The customer owned banking sector today identified significant problems with banking competition in Australia and made three key recommendations to the Productivity Commission (PC) Inquiry to address the issue.

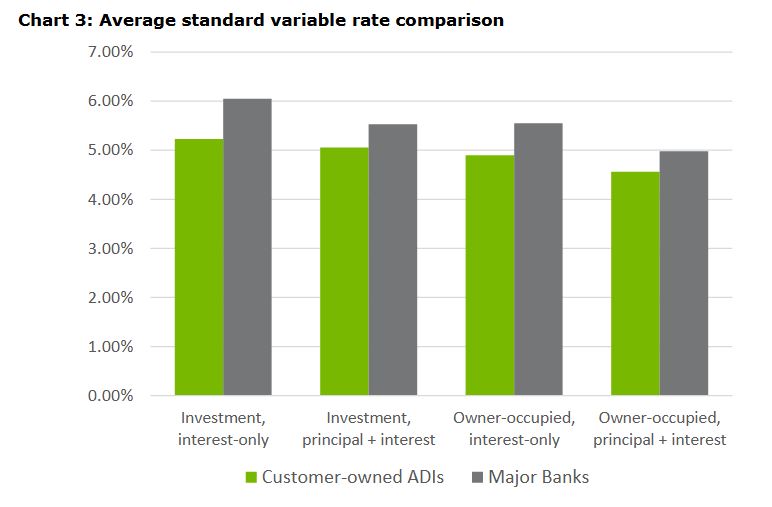

In their submission they highlighted the better rates on offer from Customer-owned banks, reflecting lower returns to stakeholders, but of benefit to customers. They also show better rates for depositors.

COBA’s Submission to the Productivity Commission Inquiry into Competition in the Australian Financial System recommends:

1. Policymakers and regulators give greater consideration to the impact on competition of the regulatory compliance burden and ensure that regulation is targeted, proportionate, risk-based and, where possible, graduated.

2. The Government introduce an explicit ‘secondary competition objective’ (SCO) into APRA’s legislative mandate, including with an accountability mechanism.

3. Interventions are needed to empower consumers to switch between banking products but interventions to promote switching should be cost-effective and based on rigorous market studies of banking product markets and consumer behaviour.

COBA’s Director – Policy, Luke Lawler, said:

“The enduring solution to concerns about the banking market is action to promote sustainable competition.

“We don’t have sustainable banking competition at the moment. A lack of competition can contribute to inappropriate conduct by firms, and insufficient choice, limited access and poor quality products for consumers.

“The regulatory framework over time has entrenched the dominant position of the largest banks.

“Promoting a more competitive banking market does not require any dilution of financial safety or financial system stability.

“A ‘secondary competition objective’ (SCO) for APRA would raise the relative ‘priority’ of competition compared to APRA’s ‘other considerations’. It would remain secondary to APRA’s primary responsibilities of financial stability and safety. The SCO would include reporting obligations to ensure accountability against the objective.

“The SCO would formalise the relative ‘prioritisation’ of competition and ensure that it becomes ingrained into APRA’s day-to-day regulatory processes.

“APRA’s peer regulator in the UK, the PRA, was given an SCO in 2014 and the outcome is a ‘material change of gear’ where ‘competition is gaining airtime and traction at all levels’ and ‘there are numerous instances where competition considerations have influenced policy outcomes.’

“We do not doubt that APRA already gives some consideration to competition but we judge this to be inadequate and inconsistent.

“Examples of APRA’s failure to give due consideration to competition concerns include: lack of urgency in addressing the market distortions caused by the unfair funding cost advantage enjoyed by the major banks due to the implicit guarantee continuing wide gap in mortgage risk weight settings between the major banks and smaller banking institutions, and implementation of macro-prudential measures affecting investor lending that rewarded major banks which had expanded their investor lending portfolios most aggressively before the cap was applied.

“Customer owned banking institutions offer the full range of consumer retail banking products and services, including highly competitive home loans, credit cards, personal loans and deposit products. Many of these products are market leading and award winning.

“As the providers of these products, customer owned banking institutions strongly support cost-effective measures to empower consumers to switch.

“COBA recommends rigorous market studies of retail banking product markets, taking into account consumer behaviour and behavioural biases, to identify the barriers to switching and to design interventions to reduce these barriers in the most cost-effective way.

“We welcome the Government’s decision to provide resources to the ACCC to establish a dedicated Financial Services Unit to undertake regular in-depth inquiries into competition issues in the financial system. We also support the Government’s decision to include competition in ASIC’s mandate. We recommend clarity of responsibility between these two regulators for carrying out market studies and designing interventions to promote switching.”