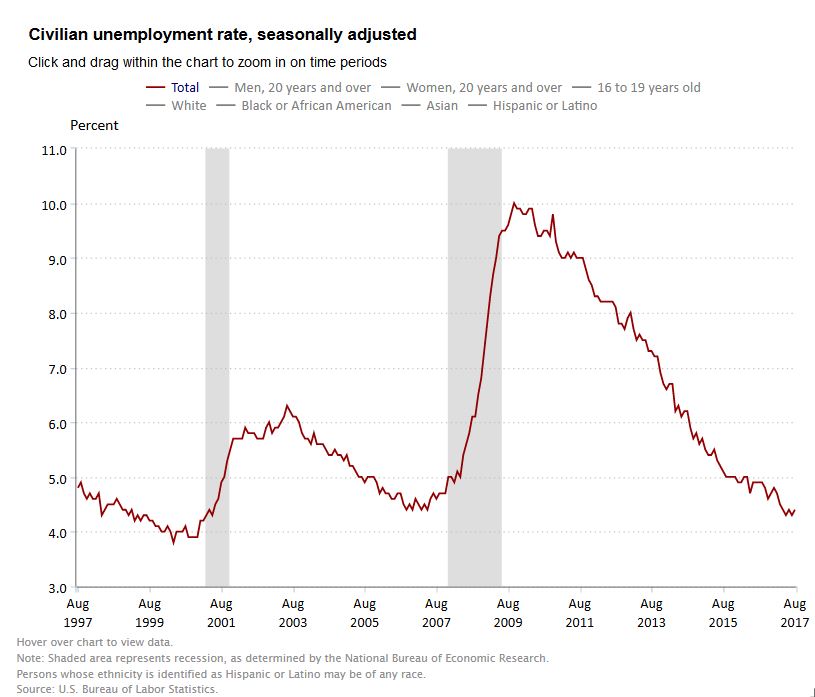

More weaker than expected economic data from the US. Total nonfarm payroll employment increased by 156,000 in August, and the unemployment rate was little changed at 4.4 percent, says the U.S. Bureau of Labor Statistics. The jobs growth was lower than the 186,000 consensus expectation. More evidence supporting the lower for longer interest rate hypothesis.

The number of long-term unemployed (those jobless for 27 weeks or more) was essentially unchanged in August at 1.7 million and accounted for 24.7 percent of the unemployed.

The labor force participation rate, at 62.9 percent, was unchanged in August and has shown little movement on net over the past year. The employment-population ratio, at 60.1 percent, was little changed over the month and thus far this year.

In August, average hourly earnings for all employees on private nonfarm payrolls rose by 3 cents to $26.39, after rising by 9 cents in July. Over the past 12 months, average hourly earnings have increased by 65 cents, or 2.5 percent. In August, average hourly earnings of private-sector production and nonsupervisory employees increased by 4 cents to $22.12.

The change in total nonfarm payroll employment for June was revised down from +231,000 to +210,000, and the change for July was revised down from +209,000 to +189,000. With these revisions, employment gains in June and July combined were 41,000 less than previously reported. (Monthly revisions result from additional reports received from businesses and government agencies since the last published estimates and from the recalculation of seasonal factors.) After revisions, job gains have averaged 185,000 per month over the past 3 months.

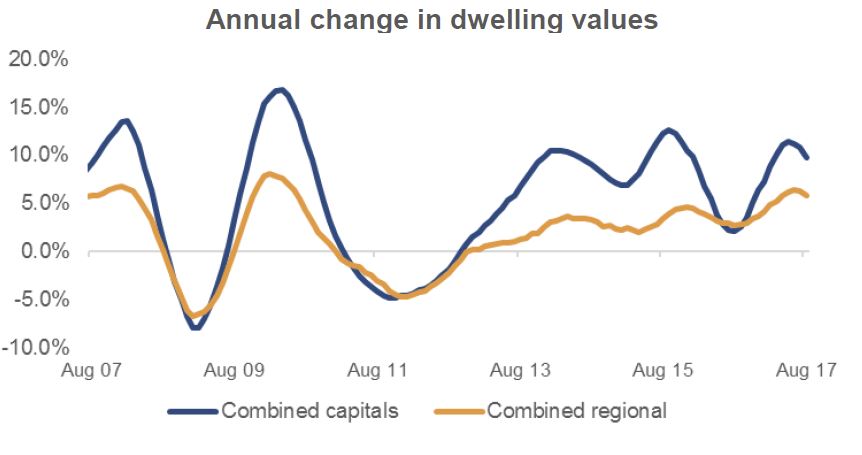

Corelogic has released their new hedonic home value index for August. They report a 0.1% rise across the capital cities, while regional values fell 0.2%.

This was the lowest rolling quarterly gain since June last year. Sydney’s rolling 3 month gain was just 0.3%, with a 13% annual rise. Melbourne was 1.9% in the quarter with 12.7% over the year and Hobart led the pack at 13.6%. Perth and Darwin continue to fall.

So the question now is, will the spring surge in sales, and lower mortgage rates support prices, or will we see a fall in the next few months? One other question of course is whether there are series breaks in the CoreLogic data given the revised method. We shall see in the months ahead.

CoreLogic says:

The hedonic imputation approach – Hedonic regression is a statistical technique that measures the relationship between values of residential real estate and the observed values of its characteristics, for example attributes that encompass its geographic location and property features, such as number of bedrooms and bathrooms etc. The hedonic imputation index model essentially estimates the value of every property each day, using the coefficients derived using hedonic regression, and describes the daily movements in the value of the residential real estate portfolio.

Heritage Bank has said it has temporarily stopped accepting new applications for investment home loans, to ensure they comply with regulatory limitations on growth.

Heritage has experienced a sharp increase in the proportion of investment lending in our new approvals recently.

That’s an outcome both of our attractive pricing structure and the actions other lenders in the investor market have taken to slow their growth.

We need to manage our investment lending portfolio carefully, to ensure we stay within the caps APRA has placed on growth in investor and interest only lending.

As a result, we’ve taken the decision to temporarily stop accepting applications for new investor lending, effective from Friday (1 September).

We will monitor our approvals and loan portfolio in coming weeks and review that decision as needed.

They also announced a tiered pricing structure, based on LVR bands for some products, reflecting the risks involved.

Heritage Bank is Australia’s largest customer-owned bank. In 1981 Toowoomba Permanent Building Society (est. 1875) and the Darling Downs Building Society (est. 1897) merged and became Heritage Building Society. In December 2011, Heritage Building Society officially changed its name to Heritage Bank to remain relevant and competitive.

Commonwealth Bank notes recent media reports concerning compliance and transaction monitoring in offshore jurisdictions by the Institutional Banking & Markets division.

The document referred to in those media reports was a working document, proposing technology enhancements as part of our ongoing Program of Action, including the automation of tasks currently undertaken manually. A combination of automated and manual monitoring is common practice across the industry.

A statement on 9 August 2017, by Commonwealth Bank Chairman Catherine Livingstone AO, noted the progress which has been made under the Program, including an investment to date of more than $230 million to strengthen policies and processes related to financial crimes compliance.

The Program includes investment in systems to enhance transaction monitoring currently performed in Australia and offshore jurisdictions.

The Commonwealth Bank maintains proactive relationships with all relevant global regulators on these and other matters.

A Committee of the Board of the Bank was established on 8 August 2017 to oversee the Bank’s response to AUSTRAC’s statement of claim. This Program is working to strengthen the Group’s anti-money laundering frameworks.

The Committee, which meets weekly, is requesting and considering information and reports from management relating to the progress of the Program, as well as making recommendations to the Board on matters of accountability. The Committee comprises four independent directors: Mary Padbury, who chairs the committee, Catherine Livingstone, Brian Long and Shirish Apte.

The latest data from the US which shows low inflation and wage growth has pulled the implied forward interest rates down suggesting the Fed will hold rates lower for longer. This is reflected in falling yields on the T10.

Nearly half of the “Trump Effect” repricing has been undone.

This is also flowing into lower rates in the international capital markets, which is translating to lower costs of funds for the Australian banks (one reason why Westpac has cut their fixed rates).

As a result, in our default model, we have reduced the likelihood of an interest rate rise for mortgage holders in Australia over the next few months. This will translate to a projected fall in defaults, despite rising mortgage stress. We will publish the August data on Monday. Households are likely to be able to muddle through and the RBA will hope business investment, which was stronger this time, works through.

Meantime, here is interesting commentary from Moody’s on the US, who highlight that the latest drop by personal savings in the US brings attention to the financial stress now facing many households there.

The recent slowdown by the underlying rate of consumer price inflation significantly lowered the risk of a disruptive climb by interest rates. In response, the VIX index sank from the 16.0 points of August 10, 2017 to a recent 10.7 points, while a composite high-yield bond spread narrowed from August 11’s 410 bp to August 30’s 399 bp.

However, the narrowing by the high-yield bond spread has been limited by a climb by the average high yield EDF (expected default frequency) metric from the July 2017 average of 3.9% to the 4.4% average of the five-days-ended August 30. Moreover, the US high-yield credit rating revisions of the third-quarter todate show downgrades topping upgrades even after excluding rating changes that were not primarily driven by fundamentals.

As recently as early July 2017, the Blue Chip consensus had anticipated a 2.5% average for Q3-2017’s 10-year Treasury yield. Much to the contrary, the 10-year Treasury yield has averaged 2.26% thus far in the third quarter, including a recent 2.13%. Not even a widely anticipated September 2017 start to the Fed’s reduced reinvestment of maturing bonds has been capable of lifting Treasury bond yields demonstrably.

In addition to July’s 1.4% annual rate of core PCE price index inflation, benchmark bond yields have been reined in by the market’s much reduced expectation of another Fed rate hike for 2017. As of mid-day on August 31, the futures market implicitly assigned only a 36.4% likelihood to fed funds’ midpoint finishing 2017 at something greater than its current 1.125% according to the CME Group’s FedWatch tool.

By itself, core PCE price index inflation’s performance of the last 20 years suggests that the FOMC may have considerable difficulty as far as sustaining PCE price index inflation at 2% or higher. For the 20-years-ended June 2017, core PCE price index inflation averaged only 1.7% annually. The annual rate of core PCE price index inflation was at least 2% in only 58, or 24.2%, of the last 240 months (20 years).

For those months showing an annual rate of core PCE price index inflation of at least 2%, the average annual rate of core inflation was only 2.2%, wherein the fastest annual rate of core inflation was the 2.5% of August 2006.

Drop by personal savings curbs core inflation

The slower growth of wage and salary income has helped to contain price inflation. After decelerating from 2014’s 5.6% and 2015’s 5.5% to 2016’s 3.0%, the annual increase of private-sector wages and salaries approximated a still sluggish 3.1% during January-July 2017. In response to the pronounced slowdown by wages and salaries, personal savings have shrunk by -29% annually thus far in 2017 following yearlong 2016’s -18% plunge.

The drop by the ratio of personal savings to disposable personal income from its 6.1% average of the five years ended 2015 to the 3.8% of 2017 to date implies Americans lack the financial wherewithal to either support or absorb significantly higher prices for long.

High rates of personal savings make it easier for consumers to absorb higher prices. When core PCE price index inflation averaged 6.4% during 1970-1981, the personal savings rate averaged 11.7%. By contrast, the averages for January-July 2017 showed a much lower 3.8% personal savings rate and a much slower 1.6% annual rate of core PCE price index inflation.

In addition, the latest drop by personal savings brings attention to the financial stress now facing many US households. Today’s more unequal distribution of income implies that a relatively greater number of today’s households save little, if any, of their after-tax income. When confronted with higher prices, these “paycheck-to-paycheck” consumers will be compelled to eventually curtail real spending at the expense of business pricing power.

Westpac has dropped its fixed rates on interest only loans while bringing in new introductory offers on a number of variable rate products.

The bank has decreased rates on its Fixed Rate Home and Investment Property Loans with IO repayments by as much as 30 basis points. This sets the new fixed rates for owner occupiers between 4.59% p.a. and 4.99% p.a. while rates for investors lie between 4.79% p.a. and 5.19% p.a.

“We regularly review our rates. We’ve been adjusting some over the past few months to remain competitive and ensure we meet our composition targets – i.e. the regulator’s 30% sector cap on IO loans,” a bank spokesperson told Australian Broker.

Rates for fixed rate interest only investor loans locked in for between six and 10 years remain unchanged.

Westpac has also brought in a two year introductory offer on its Flexi First Option Home and Investment Property Loan for new lenders. Refinancing and foreign lending is excluded.

Changes include an increased discount for the first two years of the Flexi First Option Home Loan for P&I payments and the introduction of a similar discount for Flexi First Option IO investor loans. After two years, the loan will roll over to the base rate:

2 year intro rate

Discount

Base rate

P&I owner-occupier

3.88% p.a.

0.71% p.a.

4.59% p.a.

P&I investor

4.18% p.a.

0.96% p.a.

5.14% p.a.

IO owner-occupier

5.18% p.a.

None

5.18% p.a.

IO investor

4.88% p.a.

0.77% p.a.

5.65% p.a.

The bank has also removed its revert rate discount from all Flexi First Option Home Loans for owner occupiers and investors.

AFG, Connective, Aussie, Mortgage Choice, Loan Market, Smartline and Specialist Finance Group made submissions in response to ASIC

Aggregators and franchise groups have near-unanimously criticised changes to commissions in their submissions to the Treasury.

Three wholesale aggregators and four franchise groups, representing thousands of brokers, were responding to ASIC’s Review of Mortgage Broker Remuneration, published in March this year.

Connective’s submission summed up the general mood, stating: “the review seems to abandon the existing responsible lending framework, instead seeking to solve a poorly defined problem with an impossible to implement solution.”

Most aggregators rejected all alternative commission arrangements, giving reasons similar to Mortgage Choice’s argument: “to suggest that it would be effective to change the shape or quantum of broker commissions based on LVR, interest-only or lower loan amounts would not be correct. Broker economics need to line up with lender economics and consumer outcomes.”

NAB’s submission proposed upfront commission be linked to the drawn down amount, but only Smartline tentatively endorsed this approach, saying it “may make sense”.

Backing the MFAA, attacking the ABA

In their submissions, aggregators overwhelmingly backed the MFAA and industry self-regulation, which was endorsed yesterday by Minister Kelly O’Dywer.

Aussie and Loan Market pointed to the MFAA’s submission as reflecting their views, with the former noting “[Aussie] believes that potential changes that introduce unreasonable levels of complexity or inconsistency should be avoided. It will, therefore, be necessary to achieve industry consensus on any proposed actions before changes are implemented.”

Aggregators also attacked the Australian Bankers Association and its Sedgwick Review of commissions, with Smartline stating that “it concerns us that the ASIC report references the ABA report, which in our view was manifestly inadequate, lacking in substantive evidence to support recommendations, while being commissioned by a representative group with significant vested interests”

What about bank-owned aggregators?

Choice Aggregation, FAST and Plan Australia were represented within NAB’s submission to the Treasury which proposes major changes to commissions.

Bank ownership did not, however, appear to have an impact elsewhere. Aussie, which as of last week is 100% owned by CBA, was highly critical of changes to commissions.

Connective, which is part-owned by Macquarie, agreed with ASIC that controlling ownership interests should be disclosed to customers, whilst Mortgage Choice, which is ASX-listed, asked for further guidance on what constitutes a controlling interest.

Neither VOW nor Yellow Brick Road were listed among submissions to the Treasury, although it is possible they made anonymous submissions or submissions through the MFAA or FBAA.

On Monday, the Australian Prudential Regulation Authority (APRA) announced that it would establish an independent prudential inquiry into the governance, culture and accountability framework of Commonwealth Bank of Australia (CBA, Aa3/Aa3 stable, a26). APRA’s focus on CBA’s culture and practices is credit negative and could damage the bank’s reputation as well as compel it to incur costs and use resources to address any mandated remedial actions.

APRA has stated that it will make the findings of its review public and that the inquiry will take around six months from its formal commencement. APRA’s regulatory review is the latest of several regulatory issues for CBA. On 3 August, the Australian Transaction Reports and Analysis Centre (AUSTRAC) commenced proceedings against CBA for non-compliance of the Anti-Money Laundering and Counter-Terrorism Financing Act. AUSTRAC alleges that CBA did not carry out a specific assessment of the money laundering and terrorism financing risk of intelligent deposit machines until three years after their introduction, and inadequately monitored and reported suspicious transactions.

We expect more information about the timing of AUSTRAC’s proceedings at the first case-management hearing scheduled on 4 September. We also expect CBA to file a statement of defense. CBA also faces a potential class-action lawsuit from shareholders that allege the bank did not meet its continuous disclosure obligations in relation to the AUSTRAC allegations. The Australian Securities and Investments Commission (ASIC) also has announced that it will investigate whether CBA did not meet these obligations.

In recent years, CBA has dealt with a number of conduct-related issues that have negatively affected the bank’s reputation. In August, ASIC announced that CBA would refund more than 65,000 customers approximately AUD10 million, after selling them unsuitable consumer credit insurance. In March 2016, the bank’s life insurance business, CommInsure, was accused of deliberately avoiding or delaying paying claims to its customers, but in March 2017, ASIC cleared CommInsure of any breaches of the law. However, ASIC identified areas that CBA should improve, which CBA has already done or is committed to doing. Also, CBA in 2014 announced an Open Advice Review program relating to the poor quality of advice and compliance breaches by its financial planning businesses, Commonwealth Financial Planning and Financial Wisdom.

Operational and compliance problems of this nature highlight the challenges of maintaining tight controls at large and complex institutions that span multiple business lines such as retail, commercial and institutional banking, insurance and wealth management. We note that the strong profitability of Australia’s major banks’ domestic franchises and the low credit costs amid an extended period of unusually low interest rates elevates the risk that banks become complacent in the their approach to operational and governance risks.

When Australian companies report results they typically include an outlook statement from the business’ leaders, giving investors some guidance about their expectations for the future. They issue these forward-looking statements with some caution as investors might rely on them, and the law requires that they be based on “reasonable grounds”.

The Conversation’s Face Value uses sentiment analysis to try and determine how Australian business leaders are feeling about the future.

A contradiction is emerging between how consumers should be feeling and what the heads of companies expect them to do. What we know about low wages growth and underemployment seems to suggest households would be tightening the purse strings but the sentiment of business leaders is very positive in sectors relying on consumer spending.

Wages are struggling to keep pace with the prices of the things we buy and average hours worked (per worker) have also been trending down or flat at best. This is not a picture of robust consumer finances.

On top of this retailers are facing the threat of competition from US giant Amazon. Yet according to our analysis of the outlook of leaders of Australia’s ASX 200 companies, positivity has increased.

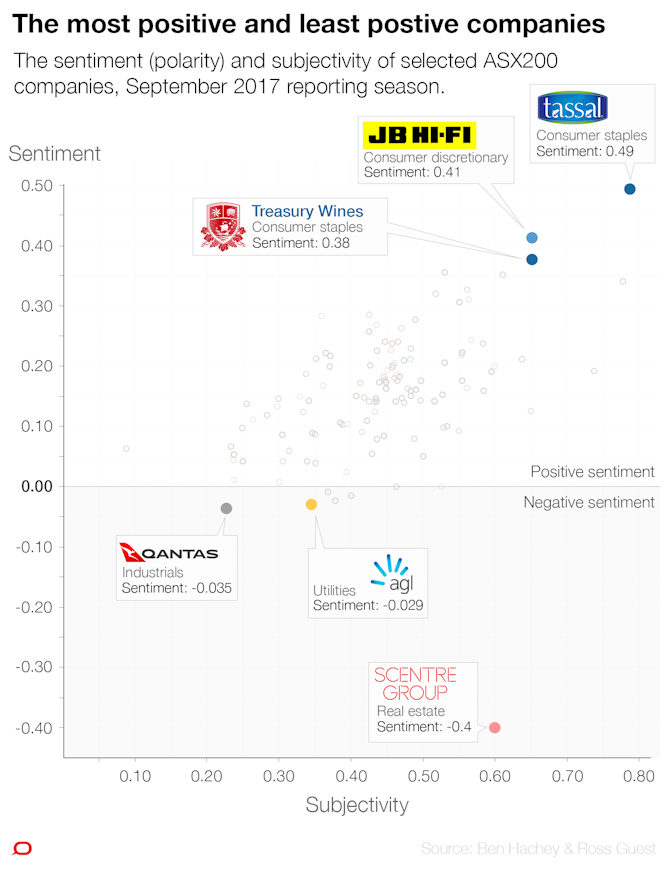

The sentiment of business leaders has remained positive and improved over the past 12 months according to our analysis. The “polarity” score, which measures whether the sentiment is positive or negative, has increased from 0.11 to 0.15 (a statistically significant improvement).

We also looked at how subjective these statements were and found there’s been no significant increase in how opinionated these statements are.

Our findings also mirror other business confidence surveys and even the Reserve Bank of Australia’s own outlook, which also paints a buoyant picture. The RBA expects growth in the economy to strengthen gradually to be around 3% in the first half of 2018. The RBA expects wage growth to gradually pick up over the next year or two and for average hours worked to increase somewhat.

Similarly, the Westpac-AusChamber Actual Composite index strengthened in June 2017, rising 1.8 points to 65.0. This factored in a strengthening in the labour market, as manufacturing firms plan to hire more workers and manufacturing wages rise. And the NAB business confidence survey also reveals that business conditions and confidence are improving.

The positive outlook for economic growth according to the RBA is driven by resource exports notably iron ore and liquid natural gas (LNG) production, household consumption including retail sales, and non-mining business investment. The RBA also expects wage growth to soon pick up.

These drivers are reflected in our sentiment analysis. Business leaders in ASX categories relying on household spending, have stronger than average positive outlook on the future, with an average score of 0.18.

This was led by businesses like JB HiFi (0.41), TabCorp (0.23) and Flight Centre (0.18); and also consumer staples led by Ardent Leisure (0.50), Treasury Wine Estates (0.38) and Coca-Cola Amatil (0.18).

The outlook for manufacturing is also positive due to a range of factors such as infrastructure spending by governments, stronger world growth, and improved international competitiveness due to a lower currency, commercial construction and home building, according to the Westpac-AusChamber index. This is supported by our analysis which found stronger than average sentiment from business leaders in the materials sector (0.17), through companies such as Amcor (0.26).

But the outlook isn’t all positive among our business leaders. Sentiment was weaker than average in utilities (0.07) led by AGL (-0.03). This is hardly surprising given the high uncertainty around energy policy – AGL for example owns coal-fired power plants. Also sentiment was somewhat weaker (0.13) than average among industrial company leaders, the sentiment in Qantas’ outlook was negative (-0.03) and property/real estate company Lend Lease (0.09) was also weak.

Perhaps the gloomy slow wage growth and underemployment will catch up to the more positive sentiment on consumer goods and services in company reports. Or this contradiction might simply reflect the high uncertainty in the global environment.

Consumers certainly seem a little confused: the weekly ANZ-Roy Morgan Consumer confidence Index ticked up slightly last week but has jumped around in recent months. Certainly the positive sentiment from business leaders consumer about consumer spending we see in company reports seems optimistic.

Authors: Ross Guest, Professor of Economics and National Senior Teaching Fellow, Griffith University; Ben Hachey, Honorary Associate, School of Information Technologies, University of Sydney.

AFG Chief Executive Officer David Bailey said this latest transaction is the largest term deal AFG has undertaken.

“The securitisation program is an important contributor to the company’s overall growth strategy. We are delighted to see the success of this issue further validate the AFG Securities business model.

”A very positive aspect of this transaction was the increase in the number of returning investors, as well as the increased number of new investors to our programme.

Mr Bailey said the success of the transaction reinforces the importance of the securitisation sector to the Australian lending market. “A vibrant and strong RMBS market is vital to ensure a greater level of competition and choice in the Australian mortgage market.

“By being able to source competitively priced funding from a variety of investors we can in turn provide competitively priced products to Australian consumers.

He noted the success of today’s issue reflects the confidence of investors in the high quality lending standards that AFG Securities apply. “The performance of our portfolio continues to be very strong and investors are recognising the unique position AFG holds in the residential mortgage market. These standards have underpinned the success of our latest transaction.

“As I have said before, the performance of every mortgage starts and ends with the credit policies and appetite of the lender. Our AFG Securities programme has robust underwriting and risk protocols and this is reflected in the performance of our book.

The transaction will settle on 7th September 2017.

Prior transactions include a $300m RMBS issuance in 2016, a $300 million issue in 2014 and a further two issues in 2013 of $245m and $300m.

The AFG 2017-1 Trust RMBS was successfully arranged by Australia and New Zealand Banking Group Limited (ANZ). Joint Lead Managers were National Australia Bank Limited and ANZ.

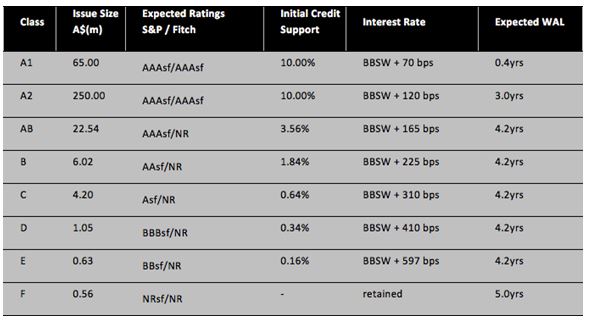

Detail relating to the A$350m AFG 2017-1 Trust RMBS transaction is as follows:

AFG is a diversified lending services company and one of the country’s largest mortgage broking groups. Through a network of 2,875 contracted mortgage brokers, AFG processes around $4.5 billion of finance every month and has a combined residential and commercial loan book of $133 billion.