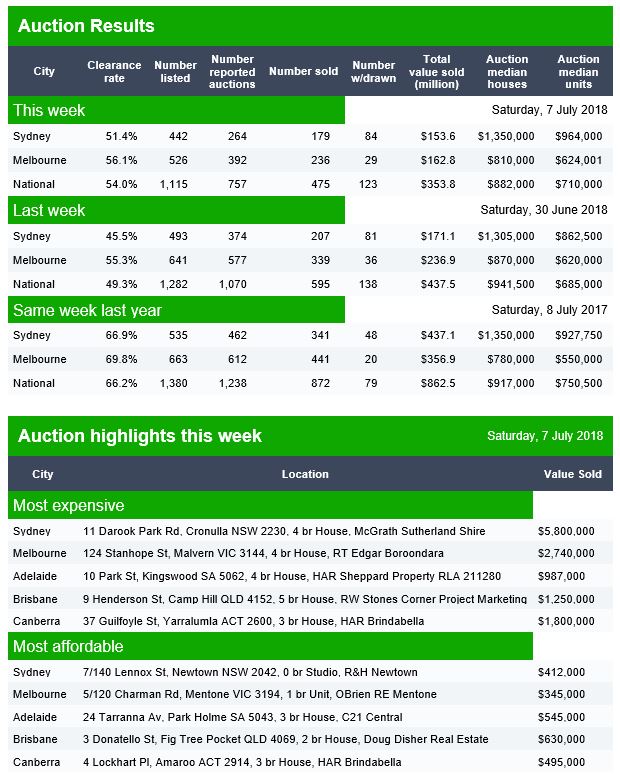

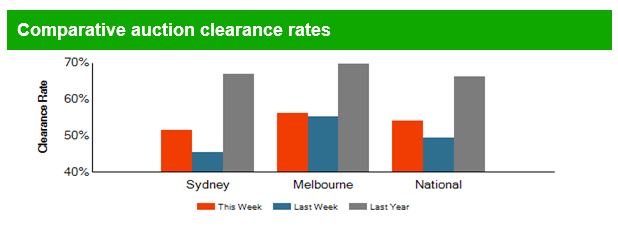

The preliminary data from Domain is out, and the trends continue lower, with a final rate last week below 50% nationally and continued weakness this time around. Many properties are being withdrawn.

In Sydney, of the 442 listed, 84 were withdrawn, and 179 sold. In Melbourne, 526 were listed, 29 withdrawn and 236 sold. Last year at this time, clearance rates were more than 10% higher, on larger volumes.

Brisbane listed 57, 6 were withdrawn and 17 Sold. Adelaide listed 43, withdrew 1 and sold 13. Canberra listed 47, sold 30 and 3 were withdrawn.

ASIC has accepted court enforceable undertakings from the Commonwealth Bank of Australia and Australia and New Zealand Banking Group under which the banks have agreed to change the way they distribute superannuation products to their customers.

ASIC investigated CBA’s distribution of its Essential Super product and ANZ’s distribution of its Smart Choice Super and Pension product (Smart Choice Super) through bank branches. ASIC found a common practice of offering those products to customers at the conclusion of a fact-finding process about customers’ overall banking arrangements.

CBA’s fact-finding process was called a ‘Financial Health Check’. CBA staff also sometimes helped customers roll over their other superannuation into the Essential Super account at the time of distribution.

ANZ’s fact-finding process was called an ‘A-Z Review’.

ASIC was concerned that the proximity between the fact-finding process and the discussion about Essential Super or Smart Choice Super was leading CBA staff and ANZ staff to provide personal advice to customers about their superannuation. Branch staff for both CBA and ANZ were only authorised to provide general advice.

Stricter consumer protection laws apply to financial services licensees when their representatives give personal advice about complex financial products such as superannuation than when they provide general advice about those products. This includes the requirement, with personal advice, to give a customer a Statement of Advice and to act in the customer’s best interests. People who give personal advice about complex products are also required to meet higher training standards.

ASIC was concerned that customers may have thought, due to the proximity of the fact-finding process to the offer of Essential Super or Smart Choice Super, that the CBA branch staff or the ANZ branch staff were considering risks specific to the customer when this was not the case.

These court enforceable undertakings prevent CBA from distributing Essential Super in conjunction with a Financial Health Check and ANZ from distributing Smart Choice Super in conjunction with an A-Z Review. They also require CBA and ANZ to each make a $1.25 million community benefit payment. If there is a breach of the undertaking ASIC can, under the ASIC Act, apply for orders from the court to enforce compliance.

CBA chose to suspend the distribution of Essential Super in CBA branches in October 2017.

‘ASIC will continue to proactively monitor how complex financial products such as superannuation are sold,’ ASIC Deputy Chair Peter Kell said.

ASIC’s actions underline the importance for financial services licensees to ensure that customers understand the nature of advice they are receiving about their superannuation.

ASIC’s investigation arose following a surveillance conducted in relation to CBA’s distribution of its retail superannuation product, Essential Super and ANZ’s distribution of its retail superannuation product, Smart Choice Super.

These actions are part of ASIC’s Wealth Management Project. The Wealth Management Project was established in October 2014 to lift the standards of major financial advice providers. The Wealth Management Project focuses on the conduct of the largest financial advice firms (NAB, Westpac, CBA, ANZ, Macquarie and AMP).

ASIC says Perth man Mr Peter Lachlan McDonald has been sentenced in the Perth Magistrates’ Court to 21 months’ imprisonment following an investigation by ASIC into his brokering of motor vehicle finance contracts while an employee of Get Approved Finance.

The sentence was fully suspended for 12 months upon Mr McDonald paying a $5000 bond to the Court. The sentence took into account Mr McDonald’s guilty plea to seven charges of giving false information to Esanda (a business then owned by ANZ) and one fraud charge.

ASIC Deputy Chair Peter Kell said Mr McDonald’s actions abused the trust of his clients, who are entitled to expect brokers to act honestly and in their best interests.

‘Loan fraud, which often involves an intermediary like a finance broker, is a particular focus of ASIC. We are actively working to improve standards in the broking industry and warn anyone tempted to deceive lenders or mislead customers that they will be held to account.’

Since becoming the national regulator of consumer credit in 2010, ASIC has achieved significant loan fraud outcomes resulting in 17 convictions for various related offences. Over this time, 83 individuals or companies have also been banned from providing credit services or precluded from holding a credit licence.

Mr McDonald was sentenced on 5 July 2018. The Commonwealth Director of Public Prosecutions prosecuted the matter.

Background

ASIC’s investigation found that between January 2013 and April 2013, Mr McDonald, in the course of brokering four motor vehicle finance contracts, provided the lender Esanda (a business then owned by ANZ) with information that falsely represented that persons, who had in fact only agreed to be loan guarantors, were the applicant borrowers who would ultimately own the vehicle to be financed. It is alleged that Mr McDonald had previously advised his clients, who had poor credit histories, that they would be approved for vehicle finance if their loan applications were supported by guarantors.

In two further loan applications, Mr McDonald is alleged to have provided information to Esanda that falsely represented that insurance quotes were issued insurance policies, knowing that Esanda required all financed vehicles to be insured before loans were approved. In one additional application it is alleged that Mr McDonald inserted what purported to be his client’s signature on an extended warranty and submitted that document to Esanda (the client having agreed to purchase the extended warranty).

In relation to one of the seven loan applications, Mr McDonald is also alleged to have acted fraudulently by artificially interposing a third party vendor while representing to his client that the vehicle being purchased on credit was being sourced directly from a car dealership. In doing so, he gained a pecuniary benefit for himself.

In July 2015, ASIC permanently banned Mr McDonald and a colleague from engaging in credit activities and providing financial services (refer: 15-189MR).

At the time of the conduct, Get Approved Finance was the trading name and operated under the Australian credit licence of West Australian-based finance broker Jeremy (WA) Pty Ltd. The company was deregistered in September 2017.

A number of other former Get Approved Finance brokers have also been banned by ASIC from both the credit and financial services industry (refer: 15-374MR, 16-116MR, 16-132MR).

In October 2015, ANZ agreed to compensate more than 70 borrowers for car loans organised by Get Approved Finance (refer: 15-312MR).

The IMF has published an excellent piece on their blog, which sharply defines the issues around bank bail-out and bail-in should a bank fail.

The trouble is the “bail-in” route which they define as targetting “Sophisticated Investors” such as super funds, effectively means a indirect risk to households who save via their superannuation, and of course there is the risk that even deposits could be grabbed as is explicitly stated in New Zealand.

The IMF argues that the risk of bail-in means prospective investors should see a premium to cover the risk, in the returns they get from their investments. But it seems to me in an attempt to deflect risks away from governments being forced to bail-out a bank, once again the end user of financial services products are effectively taking the risks, and creating a moral hazard, where banks and governments can pass the buck.

Watch my previous video:

During the global financial crisis, policymakers faced a steep trade-off in handling bank failures. Using public funds to rescue failing banks (bail-outs) could weaken market discipline and lead to excessive risk taking—the moral hazard effect.

Letting private investors absorb the losses (bail-ins) could destabilize the financial sector and the economy as a whole—the spillover effect. In most cases, banks were bailed out.

This created public resentment and prompted policymakers to introduce measures to shift the burden of bank resolution away from taxpayers to private investors.

Resolving a failing bank should rely on bail-ins: private stakeholders should bear the losses.

Our recent study, also featured in an Analytical Corner in the 2018 Spring Meetings, looks at the question of what to do when a bank fails.

We advocate a resolution framework that carefully balances the moral hazard and spillover effects and improves the trade-off. Such a framework would make bail-outs the exception rather than the rule.

Balancing moral hazard and spillover effects

Not all crises are alike. Some are isolated, with little or no spillover effect. In those cases, bail-outs would merely create moral hazard. Resolving a failing bank should rely on bail-ins: private stakeholders should bear the losses.

Other crises are systemic, and affect all corners of an economy or many countries at the same time.

The destabilizing spillovers associated with bank failures in such a situation would justify the use of public resources: moral hazard still exists but is bearable compared to the alternative of a severe crisis that hurts all, including those without a stake in the troubled bank.

So, the framework should commit to using bail-ins in most cases and allow use of public funds only when the risks to macro-financial stability from bail-ins are exceptionally severe.

Improving the trade-off

The best way to avoid such dilemmas is to reduce spillovers and the need for bail-outs in the first place. This can be achieved through two mutually re-enforcing mechanisms.

The first mechanism is reducing the likelihood of crises and minimizing costs should a crisis occur. This translates into having a more resilient banking system: less leverage and risk taking, and more capital and liquidity. Then the odds that a bank runs into trouble are smaller. And, if there is trouble, banks can absorb the losses without help from the government.

The second mechanism is making the bail-in option viable. The problem is that policymakers may make the promise to bail in a troubled bank but, in a crisis, they will be tempted to bail them out. So people will not believe that bail-ins will happen and continue to expect bail-outs.

This is the worst of both worlds, because it has spillover and moral hazard effects.

How do policymakers make a credible commitment that there really will be bail-ins?

First, ensure that banks have enough buffers to absorb losses and clarify upfront which investor claims (such as bonds and deposits) will in the event of failure be written down and in what order. Second, only allow sophisticated investors who can understand and absorb the losses to hold these bail-in-able claims. Third, improve systemic banks’ resolvability by periodic assessments, living wills that spell out how the bank will be resolved, and domestic and cross-border drills to assess the impact of a threat.

Turning to the other side of the trade-off, how do we limit moral hazard?

First, credibly commit to using bail-outs only in exceptional cases and on a temporary basis with a clear exit plan. Second, use public funds only after those that can absorb the losses have been bailed in. Third, recover these bail-out funds after the storm has passed and ensure that all is executed in a transparent, accountable manner.

The way forward

Reforms since the crisis have improved the trade-off by seeking to make bail-ins a credible option and to make bail-outs less likely.

New frameworks—such as those in the United States and the European Union—introduce comprehensive powers to resolve banks, including through bail-ins. These measures also seek to contain spillovers from bail-ins by ensuring that banks have adequate buffers to absorb losses, and aim to make them more resolvable via effective resolution planning.

We support the ongoing reform agenda and stress that resolution frameworks should minimize moral hazard. That said, we also emphasize the need to allow for sufficient, albeit constrained, flexibility to be able to use public resources in systemic crises—when spillovers are deemed likely to severely jeopardize macro-financial stability.

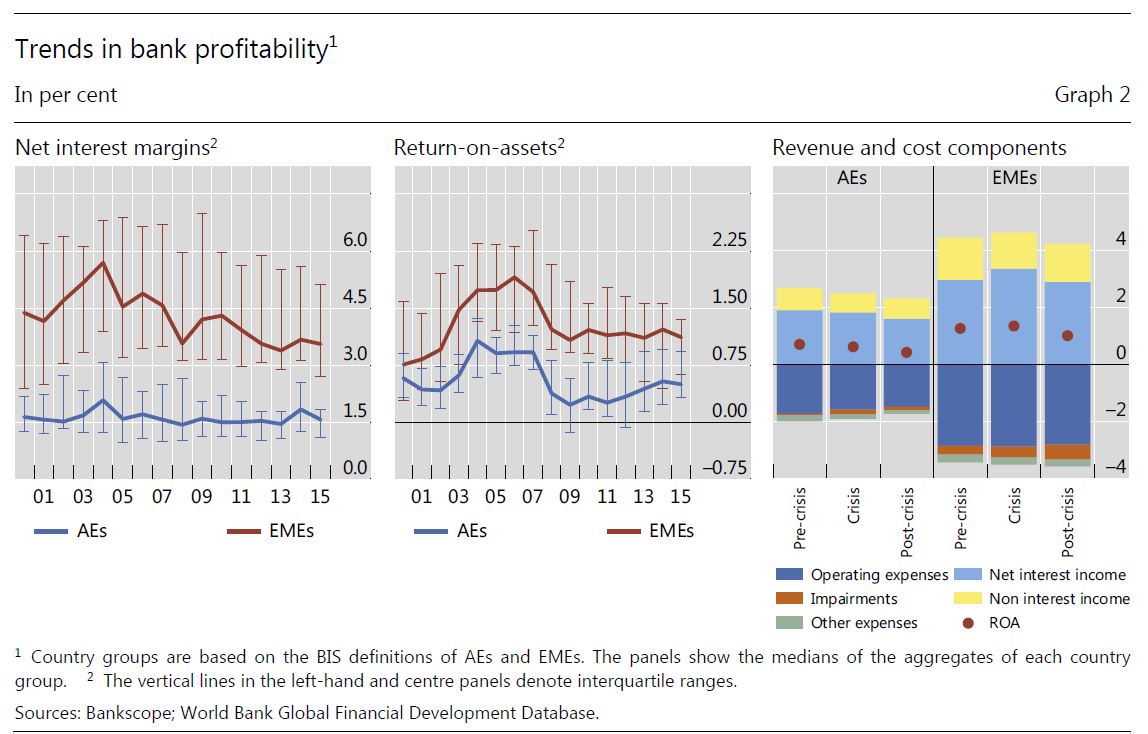

The BIS is worried by the current low interest rate environment, and in a new report by a committee chaired by Philip Lowe warn of the impact on financial stability across the financial services sector, with pressures on banks via net interest margins, and on insurers and super funds. They warn that especially in competitive markets, risks rise in this scenario. Low interest rates may trigger a search for yield by banks, partly in response

to declining profits, exacerbating financial vulnerabilities.

In addition, keeping rates low for longer may create the need to lift rates sharper later with the risks of rising debt costs and the broader economic shock which follows. A salutatory warning!

Interest rates have been low in the aftermath of the Global Financial Crisis, raising concerns about financial stability. In particular, the profitability and strength of financial firms may suffer in an environment of prolonged low interest rates. Additional vulnerabilities may arise if financial firms respond to “low-for-long” interest rates by increasing risk-taking.

The decade following the Great Financial Crisis (GFC) has been marked by historically low interest rates. Yields have begun to recover in some economies, but they are expected to rise only slowly and to stabilise at lower levels than before, weighed down by a combination of cyclical factors (eg lower inflation) and structural factors (eg productivity, demographics). Moreover, observers put some weight on the risk that interest rates may remain at (or fall back to) very low levels, a so-called “low-forlong”

scenario. An environment characterised by “low-for-long” interest rates may dampen the profitability and strength of financial firms and thus become a source of vulnerability for the financial system. In addition, low rates could change firms’ incentives to take risks, which could engender additional financial sector vulnerabilities.

In light of these concerns, the Committee on the Global Financial System (CGFS) mandated a Working Group co-chaired by Ulrich Bindseil (European Central Bank) and Steven B Kamin (Federal Reserve Board of Governors) to identify and provide evidence for the channels through which a “low-for-long” scenario might affect financial stability, focusing on the impact of low rates on banks and on insurance companies and private pension funds (ICPFs).

Now a report by the Committee on the Global Financial System finds that low market interest rates for a long time could have implications for financial stability as well as for the health of individual financial institutions. Philip Lowe, Chair, Committee on the Global Financial System and Governor, Reserve Bank of Australia said:

“The adjustment of financial firms to a low interest rate environment warrants further investigation, especially when low rates are associated with a generalised overvaluation of risky assets. I hope that this reports provides both a sound rationale for ongoing monitoring efforts and a useful starting point for future analysis”.

For banks, based on econometric evidence, simulation models, and reviews of past stress tests, the Working Group found considerable evidence that low interest rates and shallower yield curves depress net interest margins (NIMs). This effect was more pronounced for banks facing constraints on their ability to reduce deposit rates, for example, because of very low interest rates or strong competitive pressures. low rates might reduce resilience by lowering profitability, and thus the ability of banks to replenish capital after a negative shock, and by encouraging risk-taking. These effects can be expected to be particularly relevant for banks operating in jurisdictions where nominal deposit rates are constrained by the effective lower bound, leading to compressed net interest margins. For banks in emerging market economies (EMEs), such adverse effects might materialise not only as a result of low domestic interest rates but also as a consequence of “spillovers” from low interest rates in advanced economies (AEs), which can encourage capital inflows into EMEs, excessive local credit expansion, and heightened competitive pressures for EME banks.

Lower for longer would be harder on insurers and pension funds than on banks. Even though the CGFS analysis did not show that measures of firms’ financial soundness dropped significantly, prolonged low rates could still involve material risks to financial stability. In particular, a “snapback”, involving an unexpected sudden increase in market rates from currently low levels, could affect banks’ solvency and create liquidity issues for insurers and pension funds.

“A key takeaway is that, while a low-for-long scenario presents considerable solvency risk for insurance companies and pension funds and limited risk for banks, a snapback would alter the balance of vulnerabilities,”

Chair Philip Lowe, said.

“The first line of defence against these risks should be to continue to build resilience in the financial system by encouraging adequate capital, liquidity and risk management. But the report also underscores the need to monitor institutions’ exposures in a comprehensive way, including through stress tests.”

The CGFS is a central bank forum for the monitoring and analysis of broad financial system issues. It supports central banks in the fulfilment of their responsibilities for monetary and financial stability by contributing appropriate policy recommendations.

Superannuation funds have made some strides in transitioning to digital platforms and online communication, but the process has been challenging for them, according to Investment Trends; via InvestorDaily.

Researcher Investment Trends’ latest Super Fund Member Engagement report, compiled from surveys of the member services and activities of Australia’s largest 44 super funds, has found that super funds are “still learning to manage” their move to the online space.

“Many super funds are making inroads in the development of their digital member service platform, but the move from internal processing systems to real-time member facing applications has been challenging,” said a statement from Investment Trends.

Investment Trends technology analyst Ian Webster said the report found several super funds encountered various online stumbling blocks.

“This year, we observe many funds struggling with the reliability, consistency and quality issues in the real-time digital-based channels used to support and interact with their members,” he said.

“However, super funds are gradually mastering the challenge of managing these channels more effectively, building upon basic content publishing towards digital channels that provide easy access to services and promote two-way engagement with members.”

Among the top 10 super funds ranked according to overall member engagement score, nine were industry funds, with ANZ Smart Choice representing the only retail fund at tenth place.

AustralianSuper took out first place, followed by Sunsuper, HESTA, QSuper, HOSTPLUS, Rest Super, Cbus Super, Vic Super and NGS Super.

Mr Webster pointed to HESTA, Sunsuper and AustralianSuper which had all made developments to their website and were “shining examples of industry funds adopting a ‘member first’ approach”.

“The last 12 months alone saw a host of interesting developments by super funds, including an increase in the number of fund mobile apps, increased social media activity, and direct engagement through online chat and bot-based applications,” he said.

And insurance agents were able to exploit and target Aboriginal people because the industry isn’t fully regulated.

The cultural, economic and political arrangements that allow this to happen are called “practice architectures”. They include the complex language used to deceive consumers into buying unsuitable products, incentivised high pressures sales tactics, and a lack of care and concern for vulnerable consumers.

All of these aspects are within the scope of financial regulators. The funeral insurance industry can push dodgy products because no one is watching. Predatory financial practices will continue until governments and/or regulators do something about it.

Changing exploitative and predatory financial practices

To change predatory financial practices requires regulatory action to constrain the ability to exploit vulnerable consumers. Educating consumers about predatory financial practices and fostering critical thinking skills is also needed.

But financial literacy education alone is not enough when deliberate deception in financial products and services is permitted.

Research shows Indigenous Australians are too trusting in the role of government to regulate financial matters and can fall prey to predatory lenders. For example, the researchers found there was a belief the Australian Securities Investment Commission would check the accuracy of all prospectuses and that personal loan interest rates are legislated.

To ensure vulnerable consumers are protected requires a lot more than financial education. It requires regulation.

This meant an applicant going to a broker was more likely to end up with a larger mortgage over a longer term than one who dealt directly with their bank, a finding that was revealed in a review of the industry.

Consumers best interest must put be above those of the agents when it comes to insurance products and mortgages.

Much like how certified financial planners are now mandated under the corporations act to work in the best interest of their clients.

The royal commission has also revealed funeral insurance agents gave the appearance of being an Aboriginal organisation, while deliberating exploiting Aboriginal people.

Fixing the problem requires the Australian Securities Investment Commission to change the predatory financial practices so the financial landscape can operate ethically.

In the case of mortgage brokers, exploitative practices were encouraged based on the way brokers are remunerated. So how brokers are remunerated has been changed to align with the best interest of the client.

Selling insurance similarly has a number of cultural, social and financial elements that can be acted upon. There are the cultural aspects of what it means to be a broker, the economic incentives to push clients towards certain products, and social elements that encourage agents to put their own needs ahead of those wanting insurance to protect and cover their loved ones.

Together, these arrangements form practice architectures which make it possible to constrain the practices used in mortgage broking and the insurance industry. Different practice architectures are required to make possible other, non-predatory, methods of mortgage-broking and selling insurance.

Once what it means to be an ethical mortgage broker or an ethical funeral insurance agent becomes the norm, then the social and cultural concern for others’ well-being may be realised.

Predatory financial practices will not go away without effective regulation. The finance and insurance industry needs more effective regulation that forces higher ethical standards to be met in order to establish new financial practices.

This change can begin by asking whether the financial practices that have already been exposed are rational, reasonable, productive, sustainable, socially just or inclusive. And since they aren’t, what action can be taken to change the unjust financial practices? More and better regulation to protect consumers.

Author: Levon Ellen Blue Lecturer, Queensland University of Technology

Dwelling investment has gone from making a positive contribution to growth two years ago to being roughly flat over the year to March. In terms of our forecasts, dwelling investment is not expected to contribute much to growth over the next couple of years, but is expected to remain at a high level.

To understand the outlook, it is helpful to recognise that there isn’t a single national housing market. At the state level, there have been some similarities in the evolution of dwelling investment, but there have also been distinct differences (Graph 5).

Graph 5

One point of similarity is that the construction of higher-density apartments has been much more important than in the past, especially in the east-coast capitals. We have used our liaison program quite extensively to understand how to adapt our forecasting processes to take into account that the time taken for a building approval to progress to construction and the period of construction is longer and more variable for high-density projects than for detached dwellings. The liaison program, which includes organisations such as the UDIA and its members, has also allowed us to gain deeper insights into specific local factors, such as differences in planning rules and the emergence of capacity constraints in the housing construction sector.

One point of difference across states has been the timing of dwelling investment cycles. For New South Wales and Victoria, the level of dwelling investment has been broadly stable at a high level since 2016. In contrast there has been a decline in higher-density construction in Queensland since early 2017. In Western Australia, residential construction peaked in mid 2015, which was well after the end of the mining boom. These differences highlight the fact that there are different demand and supply forces at work across the states. Given time constraints, I am going to focus my attention on the demand side of the market.

An important driver of housing demand over the long run is the rate at which new households are being formed. This depends on population growth and changes in the average number of people who are living in each household. Household size declined steadily in Australia between 1960 and 2000 before levelling out, alongside declines in marriage and fertility rates and population aging. The natural increase in the Australian population has also declined over time due to demographic factors. In particular, lower fertility rates have offset increased life expectancy (Graph 6). Having said that, the rate of natural increase in Australia’s population remains higher than in most other advanced economies.

Graph 6

Immigration has also been a feature of the population growth story and it has certainly been the dominant influence on the swings in population growth over the past decade. The largest single category of net overseas migration has been people on temporary student visas (Graph 7). Prior to the financial crisis, a large share of these students were coming to Australia for vocational training courses. Following changes to visa requirements, student visa numbers initially dropped, but have picked up again in recent years, mostly due to an increase in students attending university. To put this into perspective, education now accounts for around 10 per cent of Australia’s total exports, which is in the same ball park as our rural exports. From the perspective of demand for housing, the important point is that most of these students have gone to Sydney and Melbourne.

Graph 7

Another interesting category is skilled workers. The net inflow of people on skill visas increased in response to demand for workers during the mining boom. Most of these workers went to Western Australia and Queensland. At the same time, net migration to Western Australia and Queensland from other states and New Zealand also increased. As the mining sector transitioned from the construction to the production phase of the mining boom, the demand for labour fell. The number of people on skilled visas fell and the inflow of people from New Zealand and other Australian states turned to an outflow.

As a consequence, there have been quite large differences in population growth at the state level, which have had direct effects on the demand for housing (Graph 8). Population growth is expected to remain strong, particularly in Victoria and New South Wales, and the net overseas migration component of this is expected to be driven by people on student visas.

Graph 8

On the supply side, the pipeline of residential construction that has been approved, but not completed remains high in New South Wales and Victoria (Graph 9). There is also a reasonable pipeline of work in Queensland, although it has already started to decline. Based on recent approvals data and expected demand conditions, this suggests that dwelling investment in New South Wales and Victoria will remain at a high level for a number of years. Liaison contacts have suggested to us that capacity constraints in the construction industry, particularly in New South Wales, will make it difficult for construction activity to increase.

Graph 9

Of course household formation and population growth are not the only drivers of housing demand. For example, interest rates and changes in lending standards can also influence how much households are willing and able to spend on housing. Another way to gauge the current balance of housing supply and demand is to look at housing price growth.

Over the past five years, housing price growth has been subdued in Brisbane and Perth (Graph 10). This is consistent with the fall in population growth coinciding with an increase in the supply of housing. In contrast, housing price growth has been strong until recently in Sydney and Melbourne, where population growth has been strong. Given that housing accounts for around 55 per cent of total household assets, we are paying close attention to these developments.

Graph 10

The Housing Market in the Illawarra Region

From a demand perspective, the Illawarra region has experienced a pick-up in population growth. Some of this has come from overseas students attending the University of Wollongong, and some has come from people migrating to the Illawarra region from Sydney. Although the Illawarra region is a little older, on average, than the rest of Australia and Sydney, it still has a large working-age population (Graph 11).

Graph 11

This is partly because its geographic proximity and transport infrastructure allow people living in Wollongong and the Illawarra region to commute to Sydney. Around 20 per cent of Wollongong workers commute at least 50 kilometres to work (Graph 12). This is one of the highest rates in the state. Unsurprisingly, five of the seven areas with higher shares of people commuting more than 50 kilometres are also within commuting distance of Sydney. Illawarra residents are also well placed to benefit from the fact that some of the fastest growing areas of Sydney are in south and south-west, including the proposed “aerotropolis” around the new airport at Badgery’s Creek. Access to these growth areas will be enhanced if some of the recently announced transport infrastructure plans are realised.

Graph 12

Although people from the Illawarra region can and do commute to Sydney, labour market conditions in the Illawarra region itself have also been strong recently (Graph 13). In combination, these factors mean that there has been strong employment growth for those living in the Illawarra region over the past five years and the unemployment rate is close to the average for New South Wales, which is, in turn, lower than the Australian unemployment rate.

Graph 13

Strong population growth and the economic prosperity associated with strong labour market outcomes have led to higher housing prices in the Illawarra region (Graph 14). Just as in Sydney, developers have responded to the higher prices, and dwelling investment in the region has increased. Also similarly to Sydney, there has been a debate about whether the infrastructure has been growing fast enough to accommodate the needs of an expanding population and the increase in construction that goes with that.

Graph 14

Conclusion

In summary, over the past couple of years, non-mining business investment has become a more important driver of growth in the Australian economy. This is a good thing because investment of this kind is necessary to ensure future productivity growth, which is ultimately what contributes to the economic prosperity and welfare of the Australian people. Infrastructure investment has been a part of this story.

At the same time, dwelling investment growth has eased off. Although dwelling investment is still expected to remain at a high level, particularly in New South Wales and Victoria, it is not likely to contribute much to growth over the next couple of years. Demand for housing remains strong because population growth is expected to stay strong. However, the housing story is different across states and across regions within states, partly because population trends differ. The effects of the mining investment cycle on population trends and housing markets in Western Australia is a clear-cut illustration of this point.

The data show that population trends and housing market developments in the Illawarra region are closely linked to those in Sydney, partly because the transport infrastructure allows people to live in the Illawarra region and commute to Sydney. Future transport infrastructure plans and the development associated with the Badgery’s Creek airport are likely to strengthen these ties. As always, the key to effective urban development is high-quality, transparent cost-benefit analysis of potential infrastructure projects informed by local knowledge. The UDIA has an important role to play here. The UDIA and its members, in Wollongong and elsewhere, also have an important role to play in macroeconomic policy by informing the Bank’s understanding of the factors at play in different housing markets through our liaison program.

ASIC says an investigation into loan fraud has resulted in a permanent ban of former National Australia Bank employees, Danny Merheb and Samar Merjan (also known as Samar Awad) from engaging in credit activities and providing financial services.

NAB alerted ASIC to the misconduct of its former employees, alleging that bank staff in the greater western Sydney area were accepting false documents in support of loan applications.

Mr Merheb was found to have recklessly given NAB false payslips, letters of employment, bank statements and statutory declarations in respect of home loan applications. Ms Merjan was found to have knowingly and recklessly given NAB false payslips and letters of employment in respect of personal loan and credit card applications.

The false information and documentation submitted by Mr Merheb and Ms Merjan were primarily provided to them by a third person who had no association with NAB.

ASIC also found that:

Mr Merheb falsely attributed a loan as being referred to NAB by an introducer who was a friend in order for the friend to receive commissions dishonestly;

Ms Merjan assisted the third person in the creation of two false documents, which she subsequently provided to NAB in support of lending applications; and

Ms Merjan was twice offered cash by the third person to process lending applications.

ASIC’s investigation is continuing.

Background

Mr Merheb and Ms Merjan were permanently banned on 29 June 2018. They both have the right to lodge an application for review of ASIC’s decisions with the Administrative Appeals Tribunal.

On 16 November 2017, NAB announced a remediation program for home loan customers after an internal review, prompted by whistleblower reports it had received which found that some home loans may not have been established in accordance with NAB’s policies.

NAB identified that around 2,300 home loans since 2013 may have been submitted with inaccurate customer information and/or documentation, or incorrect information in relation to NAB’s Introducer Program.

The banking and financial services Royal Commission has unearthed the unethical practices and incentives of life insurers selling policies over the phone at the expense of the most vulnerable customers living in remote communities; via Financial Standard.

ASIC Indigenous Outreach Program senior policy analyst Nathan Boyle highlighted the rampant practice of signing up customers by being forced into policies they allegedly didn’t need or unwittingly signed up for.

Based on listening to several phone calls from ClearView Life Insurance, Boyle alleged staff coaxed customers into providing bank details and enough personal information which then entered them into a contract without knowing, he said.

This is the way “gratuitous concurrence can play out in practice,” he added.

Boyle was referring to ASIC’s review of ClearView in February, which used unfair and high pressure sales tactics when selling life insurance direct to consumers over the phone between 1 January 2014 and 30 June 2017.

Of 32,000 life insurance policies sold, 1166 were to consumers residing in areas with high indigenous populations that unlikely spoke English as their first language.

ClearView has since ceased selling life insurance directly to consumers and refunded $1.5 million to thousands of customers as a result of poor sales practices.

The Commission heard the story of Kathy Marika, an indigenous woman who was convinced into buying a funeral insurance policy with Let’s Insure (which is owned by Select AFSL) even though she was already covered.

Marika said she couldn’t fully understand the representative, who spoke over her and at great length and initially believed was calling about a survey. Ultimately, she said the representative was “forcing” her to sign up to a policy that deducted $60 per month from her account.

“I told them that I didn’t want it. I told them I’ve already had one, but he seemed to be really pushing or asking me to say ‘yes,'” she said.

When Marika eventually decided to cancel the policy, she said Let’s Insure was relentless with the phone calls.

Senior Counsel Assisting Rowena Orr asked: “And in your statement you say that sometimes they called you day after day and sometimes once a week?”

“Well, they never left me alone,” Marika said.

She eventually ran into financial difficulty and sought the assistance of Legal Aid. She told them she could no longer afford the funeral insurance.

In a written response, Let’s Insure said it disputes the allegations it didn’t act properly and in accordance with the law when it sold the policy.

“However, as an act of goodwill, we will refund all premiums paid on the above policies, currently 40 totalling $1,890.34, subject to your client’s authorisation for us to cancel their policies,” Let’s Insure said.

Select AFSL managing director Russell Howden admitted that in hindsight “we pushed our agents” and this practice was “regrettable.”

Some staff members were incentivised with a Vespa scooter and a cruise – which he conceded drove the wrong behaviour.

“We have evolved our commission structure. It was designed to make agents productive but, at all times, the intended outcome was compliant sales,” he said.

A Roy Morgan survey released in January found the phone was the most popular means of purchasing life insurance policies.

In Sydney, of the 442 listed, 84 were withdrawn, and 179 sold. In Melbourne, 526 were listed, 29 withdrawn and 236 sold. Last year at this time, clearance rates were more than 10% higher, on larger volumes.

In Sydney, of the 442 listed, 84 were withdrawn, and 179 sold. In Melbourne, 526 were listed, 29 withdrawn and 236 sold. Last year at this time, clearance rates were more than 10% higher, on larger volumes. Brisbane listed 57, 6 were withdrawn and 17 Sold. Adelaide listed 43, withdrew 1 and sold 13. Canberra listed 47, sold 30 and 3 were withdrawn.

Brisbane listed 57, 6 were withdrawn and 17 Sold. Adelaide listed 43, withdrew 1 and sold 13. Canberra listed 47, sold 30 and 3 were withdrawn.