APRA released their key metrics for ADI’s to June 2017. Net Profit across the sector, after tax was $34.2 billion for the year ending 30 June 2017. This is an increase of $6.5 billion (23.5 per cent) in 2016.

Provision were lower, with impaired facilities and past due items as a proportion of gross loans and advances at 0.88 per cent at 30 June 2017, a decrease from 0.94 per cent at 30 June 2016.

The return on equity was 12.0 per cent for the year ending 30 June 2017, compared to 10.3 per cent for the year ending 30 June 2016.

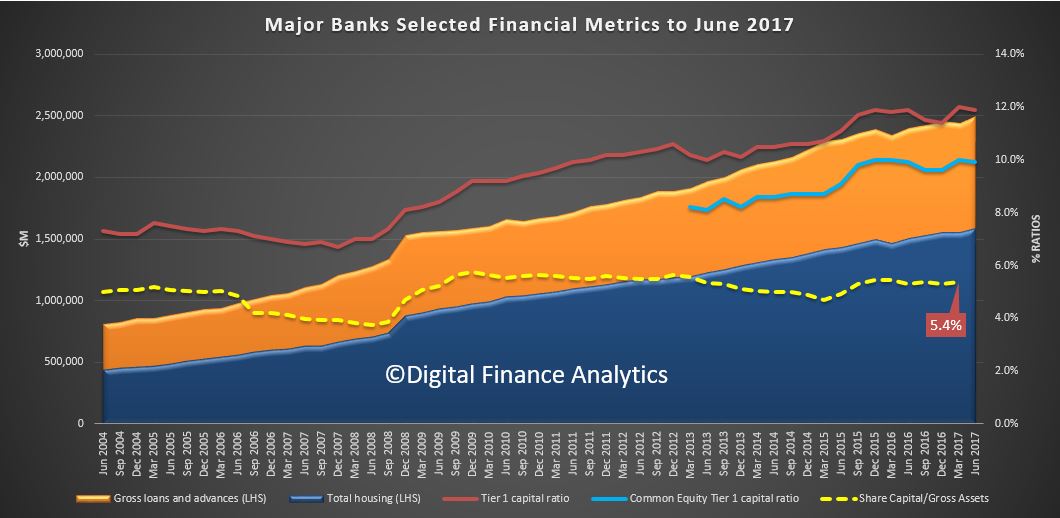

Looking at the four major banks, where the bulk of assets reside, we see that the ratio of share capital to assets is just 5.4%, this despite a rise in tier 1 capital and CET1. This is explained by the greater exposure to housing loans where capital ratios are still very generous, one reason why the banks love home lending. Thus the big four remain highly leveraged.

Looking more broadly at the APRA data:

Looking more broadly at the APRA data:

On a consolidated group basis, there were 148 ADIs operating in Australia as at 30 June 2017, 148 at 31 March 2017 and 156 at 30 June 2016.

- Bankstown City Credit Union Ltd had its authority to carry on banking business revoked, effective 16 June 2017.

- ECU Australia Ltd, had its authority to carry on banking business revoked, effective 4 May 2017.

- China Merchants Bank Co., Ltd, had its authority to carry on banking business authorised, effective 6 June 2017.

- Taishin International Bank Co., Ltd, had its authority to carry on banking business authorised, effective 23 May 2017

The net profit after tax for all ADIs was $34.2 billion for the year ending 30 June 2017. This is an increase of $6.5 billion (23.5 per cent) on the year ending 30 June 2016.

The cost-to-income ratio for all ADIs was 50.5 per cent for the year ending 30 June 2017, compared to 50.7 per cent for the year ending 30 June 2016.

The return on equity for all ADIs was 12.0 per cent for the year ending 30 June 2017, compared to 10.3 per cent for the year ending 30 June 2016.

The total assets for all ADIs was $4.64 trillion at 30 June 2017. This is a decrease of $4.6 billion (0.1 per cent) on 30 June 2016.

The total gross loans and advances for all ADIs was $3.12 trillion as at 30 June 2017. This is an increase of $141.5 billion (4.8 per cent) on 30 June 2016.

The total capital ratio for all ADIs was 14.2 per cent at 30 June 2017, an increase from 14.1 per cent on 30 June 2016.

The common equity tier 1 ratio for all ADIs was 10.2 per cent at 30 June 2017, unchanged from 10.2 per cent on 30 June 2016.

The risk-weighted assets (RWA) for all ADIs was $1.97 trillion at 30 June 2017, an increase of $123.0 billion (6.7 per cent) on 30 June 2016.

For all ADIs:

- Impaired facilities were $13.2 billion as at 30 June 2017. This is a decrease of $1.8 billion (11.9 per cent) on 30 June 2016. Past due items were $14.4 billion as at 30 June 2017. This is an increase of $1.3 billion (10.3 per cent) on 30 June 2016;

- Impaired facilities and past due items as a proportion of gross loans and advances was 0.88 per cent at 30 June 2017, a decrease from 0.94 per cent at 30 June 2016;

- Specific provisions were $6.6 billion at 30 June 2017. This is a decrease of $0.2 billion (3.6 per cent) on 30 June 2016; and

- Specific provisions as a proportion of gross loans and advances was 0.21 per cent at 30 June 2017, a decrease from 0.23 per cent at 30 June 2016.