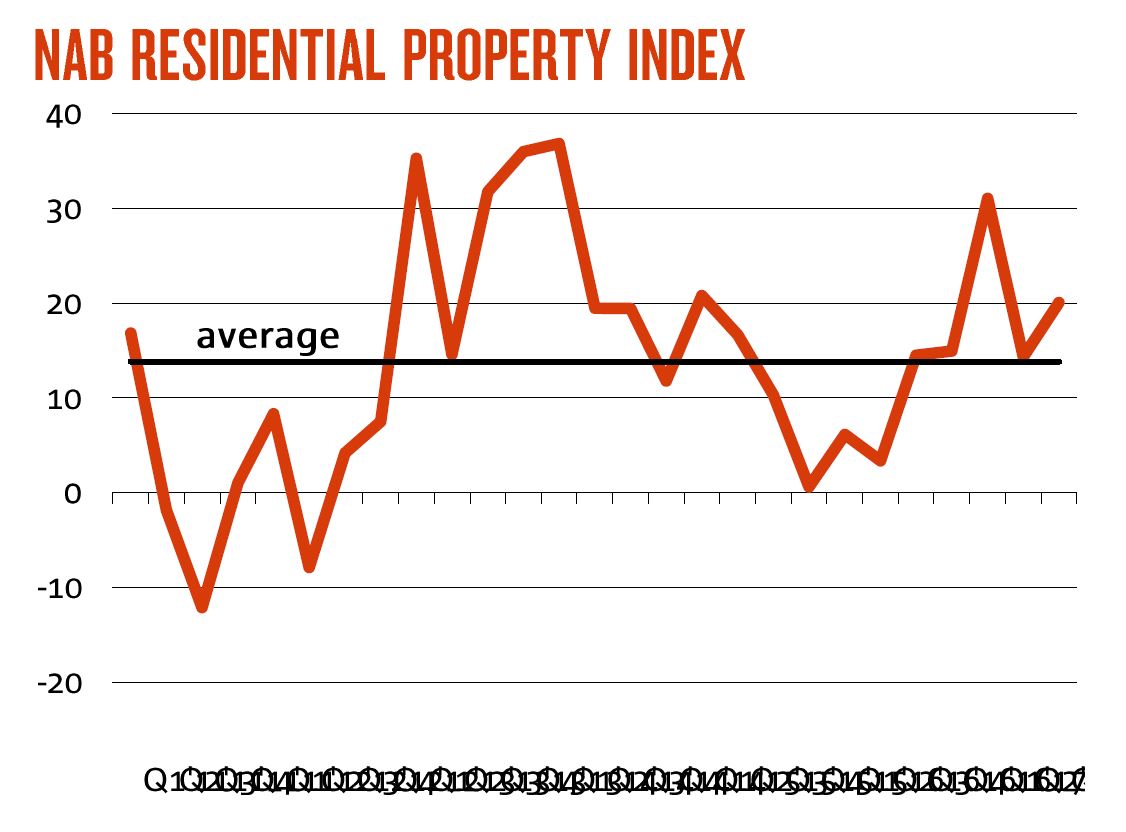

The latest NAB Residential Property Index is out, and it rose 6 points to +20 in Q3, with sentiment (based on current prices and rents) improving in all states except NSW (which edged down). Sentiment rose sharply in Victoria (up 27 to +63) and in Queensland (up 4 to +16). Whilst sentiment rises and confidence lifts among property experts in Q3, NAB expects prices to slow in 2018-19, but not a severe adjustment.

Australian housing market sentiment lifted over the third quarter of 2017, supported mainly by a large increase in the number of property experts reporting positive rental growth in the quarter and continued house price growth in most states.

“The NAB Residential Property Survey shows an improvement in market sentiment across most states last quarter, but we continue to see market conditions that vary across different locations. The momentum is clearly with Victoria, while NSW is experiencing something of a slowdown,” NAB Chief Economist Alan Oster said.

Confidence (based on forward expectations for prices and rents) lifted in all states, led by Victoria, and with WA the big improver. Despite weakening price growth in NSW, higher confidence is being supported by predictions for higher rents.

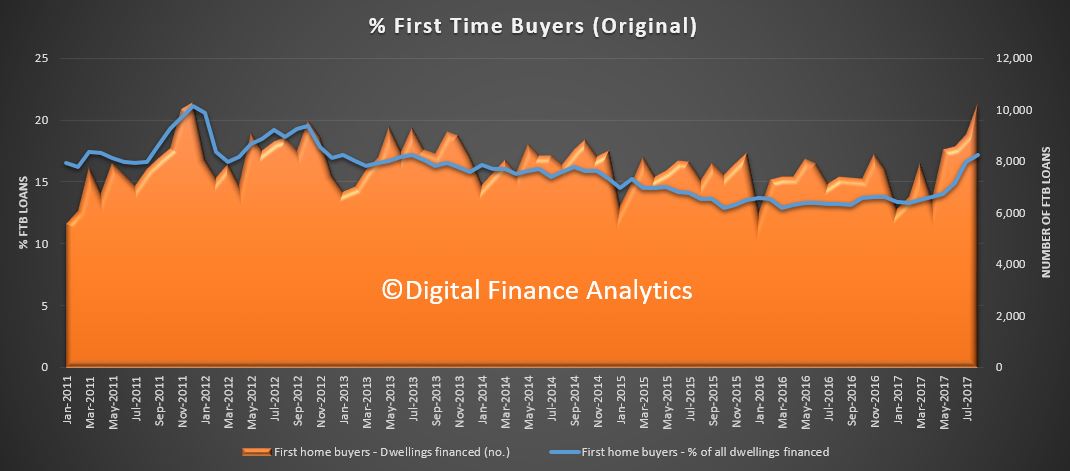

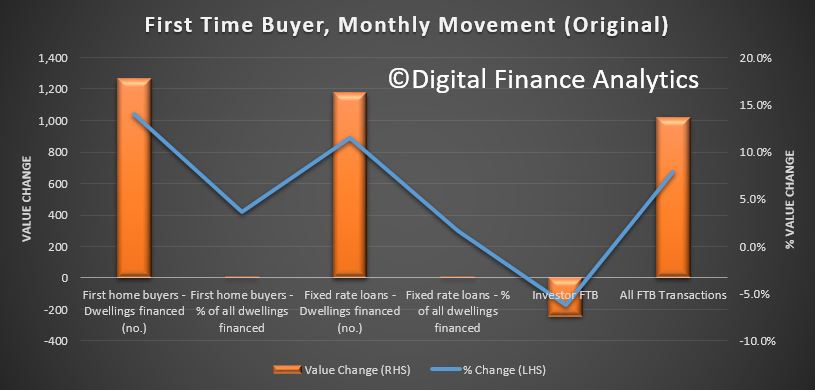

First home buyers continue emerging as key buyers in both new and established housing markets, accounting for over 36% of all sales in new housing markets and around 29% in established markets.

During Q3, the overall market share of foreign buyers in new property markets fell to a 5-year low of 9.5%, potentially due to lending restrictions on foreign buyers. Low foreign buying activity in new property markets was led by Victoria, where the share of sales to foreign buyers fell to 14.4% (20.8% in Q2).

For the first time, tight credit was identified as the biggest constraint on new developments in all states, while access to credit was the biggest barrier for buyers of established property. Price levels were the biggest concern in both Victoria and NSW. In WA and SA/NT, property experts said that employment security was the biggest barrier to buying an established home.

They also highlighted lower foreign buying activity in new property markets, with VIC saw the share fall to 14.4% (from 20.8% in Q2) and NSW down to 7.8% from 12% in Q2. In contrast, QLD saw a rise to 11.4%, up from 8.6% last quarter.

NAB’s forecasts on residential prices

NAB Group Economics has revised its national house price forecasts, predicting an increase of 3.4% in 2018 (previously 4.3%) and easing to 2.5% in 2019. Unit prices are forecast to rise 0.5% in 2018 (-0.3% previously), with a modest fall expected in 2019.

“More moderate market conditions reflect a combination of factors which vary across markets, including deteriorating affordability, rising supply of apartments, tighter credit conditions and rising interest rates in the second half of 2018” said Mr Oster.

“But still relatively low mortgage rates, a favourable housing supply-demand balance and strong population growth population growth should continue to provide support for prices going forward.”

“By capital city, house price growth is forecast to be moderate outside of Perth – where prices are flattening out – consistent with good business conditions and better employment growth.”

“Melbourne and Hobart are currently experiencing solid growth in prices; Sydney is cooling and we expect Brisbane and Adelaide will cool. Finally, we expect 2018 to mark the beginning of a gradual turnaround for Perth.”

About 300 property professionals participated in the Q3 2017 survey.