The Financial Stability Board (FSB), the Basel Committee on Banking Supervision (BCBS), the Committee on Payments and Market Infrastructures (CPMI) and the International Organization of Securities Commissions (IOSCO) has published their final report on Incentives to centrally clear over-the-counter (OTC) derivatives.

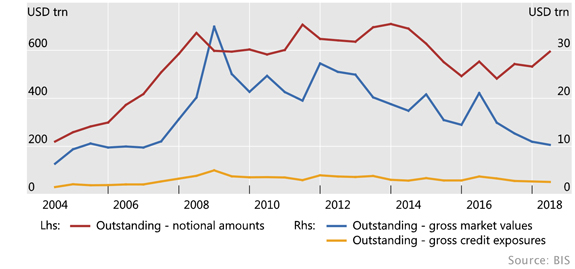

The total value of OTC derivatives was recently reported at US$595 Trillion, a massive number. The approach is been to allow the growth of these instruments, but to encourage central clearing rather than bi-lateral dealer arrangements to give greater visibility to the exposures involved. They propose capital incentives for centrally cleared transactions.

We discussed this in a recent video. This is a highly speculative market, and whilst shining more light on them may help, the more fundamental question which should be asked is why allow these to exist at all. The financial markets would be safer if they were limited to only underlying transactions, not speculative positions. At the moment, there is a risk that the derivatives markets could swamp, and bring down the normal banking system in a crisis, and that risk remains un-quantifiable. Another reason for structural separation.

The central clearing of standardised OTC derivatives is a pillar of the G20 Leaders’ commitment to reform OTC derivatives markets in response to the global financial crisis. A number of post-crisis reforms are, directly or indirectly, relevant to incentives to centrally clear. The report by the Derivatives Assessment Team (DAT) evaluates how these reforms interact and how they could affect incentives.

The findings of this evaluation report will inform relevant standard-setting bodies and, if warranted, could provide a basis for fine-tuning post-crisis reforms, bearing in mind the original objectives of the reforms. This does not imply a scaling back of those reforms or an undermining of members’ commitment to implement them.

The report, one of the first two evaluations under the FSB framework for the post-implementation evaluation of the effects of G20 financial regulatory reforms, confirms the findings of the consultative document that:

The changes observed in OTC derivatives markets are consistent with the G20 Leaders’ objective of promoting central clearing as part of mitigating systemic risk and making derivatives markets safer.

The relevant post-crisis reforms, in particular the capital, margin and clearing reforms, taken together, appear to create an overall incentive, at least for dealers and larger and more active clients, to centrally clear OTC derivatives.

Non-regulatory factors, such as market liquidity, counterparty credit risk management and netting efficiencies, are also important and can interact with regulatory factors to affect incentives to centrally clear.

Some categories of clients have less strong incentives to use central clearing, and may have a lower degree of access to central clearing.

The provision of client clearing services is concentrated in a relatively small number of bank-affiliated clearing firms and this concentration may have implications for financial stability.

Some aspects of regulatory reform may not incentivise provision of client clearing services.

The analysis suggests that, overall, the reforms are achieving their goals of promoting central clearing, especially for the most systemic market participants. This is consistent with the goal of reducing complexity and improving transparency and standardisation in the OTC derivatives markets. Beyond the systemic core of the derivatives network of central counterparties (CCPs), dealers/clearing service providers and larger, more active clients, the incentives are less strong.

The DAT’s work suggests that the treatment of initial margin in the leverage ratio can be a disincentive for banks to offer or expand client clearing services. Bearing in mind the original objectives of the reform, additional analysis would be useful to further assess these effects.

In this regard, the Basel Committee on Banking Supervision issued on 18 October a public consultation setting out options for adjusting, or not, the leverage ratio treatment of client cleared derivatives.

The report also discusses the effects of clearing mandates and margin requirements for non-centrally cleared derivatives (particularly initial margin) in supporting incentives to centrally clear; and the treatment of client cleared trades in the framework for global systemically important banks.

The final responsibility for deciding whether and how to amend a particular standard or policy remains with the body that is responsible for issuing that standard or policy.

The BCBS, CPMI, FSB and IOSCO today also published an overview of responses to the consultation on this evaluation, which summarises the issues raised in the public consultation launched in August and sets out the main changes that have been made in the report to address them. The individual responses to the public consultation are available on the FSB website.

The five areas of post-crisis reforms to OTC derivatives markets agreed by the G20 are: trade reporting of OTC derivatives; central clearing of standardised OTC derivatives; exchange or electronic platform trading, where appropriate, of standardised OTC derivatives; higher capital requirements for non-centrally cleared derivatives; and initial and variation margin requirements for non-centrally cleared derivatives.

On Monday (19 November), the seventh and final round of the royal commission hearings kicked off with CBA chief executive Matt Comyn being grilled over the group’s remuneration structures, via InvestorDaily.

Counsel assisting Rowena Orr questioned the major bank boss about frontline staff receiving ‘short-term variable remuneration’, or STVR.

“Short-term variable remuneration is what many people would think of as an annual bonus, is that right?” Ms Orr asked.

“Yes,” Mr Comyn confirmed. “We do not refer to it in that way, but it is a bonus.”

While he admitted that the bank has made a number of changes to its remuneration structure, including work towards the Sedgewick recommendations, Mr Comyn explained why CBA is standing firm on bonuses.

“We believe it is important to have an element of remuneration which is not fixed. We believe it is a well-designed set of metrics or a way for them to earn their short-term variable remuneration; it is both a way of eliciting discretionary effort and a way beyond termination as a form of consequences. It is also a way to make consequences clear to individuals,” he said.

After being prodded by Ms Orr for clarification, the CBA chief explained that “discretionary effort” is the difference between what staff might have otherwise have done if they were paid a fixed salary.

Ms Orr asked why staff can’t be motivated simply by being paid a fixed salary.

Mr Comyn used an offshore example to try and illustrate his response, alluding to a female employee at one financial institution in the United Kingdom that decided to stop paying bonuses.

“I’m talking specifically about a home lender. What they were in effect paid was 98.5 per cent of their prior year’s fixed remuneration and short-term variable reward. So they were guaranteed that remuneration,” he said.

“When I asked her what had changed, her answer was simply ‘I probably work 30 per cent less’. She was one of their best performing lenders.”

Mr Orr offered alternative ways of motivating staff instead of a bonus: “positive feedback for their performance; encouraging them to take pride in their work; encouraging them to have a sense of satisfaction in helping one of your customers; giving them additional responsibilities as a reward for performance; promotion; a higher base salary.”

Mr Comyn said all of these were appropriate ways of driving staff. However, he maintained that CBA has decided for now to continue using short-term variable rewards, or bonuses, to motivate fits sales force

A quick reminder of our upcoming live stream event tomorrow evening. You can join the live chat, or leave a question before hand in the comments. It should be a fun event! Here is the link to the event bookmark.

I think most of you will agree that in the past getting approved for a credit card wasn’t exactly difficult. I’ve heard some jokingly say that if you had a pulse you could get a card. A little cynical perhaps, but the fact is banks loved approving credit cards. It’s no mystery why, as where else could they generate those sorts of returns?

I’m sure you recall going to a shopping centre or airport and being accosted by an overly enthusiastic bright-eyed credit card salesperson. They couldn’t wait to get you a nice, new shiny credit card, perfect for buying things you didn’t need, with money you didn’t have. Between letters and emails sent by the banks with headings like, “You have been approved!” before an application had even been lodged, to credit cards being offered by anyone from supermarkets to airlines, the banks’ addiction to credit cards was obvious.

For better or for worse this may all be about to change. New regulations with regard to credit cards came into effect on July 1st with more to follow early next year.

One of the big issues being looked at is the time it takes for many people to pay off their credit cards. I can’t think of another type of loan where, with minimum payments, the loan may take longer than the borrower’s lifespan to retire. I’ve seen many credit card statements where the micro writing at the bottom of the page says something like, “At the minimum payment this debt will take 72 years to pay off”. I know life expectancy is improving, but come on! Can you think of another type of loan where the payments would outlive the borrower?

The government is onto this and is concerned about people that cannot pay down their credit cards within a reasonable period and are being exposed to high interest charges as a result. While the banks are publicly agreeing with this, the cynical side of me feels they would be quite happy to leave things as they are.

Following on from this, ASIC recently produced a report which put forward that credit card applications should be assessed on the basis that the credit limit can be retired within three years. It’s looking like this will become policy starting January 2019.

This will be a game changer and will instigate a massive change to how credit card applications are assessed. It’s a welcome change as it will help save people from themselves and hopefully ease household debt levels that seem to be ever increasing, with much of it on credit cards. One thing is for sure, it will mean getting approved for a credit card will be much tougher and this may even result in the review and possible adjustment of current credit card limits.

The days of the banks pushing limit increases are also over. It wasn’t long ago that people would receive endless letters and emails offering to increase their limits. It always struck me as odd that when someone was applying for a home loan they had to provide endless amounts of supporting information, but if they wanted a credit card it was often just a few mouse clicks away.

It appears the banks’ desire to benefit from high interest generating products clouded their judgment when applying sensible lending policies. In other words, the higher the return the lower the scrutiny.

New regulations now prohibit banks from pushing unsolicited credit limit increases which is a very good thing, as offering more and more credit to often venerable people was in my opinion predatory behaviour and not at all responsible.

The royal commission continues to reveal questionable behaviour by the banks and I feel further reform is on the way, but I do have a concern.

While we all want the banks to behave, we’re already seeing lending tightening up and this is causing real issues for people and businesses— and potentially the economy. Many people are quick to cry foul of the banks however let’s not forget that we are a credit-driven society and if credit dries up, everything else tends to dry up too and we all suffer.

I would like to think some middle ground will be found, where banks will act more responsibly when approving credit, but will remain open for business with providing credit in general.

Author: John Dickinson director of DebtX Mediation Services.

“An unexpected tight squeeze on credit for home buyers is accelerating the slowdown in building activity,” said Mr Tim Reardon, HIA Principal Economist.

HIA released its quarterly economic and industry outlook report today. The State and National Outlook Reports include updated forecasts for new home building and renovations activity for Australia and each of the eight states and territories.

“The credit squeeze that has been impeding investors for the past 18 months has expanded and is now restricting building activity across the market,” added Mr Reardon.

“APRA’s restrictions were designed to curb high risk lending practices but we are now seeing ordinary home buyers experience delays and constraints in accessing finance.

“This disruption in the lending environment is impacting on the amount of residential building work entering the pipeline. The effect on actual building activity will become more evident in the first half of 2019.

“The credit squeeze is weighing on a market that had already started to cool from a significant and sustained boom.

“If these disruptions to the home lending environment prove to be long lasting then we could see building activity retreat from the recent highs more rapidly than we currently expect.

“The decline in housing finance data shows that something in the lending environment has changed. Lending to owner-occupiers building or purchasing new homes fell by 3.6 per cent in September and is down by 16.5 per cent over the year.

“The year 2017/18 saw over 120,000 detached house starts. This is one of the strongest results on record. We expect new home starts to decline by 11.4 per cent this year and then by a further 7.4 per cent next year in 2019.

“With the prospect for the release of the Hayne Royal Commission’s findings to trigger further upheaval in the banking system, we need the banks maintain stable lending practices for fear of a destabilising influence on the housing market,” concluded Mr Reardon.

It will be worth watching the final round of hearings at the banking royal commission, which begins today. The chief executives of each of the big four will be recalled for reexaminations, via The Conversation.

It might be the final time they appear in the same room. It might even be the last time there’s even such a thing as the big four.

Not only are the so-called four pillars under attack from the Commissioner Kenneth Hayne, but there are also enormous economic and technological pressures that are already beginning to undermine their special status.

Together, these pressures have the potential to radically change the banking landscape over the coming decades and bring an end to the Four Pillars policy under which Westpac, the Commonwealth, the ANZ and the National Australia Bank have been effectively protected from takeover and prevented from merging.

Although never a formal law, the understanding that none of the big four can merge has been an accepted rule in Australian business since the late 1980s, when the then treasurer Paul Keating made it clear he would block takeovers.

Eggs in one basket

Since then the big four banks have changed in two important, but related, ways.

Over the past few years they have retreated from their overseas banking ventures, largely divesting themselves of their sometimes ill-judged foreign acquisitions.

And they have recently sold off most of their local wealth management (insurance and investment) subsidiaries.

These divestments mean we are left with four enormous retail-oriented banks that dominate both the banking system (with almost 80% of banking assets) and the stock market (four of the top six companies on the S&P/ASX 200).

Their profitability is heavily dependent on lending for housing, which in turn is heavily dependent on the housing market.

That market is already beginning to contract, meaning the big four are going to find it increasingly hard to maintain their stellar profits.

No longer unique

What’s more, the near monopoly they have had on processing payments is under threat.

In Britain around 1,000 bank branches are closing per year in the wake of a technologicial revolution that makes it possible to process payments away from branches and away from banks. The rate of these closures is climbing.

Mobile banking means that many basic transactions that used to require a visit to a branch can be done online. Australia’s New Payments Platform means that payments to people such as tradies can be made anywhere, any time, in real time and at minimal cost. Use of the platform isn’t limited to the big four.

The Reserve Bank reports that after only eight months of operation the number of payments on the platform already exceeds the number of cheques.

Too many branches

Compared with other countries, we have a lot of bank branches.

Australian banks operate more than 5,000 branches, most of them owned by the big four, as well as 30,000 automatic teller machines, and more than 900,000 EFTPOS terminals at supermarkets and Post Offices.

In the United States, just one bank, the Bank of America, has 67 million customers.

In 1997, the Wallis Financial Systems Inquiry recommended it be scrapped.

On the other hand, the 2014 Murray Inquiry into financial services recommended that the policy be retained.

But the Murray inquiry, probably due to its narrow terms of reference, found little of the egregious misconduct that has been uncovered by the royal commission. This calls into question the inquiry’s conclusion that there is adequate competition in the banking system.

Indeed, this conclusion was rejected in a recent Productivity Commission report, which stated bluntly that “the Four Pillars policy is a redundant convention”.

An end in sight

The end of the four pillars policy needn’t mean the end of competition. Smaller, cheaper competitors will be doing more of what the big four did.

A shakeout of bank branches is long overdue, however painful that may be in many small towns, where despite the serious problems raised at the royal commission, a bank branch is still an important part of the community.

Undoubtedly, such a major disruption, unless managed carefully, will be harrowing for many customers and staff.

But for the long-term stability of the economy, it is incumbent on governments to address the inevitability of a smaller, more technologically driven banking system – one that hopefully, after the royal commission, will operate ethically for the benefit of customers.

Author: Pat McConnell, Visiting Fellow, Macquarie University Applied Finance Centre, Macquarie University

APRA is undertaking work to keep Australian’s financial institutions secure if and when the economic summer ends, said newly appointed deputy chair, via InvestorDaily.

APRA’s deputy chair John Lonsdale made the comments at FINSIA ‘The Regulators’ event saying that Australia had endured 27 years of continuous expansion but no summer lasts forever.

“Australia’s unprecedented period of uninterrupted economic growth may have years yet to run. We hope it does.

“But when our economic summer inevitably ends – and winter, autumn or just an unseasonal cold snap arrives – the work that APRA is undertaking means Australians can be confident that the financial institutions they rely on are resilient,” he said.

Mr Lonsdale said that over the coming year APRA would focus on policies and actions to withstand any conditions, starting with a review into the regulators enforcement strategy.

“The review will make recommendations on which enforcement issues APRA should consider acting on, what factors we should take into account, and whether there are any practical or legislative impediments to us pursuing a stronger approach,” he said.

Without pre-empting the review, Mr Lonsdale said the authority was willing to consider a strong appetite for formal enforcement action but would remain true to it’s purpose as a regulator.

“We will, however, remain a supervision-led, rather than enforcement-led, regulator with a focus on pre-emptively tackling problems before they compromise an entity’s ability to meet its obligations to beneficiaries, or rectifying adverse outcomes in the best interests of customers.”

Mr Lonsdale said the group would continue into 2019 looking at cases of misconduct that had been raised during the royal commission which may see more enforcement action taken.

“We are also re-examining cases of potential misconduct by regulated entities raised during the royal commission where the evidence presented was either new to APRA or contradicted what we had previously been told,” he said.

APRA would also continue to administer and monitor the BEAR to ensure it is being followed by all the players in the industry said Mr Lonsdale.

“We are actively making sure the regime is firmly embedded in the major banks – and preparing other ADIs to implement it – rather than assessing whether it is yet achieving its objectives,” he said.

Mr Lonsdale said the following year would also see APRA make further advancements towards implementing the final elements of the complex Basel III capital framework for ADIs.

“A key component is rethinking how Australia’s relatively more conservative capital approach can be explained to provide greater transparency about the strength of our banks and more flexibility in times of stress,” he said.

The authority was also working on developing a formal prudential framework for recovery and resolution, to help stressed institutions restore themselves or in extreme cases manage orderly failure of entities beyond help.

“Our ability to create such a framework has been enhanced by the recently passed legislation expanding APRA’s crisis management powers, which provided a clear basis to make prudential standards on resolution.

“These are powers APRA hopes never to need; however, possessing a strong framework to manage failures and crises is a critical component of a resilient financial system,” he said.

APRA was also working with super groups to finalise member outcome packages as well as moving towards an aligned framework for private health insurance with that used in life and general insurance.

Mr Lonsdale finished by saying APRA keenly awaited the final report of the royal commission and would react to its recommendations.

“Both the report, and the government’s subsequent response to its recommendations, will become high priorities for us once they are made known, and we are confident that the financial system will ultimately emerge stronger from the scrutiny,” he said.

Domain has released their preliminary results for today. More evidence of a slowing. Last week the result was 39.2%, (off the scale on the Domain chart!).

Preliminary results show similar weakness, and will likely settle lower ahead. This signals lower home prices ahead.

Brisbane listed 102, reported 48 and sold 29 with 3 withdrawn giving a Domain clearance of 57%.

Adelaide listed 80, reported 49 and sold 35 with 5 withdrawn, giving a Domain clearance of 65%.

Canberra listed 96, reported 80 and sold 37 with 5 withdrawn, giving a Domain clearance of 44%.

Welcome to the Property Imperative weekly to 17th November 2018, our digest of the latest finance and property news with a distinctively Australian flavour.

Watch the video, listen to the podcast or read the transcript.

It has been a roller coaster ride on all fronts this week, with more market gyrations, larger predicted falls in home prices locally, and the first “unnatural act” from the Government to try and sustain the finance sector, ahead of next year’s election, expect more ahead.

And by the way you value the content we produce please do consider joining our Patreon programme, where you can support our ability to continue to make great content.

We start with the markets this week the Dow closed lower for the week, despite a rally on Friday that came despite the White House reportedly walked backed President Donald Trump’s upbeat comments on trade.

The Dow Jones Industrial Average rose 0.49% to 25,413 at the end of the week, the S&P 500 rose 0.22% to 2,736, but the Nasdaq Composite fell 0.15%.

After the falls earlier in the week, Wall Street went into rally mode Friday after Trump said he was hopeful the U.S. and China will reach a consensus on trade deal. Later the White House, however, peddled a more sombre narrative on trade in the wake of Trump’s comments, telling CNBC that a deal was not coming soon. Still, the broader averages held their gains, but that did little to avert a weekly loss following a rout in tech. The fear index, the VIX eased a little on Friday, down 9.21% to 18.14, but is still elevated, signalling uncertainty ahead.

In tech, Facebook fell 3% amid the fallout from a New York Times article detailing how the company conspired to cover up warnings that Russia had used the social media platform to disrupt the U.S. election in 2016. Apple moved higher after recent falls, up 1.11% to 193.53, while Alphabet fell 0.26% to 1,068. Intel was up 1.5% to 48.53.

Financials were mixed, with the S&P 500 Financials index up 0.06% on Friday to 443.45 but Goldman Sachs Group was down 0.8% to 202.12.

Sentiment on stocks were also lifted by easing concerns about steeper U.S. rate increases after Federal Reserve Vice Chairman Richard Clarida indicated that the U.S. central bank may stop at the neutral rate, rather than continue hiking beyond the neutral rate, which might be interpreted as an effective “rate cut,” JPMorgan said in a note to clients. The 3m bond rate slid 0.67% to 2.35, and the 10-year was 1.71% down on Friday to 3.065. Clarida does not expect a big increase in inflation this year. With that in mind, both central bankers are still confident enough in the domestic economy to proceed with a December rate hike, but there’s a good chance that it will be accompanied by a less hawkish outlook.

Energy added steel to the rally on Friday as oil prices settled flat, but slumped 6% for the week on concerns about a global glut in supplies. The WTI futures was up 0.66% to 56.83. Oil bears are back to taunting Saudi Arabia by pressuring the market again, just two days after giving a reprieve to the record sell off in crude.

In fact, West Texas Intermediate and Brent crude futures settled steady to slightly higher on Friday after rallying more than 2% earlier in the day on fears that the oil-rich kingdom and the OPEC cartel it leads could cut supplies substantially at a December 6-7 meeting. Friday’s s rebound didn’t help crude’s weekly loss of 6%, making it the sixth-straight week in the red.

Prices initially rose on an analysis from tanker-tracking firm ClipperData that showed Saudi Arabia was already loading fewer barrels on ships bound for the United States this month, continuing a trend that began in September. By sending fewer barrels to the United States, the Saudis hope to starve U.S. crude stockpiles, which have swelled by nearly 50 million barrels the past eight weeks. It’s a strategy the kingdom used last year while working alongside OPEC members, Russia and other producers to rescue oil prices from lows under $50 a barrel. But after the morning highs in New York trade, prices turned volatile before returning to positive territory just before the close. Adding pressure to the market was weekly U.S. oil rig data showing drilling activity at its highest in over three years, after an addition of two rigs this week.

In an extreme turn of events, the fire from Bitcoin Cash’s hardfork war has spread wildly across the entire crypto market, burning through virtually every cryptocurrency and leaving many investors burnt too. Bitcoin had more than $28 billion stripped from the market, as it fell beyond the support of its long-standing safety net at $5,800.

Gold was higher, up 1.9% to 1,222 on Friday, with some suggesting that the US$ bull run might be ending, as economic outperformance, rising interest rates, equity market pressure and trade policy all look suspect, and a switch to metals might make sense. But more likely it is the risks around Brexit, Theresa May could be fighting for her political survival, but the Brexit crisis she’s in has thrown gold bulls a lifeline. Initially resigned to losing the market’s $1,200 support level as the week began, fans of the yellow metal not only got to stay in their comfort zone but also saw their best weekly gain in five as hedgers rushed to the relative safely of bullion after the pounding taken by sterling from Britain’s EU-exit woes. Tory MPs may have enough votes – 48 are needed – for a letter of no confidence that would force a vote in Parliament. If the rebels within her ranks really do have the votes to force a no-confidence motion UK politics will be thrown into an even greater existential crisis.

Not that a change in leadership there would make much difference. U.K. Prime May on Friday reshuffled her minister team and took personal charge of the divorce talks with the European Union. The moves came at the end of an extraordinary week in which seven members of her government resigned and a push to force her from power gained momentum.

The pound gained 0.4% against the U.S. dollar on Friday, rebounding a bit from Thursday’s plunge. But sterling still suffered a loss for the week and volatility soared to a two-year high. The British Pound Dollar was up 0.48% on Friday to 1.2835, while the Euro USD rose 0.76% to 1.1414. The US Dollar index fell 0.51% to 96.43. Deutsche Bank, was down 0.06% to 8.59, not helped by recent Eurozone bank stress test results.

All 3 of the commodity currencies traded higher on Friday with the Australian hitting a 2-month high and the New Zealand dollar hitting a 4-month high. AUD and NZD ripped higher on the hope that President Trump will forgo another round of tariffs on China. Ever since the mid-term elections, his tone toward China has been softening. The Aussie ended up 0.76% to 73.32, helped by strong jobs numbers in October and bullish noises from both the treasurer and the RBA.

In the local market, the ASX 100 fell 0.17% to 4,711, reflecting similar weakness in US stocks. The ASX Financials was also down, 0.09% to 5,635.60 in bearish territory. Regional Bendigo bank was up 0.99% to 10.20, while Suncorp fell 0.15% to 13.54 and the Bank of Queensland was higher up 0.82% to 9.78. Macquarie who generates more than half of its business offshore, rose 0.16% to 119.00 whilst the majors were softer, with NAB down 0.46% to 23.77, Westpac down 0.28% to 25.27, then went ex. Dividend this week, ANZ was down 0.12% on Friday to 25.36 while CBA was up a tad to 68.90. Lenders Mortgage Insurer Genworth tracked lower down 0.91% to 2.18, not least because they are exposed to the housing sector and the investment markets, both of which look weaker. AMP continues in weak territory, although up 1.98% to 2.58. The Australian VIX index eased back, down 3.33% to 16.80, still will in the nervous zone. The Aussie Bitcoin dropped 2.76% to 7,492 and the Aussie Gold slid 0.06% to 1,666.43.

The property news continues south, with the latest CoreLogic average clearance rate down again last week, with only 42.7 per cent of homes successful at auction. And that excludes the large number of unreported results, so the true numbers in even worse. There were 1,541 auctions held across the combined capital cities, having decreased from the 2,928 auctions held over the week prior when a higher 47 per cent cleared. Both volumes and clearance rates continue to track lower each week when compared to the same period last year (2,046 auctions, 61.5 per cent).

In Melbourne, final results saw the clearance rate fall last week, with 45.7 per cent of the 266 auctions successful, down from the 48.6 per cent across a significantly higher 1,709 auctions over the week prior. Across Sydney, the final auction clearance rate came in at 42.6 per cent across a slightly higher volume of auctions week-on-week, with 813 held, up from 798 the previous week when 45.3 per cent cleared. Sydney’s final clearance rate last week was not only the lowest seen this year, but the lowest the city has seen since December 2008.

The only capital city to see more than 50 per cent of auctions successful last week was Adelaide (50.8 per cent), however this was lower than the prior week’s 57.6 per cent. Brisbane saw the lowest clearance rate, with only 30 per cent of homes selling.

Geelong recorded the highest clearance rate of all the non-capital city regions, with 57.1 per cent of auctions reporting as successful, while the Sunshine Coast region had the highest volume of auctions (55).

CoreLogic are expecting more auctions today, so we will see if this eventuate.

I discussed the latest household data at a UBS forum on Monday, other members of the Panel were included Tim Lawless from CoreLogic and Christopher Joye Coolabah Capital as well as Jon Mott Head of Banks at UBS and George Tharenou their Chief economist. You can watch my segment of the discussion “Some Thoughts About The Housing Market” via a scratch recording I made. Frankly demand for property continues to weaken, as supply rises, and sales volumes fall. First time buyers and investors are becoming more cautious. Jon Mott has been negative on the sector for some time and his new note proposes a worst case scenario in which Aussie house prices crash 30%, the RBA cuts rate to zero and launches quantitative easing, and banks are crushed by cascading bad debts, cut dividends and class actions. Smartly he has developed a range of different scenarios (scenarios will sound familiar to anyone following DFA, as we have been doing this for years, it’s the best way to communicate the intrinsic uncertainty in the system.

He thinks that his scenario 3 – housing correction is most likely, with a 10% drop in prices, and that the banks will be challenged in this environment. But if prices fall further, the banks get hit with class actions, and bad debts they will have to cut dividends.

SQM’s Louis Christopher also issued their latest Boom-to-Bust report, and guess what, he also used scenarios. SQM’s base case forecast is for dwelling prices to fall between -6% to -3%, which is a continuation of the current falls of 4.5% over the past 12 months. Sydney and Melbourne will drive the falls. Other cities will record mixed results with Hobart expected to have a third year of strong price rises of 5% to 9%. The base case forecasts assume no changes in interest rates, a Labor win at the next Federal Election with Negative Gearing repeal and CGT changes coming into effect 1 July 2020. If SQM Research is correct on the Sydney and Melbourne forecasts, it will mean by the end of 2019, the peak to trough declines will be at least in the order of 12% to 17% for these two cities. SQM Research believes that, presuming the RBA does not intervene in the market, 2020 could also record price declines due in part to the repeal of Negative Gearing which is a firmly stated Labor party objective. As such there is a risk that the total peak to trough declines could be in the order of 20% to 30% for our two largest capital cities. The range is dependent on: When, if and how the RBA responds to the downturn; How the economy responds to the downturn; Will the banks be required to lift rates out of cycle; Will negative gearing and capital gains tax concessions be repealed as per the Labor Party’s policy. Christopher said, “If the RBA does not respond and/or the bank lift interest rates again in 2019, it is possible the peak to trough falls in Sydney and Melbourne could be even more than this negative range. But we do take the view that the downturn in Sydney and Melbourne will be a significant negative for the overall economy, and so the central bank will eventually respond at some point and cut interest rates.”

Gareth Aird the senior economist at CBA discussed the drivers of dwelling prices, and identified four leading indicators that capture the momentum in the property market well. They are: (i) the flow of credit (i.e. housing finance); (ii) auction clearance rates; (iii) foreign residential demand; and (iv) the house price expectations index from the WBC/MI Consumer Sentiment survey. Presently all of these indicators are pointing to dwelling prices continuing to deflate over the near term (up to six months).

Indeed, credit and prices are strongly correlated, as we have discussed before. From a dwelling price perspective, the flow of credit matters more than changes in the stock. The annual change in housing finance has a close leading relationship with the annual change in dwelling prices by around six months. New lending is driven by the supply and demand for credit. The latest housing finance data indicates that the flow of housing credit continues to fall. And the pace of the decline has accelerated (chart 3). Credit to investors has been trending down for the past 1½ years. But it’s the shift downwards in lending to owner-occupiers that is behind the recent acceleration in the decline of credit.

Generally, auction clearance rates are a leading indicator of prices. Auction clearance rates tend to lead prices on average by two months. Auctions are more popular in Sydney and Melbourne as a means of selling a property. As such, the link between auction clearance rates and property prices is very much a Sydney and Melbourne story. As a rough rule of thumb, the annual change in dwelling prices tends to be negative when the auction clearance rate is below 55%.

Over the past two years, foreign investment in Australian property has waned. This is primarily due to a lift in state government stamp duties levied to foreign investors as well as tighter capital controls out of China. There is a decent relationship between the annual change in property prices against the share of sales going to foreign investors. Generally foreign purchases have led prices on average by around four months, although that lead time has shrunk more recently.

And finally on consumer sentiment, Aird says it has proved a very useful near term indicator of the annual change in dwelling prices. There is of course a self-fulfilling aspect at work. If households expect prices to weaken then demand for credit will fall and prices will correct lower. The reverse is also true when households expect price growth to accelerate. The WBC/MI house price expectations index is pointing to dwelling prices continuing to deflate over the near term.

He also again illustrated the fall in investor borrowing, the shift away from interest only loans, and a significant decrease in the maximum loan sizes now on offer – on average down 20%, though we think for some households the fall is significantly larger. He also showed some households were now paying higher rates, thanks to larger spreads over the P&I loan benchmark.

The trend unemployment moved a little lower according to the data from the ABS, from 5.2 per cent to 5.1 per cent in the month of October 2018. This is the lowest unemployment rate since early 2012 and the 25th consecutive monthly increase in employed full-time persons with an average increase of 20,300 employed per month. The trend underutilisation rate decreased 0.1 percentage points to 13.4 per cent and the trend participation rate remained steady at 65.6 per cent in October 2018.

But wages growth remains sluggish with the seasonally adjusted Wage Price Index (WPI) up 0.6 per cent in September quarter 2018 and 2.3 per cent through the year. The more reliable trend was 0.5% in the September quarter. Private sector wages grew by 0.55% over the quarter, whereas public sector wages grew by 0.61%. So Public Sector wages are growing more strongly, whilst the private sector continues to struggle. The weak wages growth will dent the budget projections and household budgets. Western Australia recorded the lowest through the year wage growth of 1.8 per cent while Tasmania recorded the highest of 2.6 per cent.

So no surprise that our household financial confidence index was lower in October The index measures households overall comfort level with their finances across a number of key dimensions. Recent home price trends, lower returns on deposits and share market gyrations have combined to take the index lower, despite strong employment trends. The wealth effect is now working in reverse, with a potential impact on future consumption. The index returned a result of 88.1, down from 88.4 last month. This continues the decline since late 2016, and is now approaching the lowest ratings from 2015. The convergence across the states continue as home price falls in NSW and VIC take a toll, with the southern state showing a significant slide. WA and QLD appear to be tracking quite closely. Across the age bands, younger households are under the most pressure (thanks to large mortgages, or renting) while those aged 50-60 years remain the most confident, thanks to lower net borrowing, and more savings and investments. For those aged 40-50 recent falls in property prices swamp any benefit from stock market performance. Those holding property for owner occupation remain the most positive, despite falls in paper values of their homes, but property investors are now registering significant concerns, thanks to flat or falling net income from rentals, falling capital values and concerns about the future of negative gearing and capital gains tax relief. More property investors signalled an intention to seek to sell property, as the switch from interest only to principal and interest loans continues. More than 41% of mortgage applications were rejected, compared with 5% last year, as more rigorous underwriting standards bare down. In fact those renting are in many cases more confident than property investors, significant turnaround. The great property investor decade in passing. You can watch our show “Household Financial Confidence Is In The Gutter”.

The use of the Household Expenditure Measure HEM may well be back in play, following the latest from the Westpac ASIC case. Given that at some banks HEM is still being used for around half of applications, and the Royal Commission commented specifically in the use of HEM, perhaps the law needs to be changed. The core of the argument is whether the loans were unsuitable, and that it seems would depend of the ultimate progress of the loan subsequently. In other words, it cannot be proved to be unsuitable until it falls over. ASIC would need to prove the loan was unsuitable! Actually we think the law says lenders have to verify expenses, and in other cases, for example in pay day lending specific inquiries are required as part of the assessment. But it’s as clear as mud at the moment! When is unsuitable lending to be demonstrated? This will have a significant impact on any potential class actions. And of course next week the Royal Commission start they next round, with senior bank executives and regulators on the stand. This should at very least be entertaining, and will perhaps get to the heart of the cultural issues in banking and finance. In this regard you should watch our recent show with John Dahlsen, business man and ex. ANZ Director, who has some important things to say about what has driven the poor outcomes from the sector and what needs to change. It’s a long piece, but highly relevant – “Thinking About Banking From The Inside”.

But for now, banks want more data on expenses, and the latest was ANZ who outlined new tighter rules from 20th November, where mortgage applicants will need to provide much more evidence, and history on income and expenditure. Any income from bonuses will be ignored and income shaded to 80% and evidence of continuous employment is needed. As well as more granularity and evidence on expenditure, they also will want more detail on potential changes to personal circumstances.

And finally, this week we saw the first “unnatural act” from the Government to support the banking sector, in an attempt to alleviate the home price falls and lending freeze ahead of the election next year. The proposed $2 billion funding pool is small beer in the estimated $300 billion SME lending sector. There is precedent a decade ago when the government’s $15 billion co-investment with the private sector into the residential mortgage-backed securities market during the GFC. So the federal government announced a new, $2 billion Australian Business Securitisation Fund to help provide additional funding to small business lenders. But this is lipstick on a pig in my view, and does not get to the heart of the matter at all. But I expect more such measures in the run up to the next election.

And if you want to understand what is ahead, then watch my recent interview with Harry Dent, as we discuss the limitations of central banks, and how QE has really created a monster which is still running rampant. And we are also extending our reach into the New Zealand market with the help of Joe Wilkes, see our latest Ireland V New Zealand – A Passion For Rugby & Property.

But to sum up the state of play, the Bears are indeed in town, and we should prepare ourselves for more falls ahead. Our scenarios continue to play out as expected.

Finally, a quick reminder, our next live Q&A session is now scheduled for November 20th at 8 pm Sydney time. You can schedule a reminder by using the YouTube Link and join in the live discussion, or send in questions beforehand. If previous sessions are any guide, it should be a lively event!