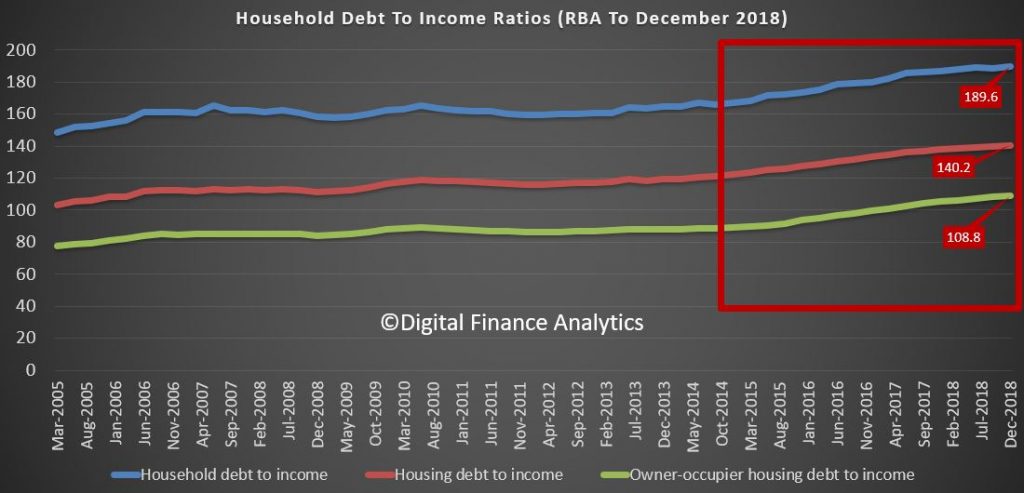

In the latest RBA data series (E2) we get an update on household debt to income and debt to asset ratios, and they are ALL moving in the wrong direction. This is to December 2018.

The household debt to income moved higher to a new record of 189.6, and housing debt to income to a new record of 140.2.

The change in trajectory from 2014/5 is significant, as lending standards were weakened, and interest rates cut (forcing home prices higher).

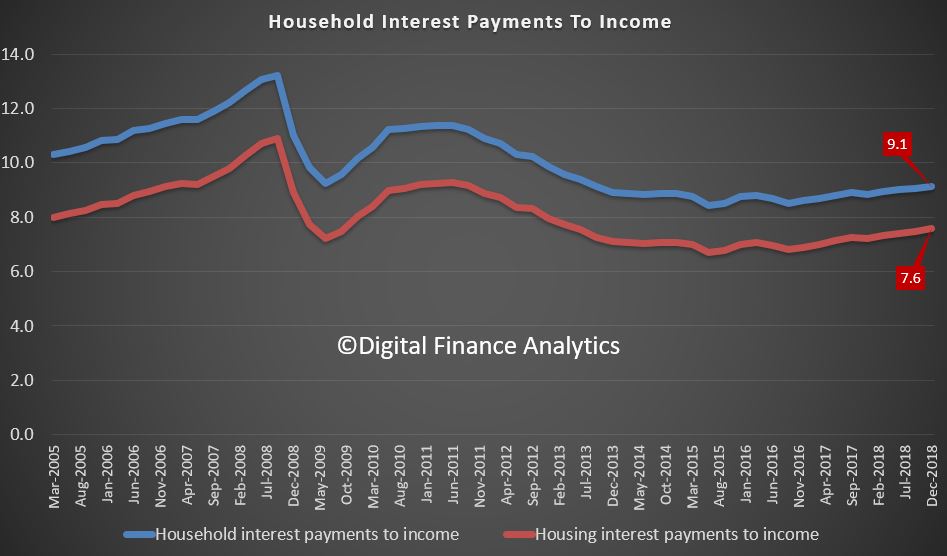

The interest payments to income also rose, thanks to bigger mortgages, slightly higher interest rates, and little income growth.

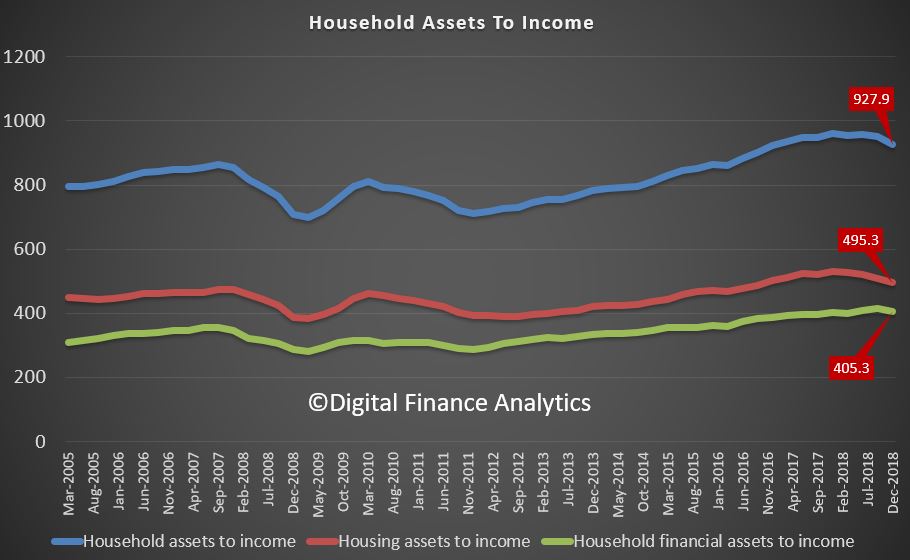

But in contrast, the asset values are falling, so the asset to income ratios are falling. Housing assets in particular are dropping.

All pointing to a higher burden of debt on households. And remember only one third, or there about, have a mortgage, so in fact the TRUE ratios are much much worst. But the trends do not lie in relative terms, and by the way these are extended ratios compared with most western economies. We are drowning in rivers of debt!

The federal government has announced a $600 million fighting fund to support the recommendations of the financial services royal commission, via InvestorDaily.

Buried

on page 167 of the hefty 2019 Federal Budget are the Hayne-related

expenses to be incurred by Treasury over the next five years.

The

government will provide $606.7 million over five years from 2018-19 to

facilitate its response to the Royal Commission into Misconduct in the

Banking, Superannuation and Financial Services Industry.

The

package comprises a suite of measures that fulfil the government’s

commitment to take action on all 76 of the recommendations of the Royal

Commission’s Final Report, including:

•

Designing and implementing an industry funded compensation scheme of

last resort for consumers and small business ($2.6 million over two

years from 2019-20);

•

Providing the Australian Financial Complaints Authority with additional

funding to help establish a historical redress scheme to consider

eligible financial complaints dating back to 1 January 2008 ($2.8

million in 2018-19);

•

Paying compensation owed to consumers and small businesses from legacy

unpaid external dispute resolution determinations ($30.7 million in

2019-20);

•

Resourcing the Australian Securities and Investments Commission (ASIC)

to implement its new enforcement strategy and expand its capabilities

and roles in accordance with the recommendations of the Royal Commission

($404.8 million over four years from 2019-20).

• Resourcing

the Australian Prudential Regulation Authority (APRA) to strengthen its

supervisory and enforcement activities which will support its response

to key areas of concern raised by the Royal Commission, including with

respect to governance, culture and remuneration ($145.0 million over

four years from 2019-20);

•

Establishing an independent financial regulator oversight authority, to

assess and report on the effectiveness of ASIC and APRA in discharging

their functions and meeting their statutory objectives ($7.7 million

over three years from 2020-21);

•

Undertaking a capability review of APRA, which will examine its

effectiveness and efficiency in delivering its statutory mandate, as

well as its capability to respond to the Royal Commission ($1.0 million

in 2018-19);

•

Establishing a Financial Services Reform Implementation Taskforce

within the Treasury to implement the Government’s response to the royal

commission, and co-ordinate reform efforts with APRA, ASIC and other

agencies through an implementation steering committee ($11.2 million in

2019-20); and

•

Providing the Office of Parliamentary Counsel with additional funding

for the volume of legislative drafting that will be required to

implement the Government’s response to the Royal Commission ($0.9

million in 2019-20).

The

cost of this measure will be partially offset by revenue received

through ASIC’s industry funding model and increases in the APRA

Financial Institutions Supervisory Levies and from funding already

provisioned in the Budget.

Lower taxes

Handing

down the Federal Budget 2019-2020 in parliament last night, Mr

Frydenberg said that the budget would restore the nation’s finances

without raising taxes.

“The

budget is back in the black and Australia is back on track,” the

treasurer said, announcing that the coalition delivered a $7.1 billion

surplus.

“Over

the last year the interest bill on national debt was $18 billion,” he

said. “We are reducing the debt and this interest bill, not by higher

taxes, but by good financial management and growing the economy.”

The government has announced immediate tax relief for low- and middle‑income earnersof up to $1,080 for singles or up to $2,160 for dual income families to ease the cost of living.

The coalition will also be lowering the 32.5 per cent rate to 30 per cent in 2024-25,

increasing the reward for effort by ensuring a projected 94 per cent of

taxpayers will face a marginal tax rate of no more than 30 per cent.

“The

Australian Government is lowering taxes for working Australians and

backing small and medium‑sized business, while ensuring all taxpayers,

including big business and multinationals, pay their fair share,” the

treasurer said.

Superannuation

The

Government will allow voluntary superannuation contributions (both

concessional and non-concessional) to be made by those aged 65 and 66

without meeting the work test from 1 July 2020. People aged 65 and 66

will also be able to make up to three years of non-concessional

contributions under the bring-forward rule.

Those

up to and including age 74 will be able to receive spouse

contributions, with those 65 and 66 no longer needing to meet a work

test.

“This measure is estimated to reduce revenue by $75.0 million over the forward estimates period,” the treasurer said.

“Currently,

people aged 65 to 74 can only make voluntary superannuation

contributions if they self-report as working a minimum of 40 hours over a

30 day period in the relevant financial year. Those aged 65 and over

cannot access bring-forward arrangements and those aged 70 and over

cannot receive spouse contributions.”

The

government will make permanent the current tax relief for merging

superannuation funds that is due to expire on 1 July 2020.

“This

measure is estimated to have an unquantifiable reduction in revenue

over the forward estimates period,” Mr Frydenberg said.

Since

December 2008, tax relief has been available for superannuation funds

to transfer revenue and capital losses to a new merged fund, and to

defer taxation consequences on gains and losses from revenue and capital

assets.

The

tax relief will be made permanent from 1 July 2020, ensuring

superannuation fund member balances are not affected by tax when funds

merge. It will remove tax as an impediment to mergers and facilitate

industry consolidation, consistent with the recommendation of the

Productivity Commission’s final report into the superannuation industry.

The

treasurer said consolidation would help address inefficiencies by

reducing costs, managing risks and increasing scale, leading to improved

retirement outcomes for members.

The government will also

reduce costs and simplify reporting for superannuation funds by

streamlining some administrative requirements for the calculation of

exempt current pension income (ECPI).

The

Government will allow superannuation fund trustees with interests in

both the accumulation and retirement phases during an income year to

choose their preferred method of calculating ECPI.

The

Government will also remove a redundant requirement for superannuation

funds to obtain an actuarial certificate when calculating ECPI using the

proportionate method, where all members of the fund are fully in the

retirement phase for all of the income year.

This measure will start on 1 July 2020 and is estimated to have no revenue impact over the forward estimates period.

FSC has mixed feelings

The

Financial Services Council (FSC) welcomed the government’s

superannuation changes to reduce red tape and improve access to

voluntary contributions.

“The

expansion of the work test exemption, spouse contributions and

bring-forward arrangements will provide workers nearing retirement

greater flexibility to make additional super contributions if they are

able. The electronic requests for release of super and simplification of

exempt current pension income calculations are sensible and welcome,”

FSC chief executive Sally Loane said.

“The

FSC also supports the tax relief for merging super funds, as this will

help the superannuation industry consolidate to reduce costs and improve

member outcomes.”

However,

the FSC is disappointed this is not part of a comprehensive product

rationalisation scheme, despite this being a longstanding government

commitment.

“A lack of reform in this area means consumers are locked into older, more expensive products,” Ms Loane said.

The FSC is pleased to note the Budget has largely kept the superannuation settings unchanged. However, Ms Loane said the council

is disappointed the government has failed to reform non-resident

withholding tax for managed funds in the Asia Region Funds Passport.

“This

means Australia will remain uncompetitive in our region, and Australia

will not be competing with Asian funds on a level playing field.

“The

withholding tax on managed funds raises little money, but harms our

competitiveness within Asia, putting Australia’s fund managers at a

major competitive disadvantage in the region.”

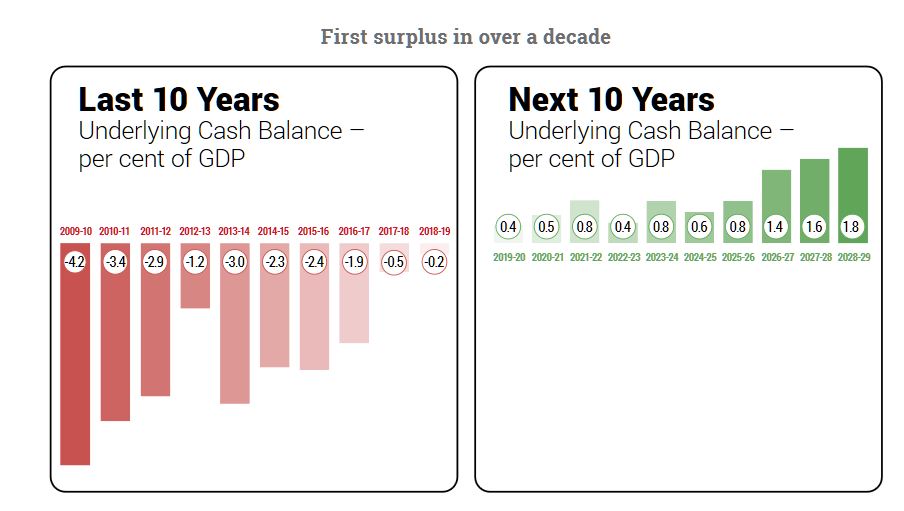

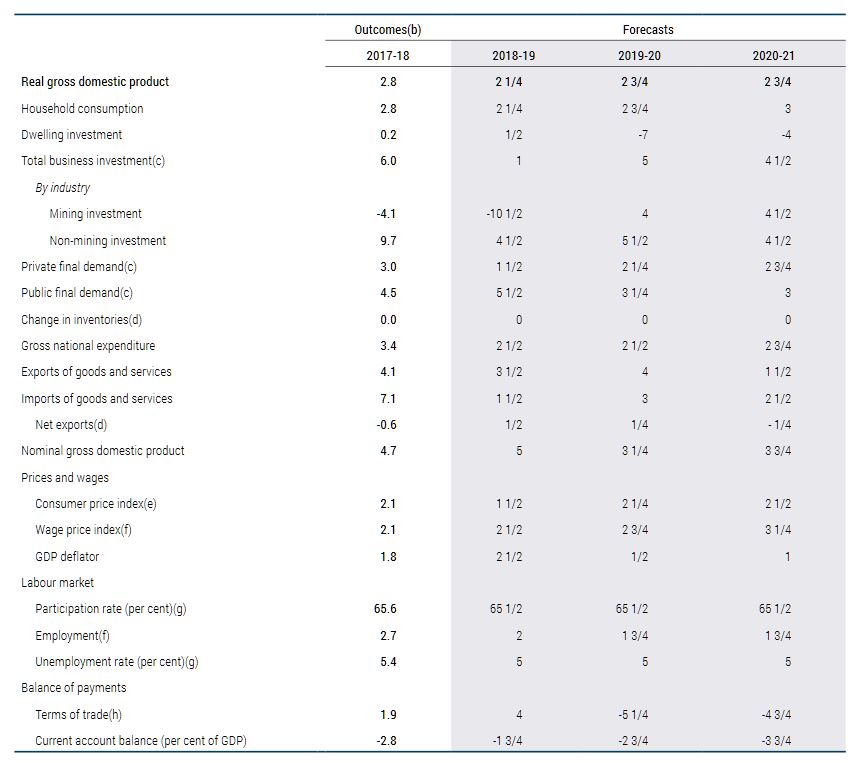

The Treasurer Josh Frydenberg has given his budget speech tonight, and he said that for the first time in 12 years the federal budget has returned to surplus.

His first budget includes billions of dollars for tax cuts, major road upgrades and health care. But actually, it is due to return to surplus in the NEXT financial year, and project small surpluses in subsequent years.

He is also spending big ahead of the election, so yes this is political (and in some regards intimating Labor’s policies in places) . This is a “boots and all” approach to try and gain election ground. Reminds me of Howard and Costello!

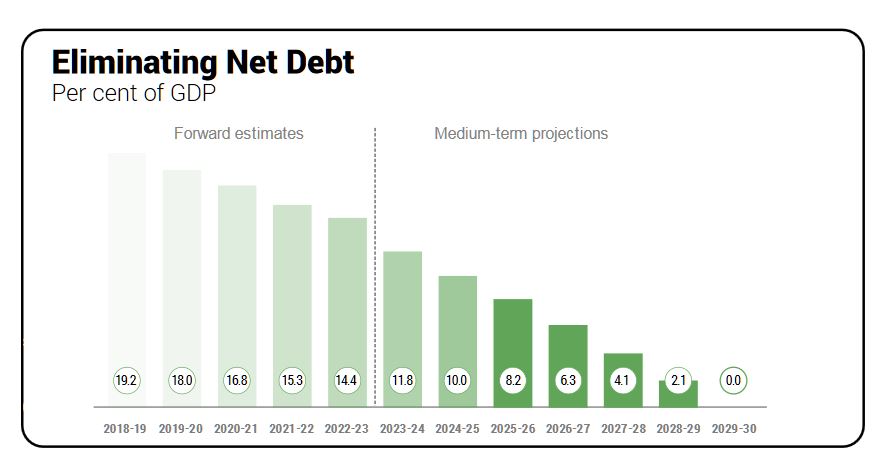

Net debt is forecast to be $360 billion next financial year, but the Coalition is promising to eliminate it by 2030 if it retains government (if the aggressive assumptions and no slow-down occurs in that time).

But it forecasts lower wages growth, then a jump back to higher rates (why?) and the same is true of economic growth at 2.75% next year, then higher later. Plus a promise for another 1.25 million jobs in the next 5 years (what type of jobs?).

“The budget is back in the black and Australia is back on track,” the treasurer said, announcing that the coalition delivered a $7.1 billion surplus

The Budget forecasts surpluses in each year over the forward estimates, reaching as high as $17.8 billion in 2012-22.

But the budget recognizes a number of risks locally and internationally and is under-funding the NDIS by $3 billion in the next two years.

“The residential housing market has cooled, credit growth has eased and we are yet to see the full impact of flood and drought on the economy.”

The mantra though the speech was that the budget would restore the nation’s finances without raising taxes.

“We are reducing the debt and this interest bill, not by higher taxes, but by good financial management and growing the economy.”

The truth is the budget may go into surplus next year thanks to very high iron ore export prices to China. This was lucky, and is explained by supply disruption from other sources lifting prices.

He makes the point that Australia has a significant national debt which is currently costing $18 billion, and this with interest rates ultra low!

Last year the coalition had announced plans to reduce income taxes for Australians by $144 billion. Now the Treasurer said the government would deliver more than $150 billion in income tax cuts.

From 1 July 2024 taxes will be reduced from 32.5 per cent to 30 per cent for those earning between $45,000 and $200,000.

“Taxes

will always be lower under the coalition,” Mr Frydenberg said, adding

that small businesses will also get tax relief from the 2019 budget.

“Small

business taxes have been reduced to 25 per cent and the instant asset

write-off will be increased from $25,000 to $30,000 and can be used

every time and asset under that amount is purchased.

“The instant asset write-off will also be expanded to businesses with a maximum turnover of $50 million.”

The coalition will also boost infrastructure spending to $100 billion over the next ten years.

Finally, the Government has matched Labor’s commitment to end a freeze on the Medicare rebate for GP visits from the first of July, as part of a $1.1 billion primary healthcare plan.

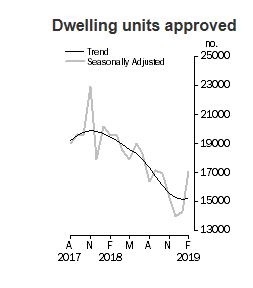

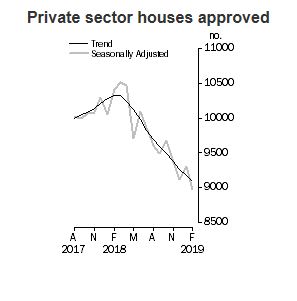

A rise in building approvals for apartments and townhouses has driven a 0.4 per cent increase in the total number of dwellings approved in Australia in February 2019, in trend terms, according to data released by the Australian Bureau of Statistics (ABS) today.

“Building approvals for private dwellings excluding houses rose 2.6 per cent in February.” said Justin Lokhorst, Director of Construction Statistics at the ABS. “Meanwhile, private houses fell a further 0.8 per cent”.

Among the states and territories, total dwelling approvals rose in February in New South Wales (3.1 per cent) and Western Australia (2.0 per cent), in trend terms. Falls were recorded in the Northern Territory (6.5 per cent), the Australian Capital Territory (6.3 per cent), Queensland (2.0 per cent), South Australia (1.1 per cent) and Victoria (0.8 per cent). Tasmania was flat.

Declines in approvals for private houses were recorded in New South Wales (2.0 per cent), Victoria (1.1 per cent) and Queensland (0.8 per cent), while increases were recorded in South Australia (2.0 per cent) and Western Australia (0.5 per cent).

In seasonally adjusted terms, total dwellings rose by 19.1 per cent in February, largely driven by rises in Victoria (37.3 per cent) and New South Wales (25.2 per cent). Private dwellings excluding houses rose 64.6 per cent, while private houses decreased by 3.6 per cent.

The value of total building approved rose 1.3 per cent in February, in trend terms. The value of non-residential building rose 1.9 per cent, while residential building increased 0.8 per cent.

The fall in residential property values is “losing steam” but could be reinvigorated by changes in the political and economic landscape, according to CoreLogic, via The Adviser.

The latest Hedonic Home Value Index from Property research group CoreLogic has

revealed that, in the month to 31 March 2019, national home values

dropped by 0.6 per cent, driven by a 0.6 per cent drop across

Australia’s combined capital cities and a 0.4 per cent fall across

combined regional locations.

The sharpest reported fall was in

Sydney (0.9 per cent), followed by Melbourne (0.8 per cent), Brisbane

and Darwin (0.6 per cent), Perth (0.4 per cent) and Adelaide (0.2 per

cent).

Hobart was the only capital city to report growth, with

dwelling values rising by 0.6 per cent, while prices in Canberra

remained stable.

Reflecting on the results, CoreLogic’s head of

research, Tim Lawless, said that the downturn could be “losing some

steam”, with the pace of falls slowing month-on-month.

However,

Mr Lawless added that the scope of the downturn has become “more

geographically widespread”, with monthly declines reported across six of

Australia’s eight capital cities and across most “rest of state”

regional locations.

Mr Lawless stated that the outlook for the

housing market continues to be plagued by uncertainty related to the

federal election, lending policies and domestic economic conditions.

Specific

reference was made to the federal Labor opposition’s proposals to limit

negative gearing to new housing and halve the capital gains tax

discount to 25 per cent.

“Federal elections generally cause some

uncertainty, which is likely amplified more so this time around

considering the potential for a change of government, which will also

involve significant changes to taxation policies related to investment,”

he continued.

“No doubt, some prospective buyers and sellers are

delaying their housing decisions until after the election; however,

there is no guarantee that certainty will improve post-election,

considering the impact of a wind back to negative gearing and halving of

the capital gains tax concession is largely unknown.”

Mr Lawless said that he expects Labor’s proposed changes to exacerbate the downturn in the housing market.

“It

seems a reasonable assumption that removing an incentive from the

market would result in some downwards pressure on activity and prices

for a period of time,” he said.

Credit availability was also cited as a source of continued uncertainty, with Mr Lawless pointing to the fall in the value of housing finance commitments, particularly in the owner-occupied space – as reported by the Australian Bureau of Statistics.

“The

value of owner-occupier lending is around 2.6 times the value of

investor lending, so the substantial drop in owner-occupier mortgage

commitments perhaps explains why the housing downturn is becoming more

widespread,” he said.

“The value of owner-occupier housing finance

commitments (excluding refinancing) was down 17.1 per cent compared

with January last year and investment credit was 24.6 per cent lower.”

Mr

Lawless said that monetary policy movements could help stimulate credit

demand but noted that tighter lending standards would limit the effect

of lower interest rates.

“While any cuts to the cash rate may

not be passed on in full, a lower cost of debt will provide some

positive stimulus for the housing market,” he said.

“Arguably,

this stimulus won’t be as effective as previous interest rate cuts due

to the high serviceability buffer applied to borrowers, whereby lenders

are still required to assess serviceability at a mortgage rate of at

least 7 per cent despite mortgage rates which are now available around

the 4 per cent mark or even lower.”

According to CoreLogic’s

research, the national median home price currently sits at $524,149,

with the median value across the country’s combined capital cities at

$597,860, and $376,728 across combined regional locations.

ANZ CEO Shayne Elliott has told a parliamentary inquiry that banks triggered the credit downturn impacting the supply of housing finance, via InvestorDaily.

Softening

conditions in the credit and housing space has sparked debate among

market analysts regarding the cause of the downturn, with some

stakeholders, including governor of the Reserve Bank of Australia (RBA)

Phillip Lowe claiming that the “main story” of the downturn is one of

“reduced demand for credit, rather than reduced supply”.

Mr Lowe claimed that falling property prices have deterred borrowers, particularly investors, from seeking credit.

According

to the Australian Prudential Regulation Authority’s latest residential

property exposure statistics for authorised deposit-taking institutions,

new home lending volumes fell by $25.1 billion (6.5 per cent) over the

year to 31 December 2018. The decline was driven by a sharp reduction in

new investment lending, which dropped by $17.7 billion (14 per cent),

from $126.9 billion to $109.2 billion over the same period.

However,

the ANZ CEO has told the House of Representatives’ standing committee

on economics that he believes the downturn in the credit space has been

primarily driven by the tightening of lending standards by lenders off

the back of scrutiny from regulators and from the banking royal

commission.

Liberal MP and chair of the committee Tim Wilson

asked: “Is the reported credit squeeze more demand-driven by borrowers

pulling back or supply-driven by banks being more conservative?”

To

which Mr Elliott responded: “This is a significant question that’s

alive today, and there are multiple views on it. I can’t portion between

those two.

“I’m probably more in the camp that says conservatism

and interpretation of our responsible lending obligations and others

has caused a fundamental change in our processes, and that has led to a

tightening of credit availability.

“It’s a little bit ‘chicken and

egg’,” Mr Elliott added. “If people find it a little bit harder to get

credit, they might step back from wanting to invest in their business or

buy a home, so I think they’re highly correlated, but I do think banks’

risk appetite has had a significant impact.”

Mr Elliott said

that “vagueness and greyness” regarding what’s “reasonable” and “not

unsuitable” as part of the responsible lending test have left the law to

the interpretation of lenders.

“Unfortunately, we haven’t always

had the benefit of a significant amount of precedence or court rulings

on some of those definitions, so we’ve done our best,” he said.

“I

think the processes recently, the questions that this committee has

asked, the questions in the royal commission, have started a debate, not

just with the regulators but with the community about what is the real

definition of [responsible] lending.”

He added: “As a result of

that, we’ve become more conservative in our interpretation, and so we’ve

tightened up, [and some] Australians will find it a little bit harder

to either get credit or get the amount of credit that they would have

otherwise had in the past or would like.

“I’m not suggesting for a minute that it’s wrong, it’s just the reality.”

In an article on Livewire, John Abernethy from Clime Asset Management really goes to town on monetary policy, saying that “The central bankers and bureaucrats of Europe and Japan are bereft of new ideas that will stimulate their economies. In our view they seem totally deluded in the belief that they are doing a good job. Rather they are seemingly repeating the same mistakes. Their policies have previously and once again taken their economies towards stagnation”.

Today they have no more ammunition – short of printing money and giving it to the public – to stimulate economic activity and business confidence.

We agree. Madness. Yet it appears we are headed the same way. To be clear, ultra-low interest rates is not an economic fix. The negative cash rates simply stimulate demand for government bonds as banks in particular seek yield from other sources.

And worth remembering, as we highlighted yesterday, the IMF says we are out of ammo. Time for some fresh thinking, though it might already be too late!

Worth reading….

Someone (maybe it was Albert Einstein) once opined that: “Insanity Is Doing the Same Thing Over and Over Again and Expecting Different Results”

It is our view that the maintenance of negative rates of interest

across both Europe and Japan with no positive economic result, is an act

of economic insanity. Further the continuation of quantitative easing

for nearly 8 years (in Europe) and over 15 years (in Japan) with no

discernible economic benefit are also acts of economic madness.

What will it take for the central bankers of Europe and Japan to

realise that their management of monetary policy is not working and that

there is no proof that it can work? Surely, they can see that negative

cash rates do not stimulate or even hold economic growth?

The recent readings of declining economic activity across Europe and

most notably in Germany, reflect poorly on the excessive use of monetary

stimulation. Further, the declining business confidence in Japan

recorded in February is a replay of many prior poor readings. Negative interest rates have done nothing to stimulate business confidence.

Our conclusion is this….

The central bankers and bureaucrats of Europe and Japan are bereft of

new ideas that will stimulate their economies. In our view they seem

totally deluded in the belief that they are doing a good job. Rather

they are seemingly repeating the same mistakes. Their policies have

previously and once again taken their economies towards stagnation.

Today they have no more ammunition – short of printing money and

giving it to the public – to stimulate economic activity and business

confidence.

Japanese economic growth over the last ten years is represented in

our first chart. Throughout this period Japan was effectively full

throttle with monetary policy.

Eurozone growth is hardly much better, and it has had its foot to the floor with both QE and zero interest rates.

These feeble growth outcomes follow years of aggressive monetary

policy. The next chart tracks the growth of the European Central Bank

balance sheet (QE) that has grown by over 2.8 trillion euros over the

last 4 years.

The purchase and the holdings of government bonds have ballooned.

Across most of the individual economies in the Eurozone the ECB holds

over 20% of all bonds on issue and in reviewing the purchases, there

seems to be little logic to the process. For instance, the acquisition

of German bonds seems inconsistent with the need to finance the German

government given its fiscal position is very strong. So why is the ECB

holding of German bonds the same as for Italy or Portugal, which are

economies in a fiscal mess?

It seems that the Germans, who effectively run the ECB, believe that

the likes of Italy or Portugal should receive no preferential treatment,

even if they are in dire need and Germany is not!

The maintenance of zero and negative cash rates since 2012 is shown

on our next chart. While the US has tried desperately to normalise

rates, the Europeans and Japanese have gone the other way – further into

negative.

The policy of negative cash rates is designed to penalise banks for

not lending. The excess reserves (or liquidity) of banks must be

deposited with the central bank and therefore are effectively taxed by

negative interest rates. To stop their loss the banks can push credit

out, but with no inflation, no business confidence and no perceived growth, there is little demand for credit.

The negative cash rates do stimulate demand for government bonds as

banks in particular seek yield from other sources. The maintenance of

negative cash yields combined with QE has pushed government bond yields

into negative territory and so the banks are stymied here as well. No

wonder the profits of the European banks is dreadful and the two largest

German banks (Deutsche Bank and Commerzbank) are now trying to merge to

drive costs down.

Our next chart (as at December 2018) tracks the amount of government

bonds that trade in markets with negative yields. It shows that at that

time 64% of all Japanese bonds on issue had a negative yield – even

though Japanese ten year bonds were yielding a positive return. Since

December, Japanese ten year bonds have fallen below a zero yield and the

percentage of negative yielding bonds has lurched higher towards 70%.

The cost to the economies and the investors of Europe and Japan is

immense. It is the savers and providers of capital that suffer most. The

destruction of the capital of pension funds must surely be a hidden

time bomb.

How can pension funds that generate little or no return meet the liabilities of an ageing population?

How significant is the pension shortfall across Europe and Japan? We can only wonder.

But if there is a grand covert plan to recapitalise Europe and Japan

through QE – it could be this. The central banks buy all of the

government debt on issue and then write it off or roll it into 100 year

bonds. The debt will never be repaid and effectively disappears! There is no other logical explanation for what is happening in Europe and Japan – other than insanity!

Unfortunately, it is the policies of central bankers in Europe and

Japan that is affecting the growth outlook for the whole world. It is

their policies that have stymied the US monetary policy adjustment that

is now on hold. It is their policies that are increasingly influencing

the investment returns of Australian retirees.

The outlook for Australian asset classes

There is no doubt that the declining and manipulated bond yields of

Europe and Japan directly influence the bond yields in the US and

therefore Australia. However over recent months the interplay between US

and Australian bonds has passed through a significant and historic

point.

As can be seen from the chart below, the Australian ten year bond has dipped below the US bond yield and has continued to do so.

The Australian bond yield lurched lower this week to a record low

that is now 0.25% below the RBA targeted rate of inflation. Thus ten

year bonds are close to having a negative “real” yield.

The RBA inflation target, which does influence the expected return

from investment assets, remains unmet. The recent reading of inflation

at about 1.5% is well below the target range of 2% to 3%.

Thus, the RBA is hamstrung by both the low inflation rate and the

influences from offshore policy settings. We predict that Australian

cash rates will remain at current levels for at least another 12 months.

Australia currently has “negative” real cash rates which are feeding

into bank bill rates and thus the term deposit rates offered to SMSFs by

banks. The outlook for term deposit rates is depressing!

A source of yield has been the Australian equity market. The

grossed-up yield (with the benefit of franking credits) has averaged

around 6% and given SMSF investors a yield that compensates for the

appalling alternatives of bank deposits and government bonds. Therefore,

the policy of the ALP to stop franked cash rebates would make yield

investing even more difficult in an historically low yield market.

Low investment returns on savings and cash deposits in SMSFs is

having an effect on the savings ratio. These negative influences have

added to stagnant wages growth (below inflation) and the rising cost of

basic public services to push Australia’s savings rate down. Normally a

declining savings ratio indicates growing consumption and consumer

confidence – but not this time.

This analysis supports our view that the outlook for investment returns is unexciting. Low growth, low inflation and low interest rates (short and long term) all suggest that investors need to adjust downwards their outlook for investment returns – from all asset classes.

Finally, in a most disturbing development, our last chart shows that

Australian business confidence is waning. While many commentators track

the investment intentions of business to determine the outlook for

growth, we are more interested in actual investment.

The chart below from the RBA shows that Australian listed companies

dramatically reduced capital raisings in 2018. Indeed the non-financial

sector actually reduced capital employed (it returned capital to

shareholders) for the first time in over twenty years.

Thus, if Australian companies are finding it difficult to justify

investment of their capital, with no need to raise more, then why would

investors in the Australian market believe that they can?

The emphasis for investment in equities in Australia must be tilted

towards smaller companies and those focused on offshore markets (mainly

emerging Asia and US).

It remains a difficult climate for investing. SMSFs must remain

disciplined and diversified. They should not be driven by greed to chase

excessive returns that are high risk.

Not in a world driven by insane monetary management.

The chief executive of AllianceBernstein has said that there will ultimately be a recession but it would not be happening this year, via InvestorDaily.

Seth

Bernstein, AB’s president and chief executive officer said that the

firm did not see the economy tumbling over the next twelve months.

“There is clearly a slowdown underway globally but we don’t see the US economy tumbling into a recession this year,” he said.

Mr

Bernstein during a visit to Australian clients said the yield curves

were a good predictor of recessions but were rarely good indicators of

when.

“There will ultimately be a recession but they [yield

curves] are a terrible predictor of the timing of that recession,” he

said.

However, investors would see signs as the markets moved closer to recession territory said Mr Bernstein.

“The yield curve has been flat for a very long time and it will invert closer to a recession,” he said.

Currently

the market was worried about macro events particularly the ongoing

transition of the global trade framework said Mr Bernstein.

“There

is resistance to that framework wherever anyone is disenfranchised or

where anyone finds themselves on the wrong end of change,” he said.

The

blame for the disenfranchised did not just lay with US President Donald

Trump, said Mr Bernstein, but he was the one that inflamed it.

“This

has been going on well before Donald Trump took office but Trump, in

his own distinctive way, is able to articulate it and respond to it very

forcibly for his core constituents – and he has been methodical about

checking off promises that he has made,” he said.

The current

trade barriers had led to a potentially less stable environment that was

not to the benefit of any nation, said Mr Bernstein.

“We are

concerned about a much less stable global trading environment. Lower

levels of global trade will mean lower levels of growth for Australia,

for the US, for the global economy more generally,” he said.

Ultimately,

the trade spat with China would be solved; however, Mr Bernstein said

that while it would be a deal that cuts the trade deficit, it would not

be as far reaching as the trade officials would like.

“Cooler

heads will prevail. I think the president wants a deal with the Chinese,

because he loves deals and he can talk about it in the news cycle, but

it probably won’t be as far reaching as many of us want it to be,” he

said.