The question of how much capital should a bank hold is running hot these days. To illustrate the point, lets look at the commentary surrounding the the semi-annual update of the Global Capital Index, which show the capital ratios for Global Systemically Important Banks, and which was released in early April by FDIC Vice Chairman Hoenig. The Federal Deposit Insurance Corporation (FDIC) preserves and promotes public confidence in the U.S. financial system by insuring depositors for at least $250,000 per insured bank; by identifying, monitoring and addressing risks to the deposit insurance funds; and by limiting the effect on the economy and the financial system when a bank or thrift institution fails. So what they say in significant.

Among the data in the report:

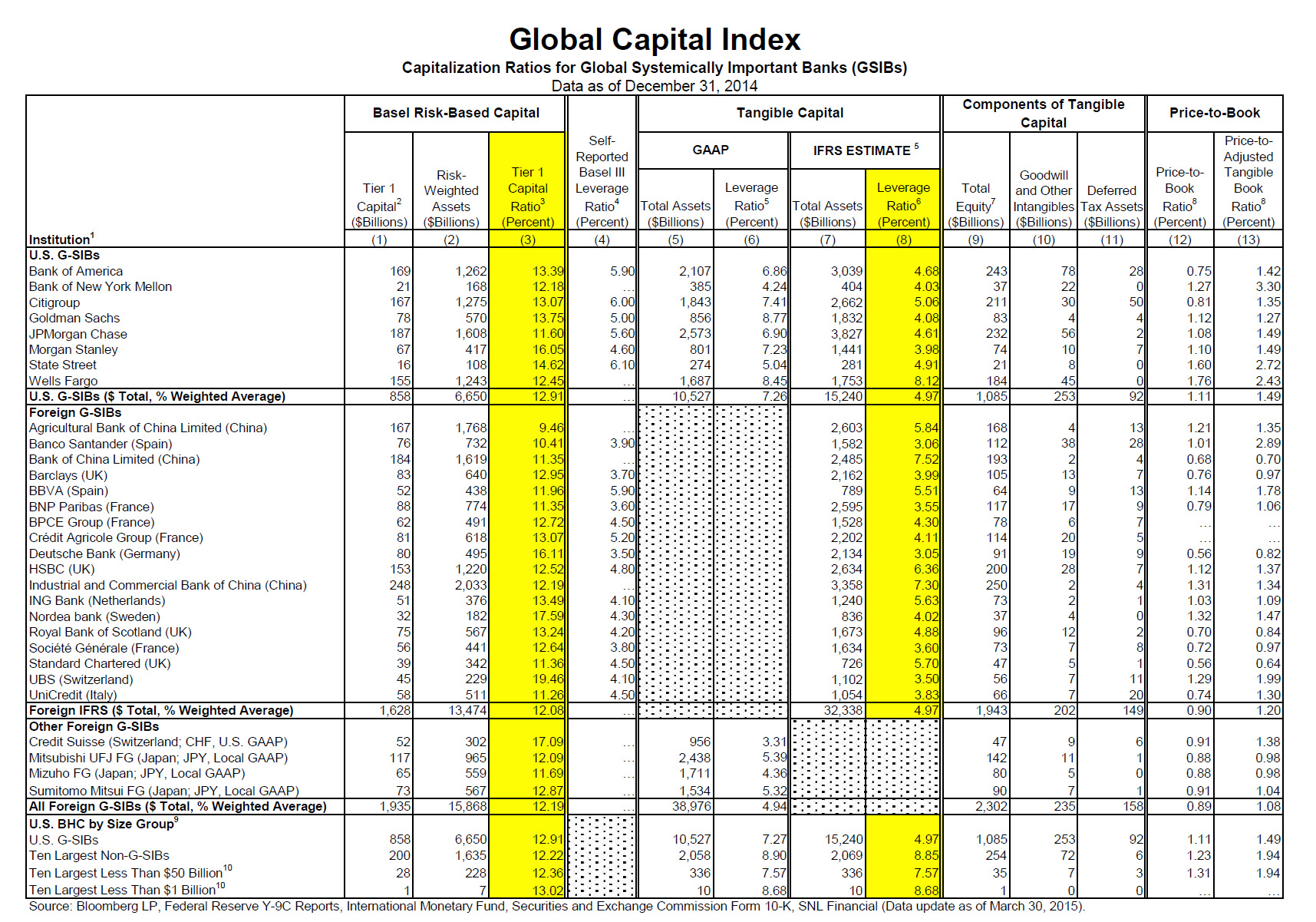

- For the largest U.S. banking firms, the average tangible equity capital ratio – known inversely as the leverage ratio – is 4.97 percent. In other words, each dollar of assets is funded with 95 cents of borrowed money.

- The largest regional and community banks, have tangible capital ratios ranging from 7.57 to 8.85 percent. That is, they operate with between 1.5 and 1.7 times more funding from their ownership than G-SIBs do.

“The Global Capital Index illustrates how financial resiliency is still sorely lacking,” Vice Chairman Hoenig said. “The sector of the financial industry with the greatest concentration of assets is the least well capitalized. Plainly put, it operates with the largest amount of borrowed, or as we say, leveraged funding, and thus it is the least well prepared to absorb loss. Yet the primary measure of capital – the risk weighted measure — makes the largest firms appear relatively more stable than they really are. The reality is that with too little owner equity funding individual firms, the industry as a whole also is undercapitalized and should one firm fail, the industry continues to be vulnerable to contagion and systemic crisis. It follows that the lack of adequate tangible capital remains among the greatest impediments to successful bankruptcy and resolution.”

The Global Capital Index uses estimates of International Financial Reporting Standards (IFRS) to measure a firm’s tangible equity (loss-absorbing capital) against on- and off-balance sheet assets, as shown in column 8 of the table. The tangible capital measurement includes derivatives and other assets that are off-balance-sheet in US Generally Accepted Accounting Principles (GAAP) and Basel calculations. It is calculated by comparing equity capital to total assets, deducting goodwill, other intangibles, and deferred tax assets from both equity and total assets.

The tangible leverage ratio measures funds available to absorb loss against total balance sheet and some off-balance sheet assets. It does not attempt to predict or assign relative risk weights among asset classes. “It is more difficult to game, and it provides the most clear and complete picture of a banking firm’s ability to absorb loss regardless of source,” Vice Chairman Hoenig said.

In contrast, the ratios of Tier I capital to risk-weighted assets for all banks, largest to smallest, are above 10 percent and some of the largest have ratios of more than 15 percent. “This higher capital ratio is achieved by reducing on-balance sheet assets by a pre-assigned risk weight and excluding off-balance sheet assets, such as derivatives. This measure is misleading and overstates the strength of these firms’ balance sheets. No other industry is allowed to make these kinds of adjustments,” Vice Chairman Hoenig said. “The tangible leverage ratio provides a more accurate measure of assets and risks than the balance sheet reported under either GAAP or Basel.”