New data out this week gives an updated read on the state of the property and finance market. We consider the evidence. Welcome to the Property Imperative Weekly to 2nd September 2017.

Starting overseas, we saw lower than expected job growth in the USA, and also lower than expected inflation. Overall, the momentum in the US economy still appears fragile, and this has led to the view that the Fed will hold interest rates lower for longer. As a result, the stock market has been stronger, whilst forward indicators of future interest rates are lower. In fact, half of the jump caused by the Trump Effect last November has been given back. In Europe, the ECB said there would be no tapering until later, again suggesting lower rates for longer.

This change in the international rate dynamics is relevant to the local market, because it means that international funding costs will be lower than expected, and so banks have the capacity to offer attractor rates without killing their margins. The larger players still have around one third of their funding from overseas sources and so are directly connected to these international developments.

This change in the international rate dynamics is relevant to the local market, because it means that international funding costs will be lower than expected, and so banks have the capacity to offer attractor rates without killing their margins. The larger players still have around one third of their funding from overseas sources and so are directly connected to these international developments.

Westpac for example decreased rates on its Fixed Rate Home and Investment Property Loans with IO repayments by as much as 30 basis points. This sets the new fixed rates for owner occupiers between 4.59% p.a. and 4.99% p.a. while rates for investors lie between 4.79% p.a. and 5.19% p.a. They also brought in a two-year introductory offer on its Flexi First Option Home and Investment Property Loan for new borrowers. After two years, the loan will roll over to the base rate which may be more than 70 basis points higher. This may create risks down the track.

Mozo the mortgage comparison site said that twenty-three lenders have dropped their home loan rates since 1 July, showing that competition for good-quality borrowers is hotting up in the lead up to spring, with lenders offering lower interest rates, fee waivers, or lower deposits for favoured customers. Mozo’s research found the most competitive variable rate in the market for a $300,000 owner-occupier loan is 3.44 per cent, which is 120 basis points lower than the average Big 4 bank variable rate. Borrowers should shop around.

Elsewhere, Heritage Bank, Australia’s largest customer-owned bank, said it had temporarily stopped accepting new applications for investment home loans, to ensure they comply with regulatory limitations on growth. They have experienced a sharp increase in the proportion of investment lending in their new approvals recently, partly due to the actions other lenders in the investor market have taken to slow their growth.

APRA’s monthly data for July revealed a significant slowing in the momentum of mortgage lending. Bank’s mortgage portfolios grew by 0.4% in July to $1.58 trillion, the slowest rate for several months. This, on an annualised basis would still be twice the rate of inflation. Investment loans now comprise 35.08% of the portfolio, down a little, but still a significant market segment.

Owner occupied loans grew 0.5% to $1.02 trillion while investment loans hardly grew at all to $552.7 billion, the slowest growth in investment loans for several years. So the brakes are being applied in response to the regulators, although individual lenders are showing different outcomes.

The ABA released a report showing that Less than one third of those surveyed had high levels of trust in the banking industry. This is below the international benchmark. There are significant differences in attitude between those who have higher levels of trust, and those who do not. Those with low trust scores believed the banks were drive by profit, not focussed on customer needs and had terms and conditions which are not transparent.

APRA also released their Quarterly ADI Real Estate and Performance reports to June 2017. Overall, major banks are highly leveraged, and more profitable. Net profit across the sector, after tax was $34.2 billion for the year ending 30 June 2017, an increase of $6.5 billion (23.5 per cent) on 2016. Provision were lower, with impaired facilities and past due items at 0.88 per cent at 30 June 2017, a decrease from 0.94 per cent at 30 June 2016. The return on equity was 12.0 per cent for the year ending 30 June 2017, compared to 10.3 per cent for the year ending 30 June 2016. Looking at the four major banks, where the bulk of assets reside, we see that the ratio of share capital to assets is just 5.4%, this despite a rise in tier 1 capital and CET1. This is explained by the greater exposure to housing loans where capital ratios are still very generous, one reason why the banks love home lending. Thus the big four remain highly leveraged.

The APRA Real Estate data shows ADIs’ residential mortgage books stood at $1.54 trillion as at 30 June 2017, an increase of $105.2 billion (7.3 per cent) on 30 June 2016. Owner-occupied loans were $1,006.2 billion (65.3 per cent), an increase of $75.8 billion (8.1 per cent) from 30 June 2016; and investor loans were $535.7 billion (34.7 per cent), an increase of $29.4 billion (5.8 per cent) from 30 June 2016. Whilst APRA use a different and private measure of interest only loans, their data showed a significant fall this quarter, although the proportion of new IO loans is still above their 30% threshold. High LVR lending was down again, although there was a rise in loans approved outside standard approval criteria. Loans originated via brokers remained strong, with 70% of loans to foreign banks via this channel, whilst the major banks were at 48%.

Separately the RBA released their credit aggregates for July. Overall credit rose by 0.5% in the month, or 5.3% annualised. Within that housing lending grew at 0.5% (annualised 6.6% – well above inflation), other Personal credit fell again, down 0.1% (annualised -1.4%) and business credit rose 0.5% (annualised 4.2%). Home lending reached a new high at $1.689 trillion. Within that owner occupied lending rose $7 billion to $1.10 trillion (up 0.48%) and investor lending rose just $0.09 billion or 0.15% to $583 billion. Investor mortgages, as a proportion of all mortgages fell slightly. A further $1.4 billion of loan reclassification between investment and owner occupied loans occurred in July 2017, in total $56 billion has been switched, so the trend continues.

Building Approvals for July rose 0.7% according to the ABS, in trend terms, approvals for private sector houses rose 1.0 per cent in July, whilst approvals for multi-unit projects continues to slide. This may well adversely hit the GDP figures out soon. New home sales also declined in July according to the HIA. Sales volumes declined by 3.7 per cent during July 2017 compared with June 2017. Sales for the first seven months of this year are 4.6 per cent lower than in the same period of 2016.

The debate about mortgage broker commissions continues, with a joint submission from four consumer groups to Treasury arguing that brokers don’t always obtain better priced loans for clients than the banks and they don’t always offer a diverse range of loan options. They suggested that given the trust consumers place in brokers, they should all be held to a higher standard than arranging a ‘not unsuitable’ loan for their customers. They should be required to act in the best interests of their customers. Most industry players argue for minor tweaks or retaining the current structure, arguing that first time buyers may be hit, and that the current commissions do not degrade the quality of advice. CBA apologised to Brokers this week. Ian Narev, the outgoing chief executive officer of the Commonwealth Bank, has apologised to brokers for some of the “uncertainties” it has caused. He said the bank was very committed to the broker channel, as the Aussie transaction shows. He acknowledged that while the bank has “never shied away” from wanting to do its own business through its branches and direct channels, using a broker was “good for customers”.

CBA was of course in the news for all the wrong reasons, with APRA saying it would look at the culture of the Bank, following the money laundering claims. The investigation will be run by an independent panel, appointed by APRA for six months after which the regulator will receive a final report, to be made public. Of note is their perspective that capital security is not sufficient to guarantee the long term security of the financial system, – culture and accountability are critical too. Of course the big question will be – is CBA an outlier? Does this also provide more weight to calls for a broader Royal Commission? The bank may also face big penalties if international regulators are forced to act over its breaches of rules around money laundering and terrorism financing. Moody’s says this is credit negative and could damage the bank’s reputation as well as compel it to incur costs and use resources to address any mandated remedial actions

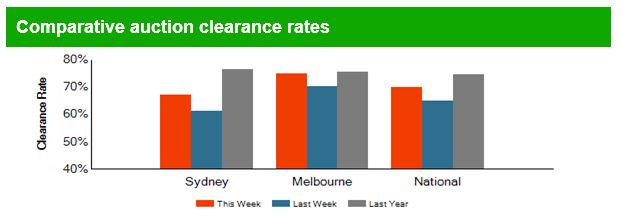

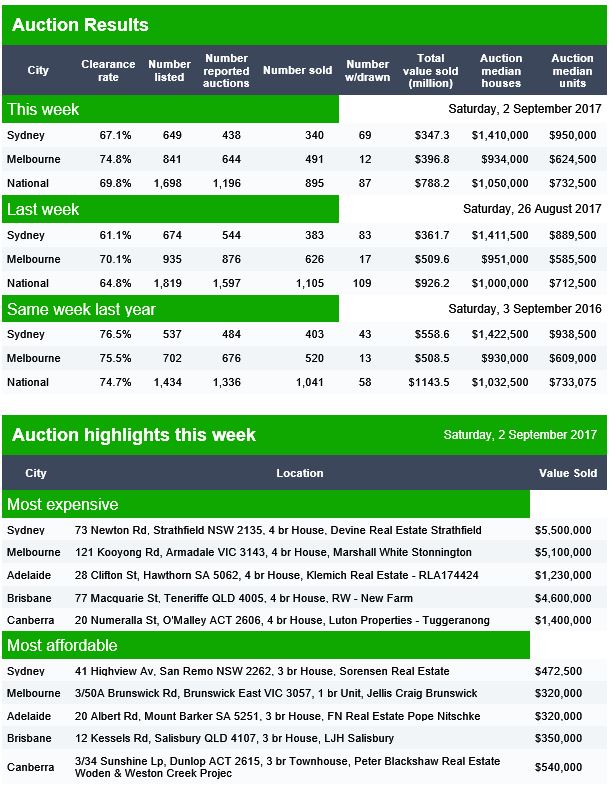

CoreLogic’s revised home price index for August report a 0.1% rise across the capital cities, while regional values fell 0.2%. This was the lowest rolling quarterly gain since June last year. Sydney’s rolling 3-month gain was just 0.3%, with a 13% annual rise. Melbourne was 1.9% in the quarter with 12.7% over the year and Hobart led the pack at 13.6%. Perth and Darwin continue to fall. So the question now is, will the spring surge in sales, and lower mortgage rates support prices, or will we see a fall in the next few months? Auction clearances remain quite strong.

It is worth saying that the strong growth in Australian home prices is nothing unusual as the latest data from the Bank For International Settlements shows. Hong Kong has the strongest growth, and New Zealand and Canada are both well ahead of Australia. We track quite closely with the USA. Spain sits at the bottom of the selected series. The year on year change shows that Australian residential prices are accelerating, whilst the macroprudential measures deployed in New Zealand is slowing growth there. Iceland, Canada and Hong Kong are all accelerating.

So, standing back we see demand for property remaining strong, even if supply of new property is on the slide. Banks are still willing to lend, but are more selective, meaning that some borrowers will find it hard to get a loan, while others will be greeted with open arms and discounts. Banks have the benefits of falling international funding costs and the war chests created by regulator inspired hikes in investor and interest only loans. So we think home prices will continue to find support, and lending will continue to grow overall, even if the mix changes. In addition, we have revised down our expectation of future mortgage rate rises, leading to an estimated fall in the number of defaults, despite the fact that more households are in mortgage stress. We published our updated figures for August on Monday, so look out for that.

And that’s the Property Imperative Weekly to 2nd September 2017. If you found this useful, do subscribe to get future updates and check back for our latest news and analysis on the finance and property market. Thanks for watching.