We monitor Pay Day lending – or Small Amount Credit Contracts (SACC) – as they should be called, via our surveys. We have just run our 2017 updates, and we find that SACC lending is still growing, and well above inflation and wage growth. A symptom of financial stress in the community .

Watch the video, or read the post.

But SACC lenders are targeting different borrowers now, and mainly via online channels.

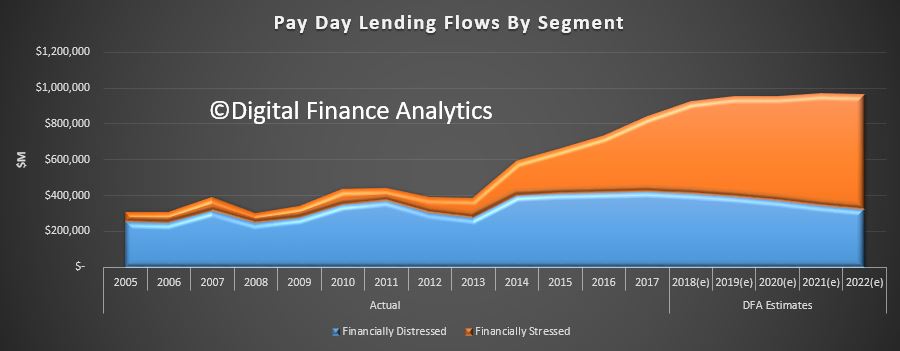

This first chart shows the relative lending flows split by distressed households and stressed households. Stressed households, we define as those with cash flow problems (often thanks to poor budgeting or over commitment) but many will have other financial assets, and even may own property. Most will be in employment. Lenders are targeting this group (especially using TV, radio and online channels) and there has been substantial growth.

Distressed households are those under financial pressure, often with limited employment, and are very likely to be on Government assistance. Recent tightening of the lending rules has reduced the share of lending to these distressed groups – which is a good thing.

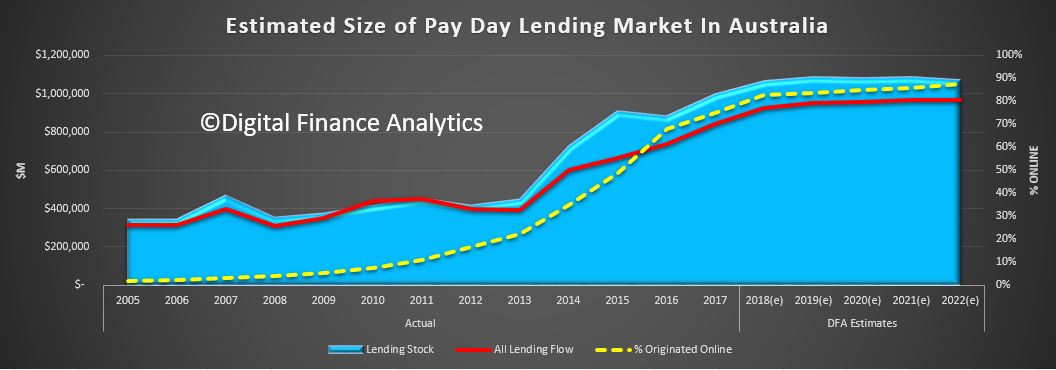

The overall net effect is the total lending from Pay Day providers, including the many online players – has risen to around $842m flow and $994m stock. Growth in 2015 -2016 was 10.7% and 2016-17 was 14.5%. We expect growth at least 10% in 2018, perhaps higher.

The overall net effect is the total lending from Pay Day providers, including the many online players – has risen to around $842m flow and $994m stock. Growth in 2015 -2016 was 10.7% and 2016-17 was 14.5%. We expect growth at least 10% in 2018, perhaps higher.

The share of loans originated online continues to rise, from 48% in 2015, to more than 75% now, and it will continue to rise further. These online services are easy to access, and borrowers, once they sign up can get “special” deals.

The share of loans originated online continues to rise, from 48% in 2015, to more than 75% now, and it will continue to rise further. These online services are easy to access, and borrowers, once they sign up can get “special” deals.

The online environment is of course hard to police, but the interest rates offered by many players are right at the top end of the allowable range.

The latest changes to the SACC legislation are still in the works. But we think there should be a further review looking at the online lending environment. This is clearly where the action (and risks) are. By plugging the lending to our most vulnerable households, the industry has regrouped around more affluent but needy connected households. There are more to target, and the prospect of substantial growth.

For an outline and critique of the proposed payday lending* reforms, see the following articles by Gill North (Professor of Law at Deakin University and Joint Principal of Digital Finance Analytics)

- ‘Small Amount Credit Contract Reforms in Australia: Household Survey Evidence & Analysis’ (2016) 27 Journal of Banking and Finance Law and Practice 203

- ‘Small Amount Credit Contract Reforms: Will the Affordability Cap Achieve Its Intended Objectives Without Unintended Adverse Consequences?’ (2017) 32 Australian Journal of Corporate Law 1

- ‘Small Amount Credit Contract Reforms: Have Transparency and Competition Concerns Been Forgotten?’ (2017) 25 Competition & Consumer Law Journal 101

Draft versions of these papers are available at https://ssrn.com/author=905894

Defined as “small amount credit contracts” in the National Consumer Credit Protection Act 2009 (Cth)