home sales has started filtering through. Even if this isn’t the bottom of the cycle the pick-up in new home sales in May suggests the pace of decline is slowing”.

Westpac said ” Overall the May update was a touch firmer than expected but the detail was not great with clear questions around the sustainability of the gain in high rise approvals and weakness elsewhere”.

That is closer to the mark. Little here, yet to argue for a shift in gears.

As Westpac put it ” All of this still predates several positive developments for housing, in particular: the Federal election result, which has removed the threat of tax policy changes around negative gearing and capital gains tax; and the RBA’s interest rate cuts in June and July. More timely market measures suggest wider housing market conditions have improved, especially in Sydney and Melbourne. We suspect that shift will be slow to flow through to new dwelling construction with an overhang of stock in some segments and financing issues likely to continue restraining activity near term.

Certainly the major markets of Sydney, Melbourne and Brisbane all have a way to go before we can claim a rebound, and of course there is a significant oversupply of new high-rise under construction in these centres, despite the worries about construction standards, and the disappearing indemnity insurance in the sector.

To be a registered surveyor with the Victorian Building Authority (VBA) a person must have professional indemnity insurance, without any exemptions.

The same rule applies in NSW and Queensland.

But insurance companies are no longer providing this option and the industry is warning work on buildings may simply stop.

Other surveyors have reported that the cost of their insurance premiums and excesses have more than quadrupled.

Building surveyors are responsible for signing off on buildings, including building permits and occupancy permits.

While local government building surveyors can also sign off on permits, private building surveyors have been the preferred option for most of the building industry.

The chief executive of the Australian Institute of Building Surveyors, Brett Mace, warned the building industry could start to slow down over the next year.

“We think it’s a huge crisis,” Mr Mace said.

“If building surveyors are unable to be registered then you’re not going to be able to provide approvals and the construction industry will come to a stop.”

The Master Builders Association (MBA) said up to 30 per cent of building surveyors are required to renew their insurance by the end of June.

“If they are unable to obtain insurance or the insurance offered to them is non-compliant due to exclusions being imposed, many building projects could come to a standstill,” the MBA said in a statement.

One more reason to be cautious about a lift in approvals ahead.

At the time of writing, cuts of 25bps had been announced by Resimac, State Custodians and Athena Home Loans. Reduce Home Loans cut its rates by 22bps, taking its lowest advertised rate to 2.89% and putting the lender in the sub 3% category with Greater Bank, HomeStar Finance and BOQ.

Unlike last month’s cut, all the majors responded to the RBA’s announcement before the day’s end.

As with last month, ANZ was the first

to react, announcing a full 25bps decrease across all variable interest

rates for Australian home and residential investment loans.

In June, ANZ elected to pass through just 18bps of the RBA’s 25bps

cut, defying Treasurer Josh Frydenberg’s public demand for a full

transference of the reduction.

CBA was next to go public, opting for a 0.19% reduction across both

its owner occupied and investor P&I standard variable rate home

loans.

The interest only home loans, both owner occupied and investment, received the full 25bps cut.

Last month, CBA passed through the 0.25% cut in full.

The bank also announced a special five-month term deposit rate for

savers, introduced at 2.20% per year, which is a 0.20% increase.

“With official interest rate settings already at record lows, we are

focused on balancing the benefits and the costs of further interest rate

reductions between our 1.6 million home loan and over 6 million savings

customers,” said Angus Sullivan, group executive of retail banking

services.

“It is not possible to pass on the full rate reduction to over $160

billion of our deposits, including deposits where interest rates are at

or already near zero,” he added.

In June, NAB also passed through the full 25bps. However, this month

they elected to reduce variable home loan interest rates by 19bps, but

also provided more commentary along with the decision than the other

majors.

“Decisions like these are difficult and reflect the current unique

circumstances, with home loan rates at record lows at the same time as

deposit and savings rates also being at record lows,” said chief

customer officer of consumer banking, Mike Baird.

“The difference between what we charge and how much it costs us to

fund a mortgage remains under pressure and while the circumstances of

each RBA cash rate decision will vary and has some influence on the cost

of borrowing money, it is not the only funding cost driver for NAB.”

“Getting the balance right is an ongoing challenge for banks and,

with 9 million customers, making the right decisions for our customers

matters for the Australian economy,” he explained.

Westpac rounded out the responses yesterday evening, announcing a

reduction of 20bps for variable rates including owner occupier paying

P&I, investment p&I, and owner occupier for interest only

customers.

The rate was reduced by 0.30% for residential investment property

loans for customers for customers with interest only repayments.

In June, Westpac reduced rates for owner occupiers paying P&I by

just 0.20%, and rates for investor customers with interest only payments

by 0.35%