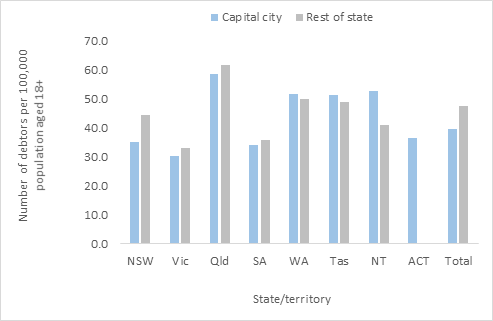

The latest data from The Australian Financial Security Authority (AFSA), regional personal insolvency statistics for the December quarter 2017, shows that on a relative basis more are in distress in the regions than in the major centres.

That said, there were 7,687 debtors who entered a new personal insolvency in the December quarter 2017 in Australia. Of these, 4,785 debtors or 62.2% were located in greater capital cities.

That said, there were 7,687 debtors who entered a new personal insolvency in the December quarter 2017 in Australia. Of these, 4,785 debtors or 62.2% were located in greater capital cities.

New South Wales – There were 1,320 debtors who entered a new personal insolvency in Greater Sydney in the December quarter 2017. The regions with the highest number of debtors were Campbelltown (NSW) (91), Wyong (80) and Gosford (74). There were 913 debtors who entered a new personal insolvency in rest of New South Wales in the December quarter 2017. The regions with the highest number of debtors were Newcastle (51), Lower Hunter (41) and Wagga Wagga (40).

Victoria – There were 1,064 debtors who entered new personal insolvencies in Greater Melbourne in the December quarter 2017. The regions with the highest number of debtors were Wyndham (72), Tullamarine – Broadmeadows (65) and Casey – South (63). There were 367 debtors who entered a new personal insolvency in rest of Victoria in the December quarter 2017. The regions with the highest number of debtors were Geelong (54), Bendigo (33) and Ballarat (29).

Queensland – There were 1,021 debtors who entered a new personal insolvency in Greater Brisbane in the December quarter 2017. The regions with the highest number of debtors were Springfield – Redbank (77), Ipswich Inner (60) and North Lakes (54). There were 1,141 debtors who entered a new personal insolvency in rest of Queensland in the December quarter 2017. The regions with the highest number of debtors were Ormeau – Oxenford (102), Townsville (101), Rockhampton (64) and Toowoomba (64).

South Australia – There were 347 debtors who entered a new personal insolvency in Greater Adelaide in the December quarter 2017. The regions with the highest number of debtors were Salisbury (54), Onkaparinga (41) and Playford (40). There were 106 debtors who entered a new personal insolvency in rest of South Australia in the December quarter 2017. The regions with the highest number of debtors were Eyre Peninsula and South West (20), Murray and Mallee (18) and Barossa (16).

Western Australia – There were 776 debtors who entered a new personal insolvency in Greater Perth in the December quarter 2017. The regions with the highest number of debtors were Wanneroo (114), Rockingham (81) and Swan (81). There were 199 debtors who entered a new personal insolvency in rest of Western Australia in the December quarter 2017. The regions with the highest number of debtors were Bunbury (38), Mid West (27) and Goldfields (25).

Tasmania – There were 89 debtors who entered a new personal insolvency in Greater Hobart in the December quarter 2017. The regions with the highest number of debtors were Hobart – North West (30), Hobart Inner (16) and Brighton (13). There were 110 debtors who entered a new personal insolvency in rest of Tasmania in the December quarter 2017. The regions with the highest number of debtors were Launceston (32), Devonport (25) and Burnie – Ulverstone (20).

Northern Territory – There were 55 debtors who entered a new personal insolvency in Greater Darwin in the December quarter 2017. The regions with the highest number of debtors were Darwin Suburbs (19), Palmerston (14) and Litchfield (12). There were 26 debtors who entered a new personal insolvency in rest of Northern Territory in the December quarter 2017. The regions with the highest number of debtors were Alice Springs (12) and Katherine (8).

Australian Capital Territory – In the December quarter 2017, there were 113 debtors who entered a new personal insolvency in the Australian Capital Territory. The regions with the highest number of debtors were Belconnen (32), Gungahlin (32) and Tuggeranong (30).