Underestimating the appetite of premium quality borrowers has led to a revenue downgrade for fintech business lender Prospa and a 28 per cent reduction in its share price. Via InvestorDaily.

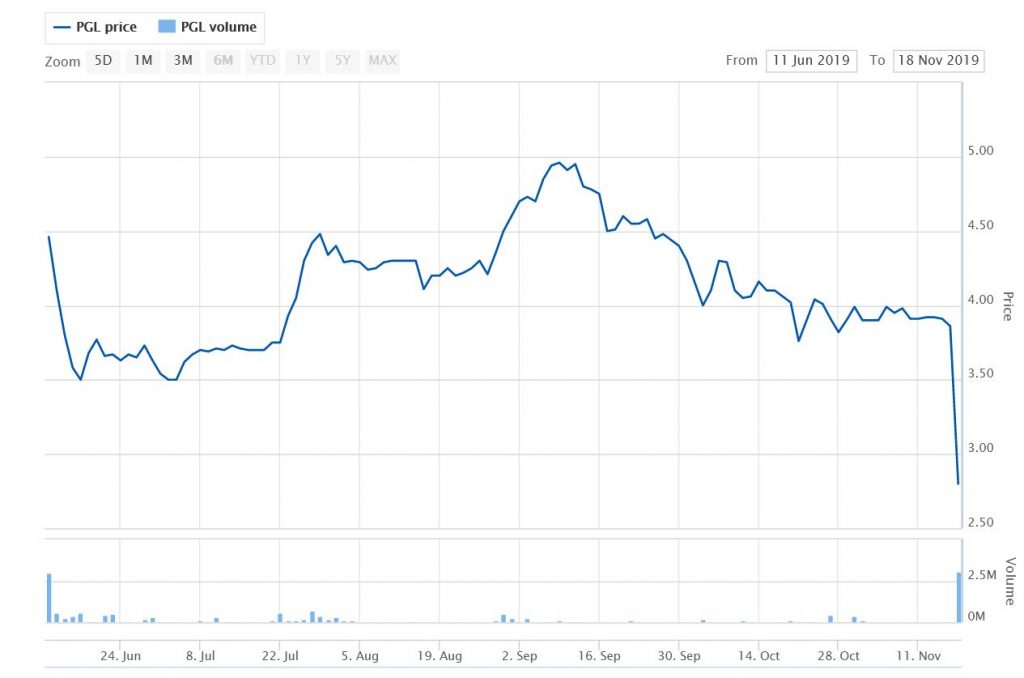

Prospa shares crashed 27 per cent to a record low of $2.80 on Monday morning following the release of the group’s trading and guidance update.

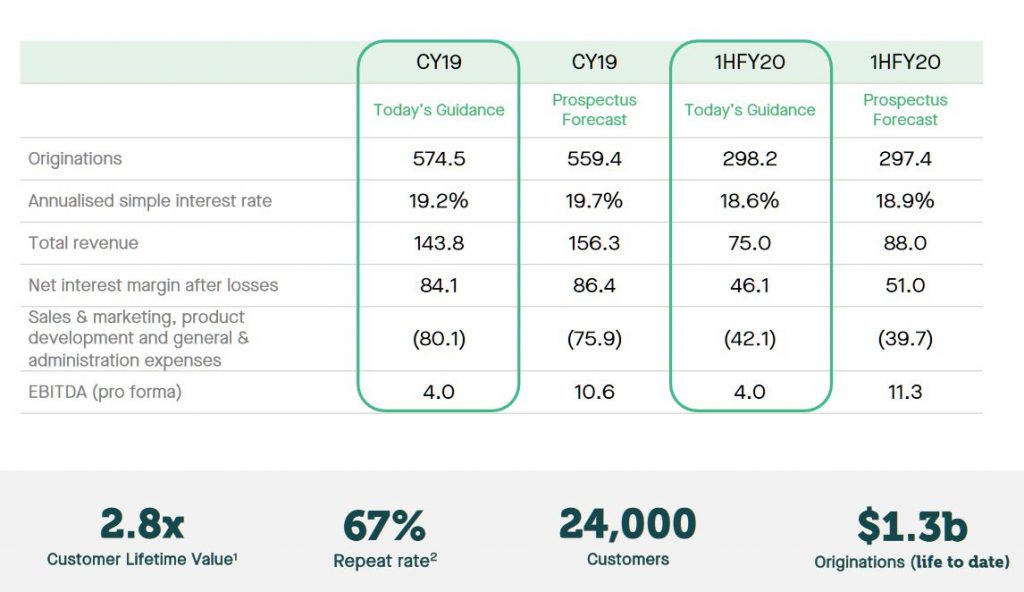

Prospa has revised its revenue forecasts down by 8 per cent to $143.8 million from the $156.4 million as advertised in the company’s prospectus. Prospa floated on the ASX in June with an IPO price of $3.78 and rallied almost 20 per cent in day of trading, lifting the company’s market cap to $720 million.

However, following this week’s trading update, the company is now valued at $450 million. Sales and marketing expenses are forecasted to be $80.1 million for the calendar year, up 5.5 per cent from the $75.9 million forecast in the prospectus.

EBITDA is forecast to take a 62 per cent hit from $10.6 million to $4 million.

Prospa stated that the downward revision to its revenue predictions is largely due to its “premiumisation strategy exceeding our forecast”. Premiumisation is traditionally a strategy employed by companies to make consumers pay more for a product by promoting its exclusivity. But for a small business lender like Prospa, premium customers are actually less profitable.

“While we continue to grow our lending to all credit grades, we are seeing increased appetite for our solutions from premium credit quality customers who pay lower interest rates over longer terms,” the company said.

Prospa said its strategy to optimise its cost of funding has facilitated lower rates for customers and broadened its customer base and appeal – allowing the company to tap more of the $20 billion addressable market.

“The introduction of a new rate card in early April was more successful than anticipated, with approximately 43 per cent of Prospa’s portfolio now represented by premium customers,” the company said.

“The evolution in book composition towards premium grades has led to a short-term impact on revenue, despite the positive impact premiumisation has had on market penetration, operating leverage, funding diversity and portfolio resilience.”

Lending rates to premium customers are lower than the average book rate and the loan duration is longer. In the four months to 31 October 2019, the average simple interest rate on Prospa’s book has adjusted to 18.5 per cent compared to the prospectus forecast at 18.9 per cent and average loan term has increased to 14.6 months (Prospectus at 14 months).

Early indications are that the static loss rates in the growing premium section of our loan book are well below 4 per cent, which is the bottom of the risk appetite range.

Greg Moshal, co-founder and joint CEO of Prospa, admitted that the lender is experiencing some short-term impacts on its forecasts, but said he remains confident Prospa has the right growth strategies to deliver long-term shareholder value and solve the funding challenges of small business owners across Australia and New Zealand.

“Originations are growing,” he said. “Portfolio premiumisation means a higher quality loan book and lower rates and longer average terms for our customers. Early loss indicators continue to improve and we expect to continue to invest in new products, sales and marketing.”