SMSF and accounting professionals alike are increasingly finding that clients are willing to take risky moves with their property portfolios, in an effort to reduce their mortgage stress. From SMSF Adviser.

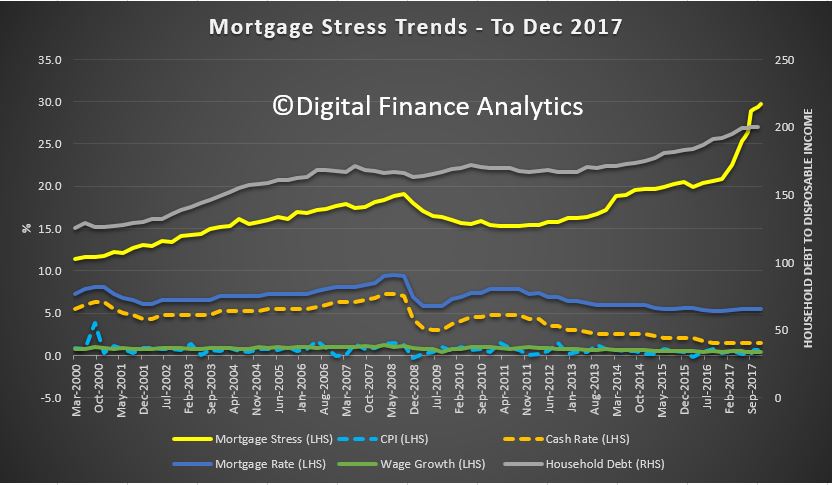

These patterns are surfacing as instances of mortgage stress continue to climb significantly in Australian households. Research house Digital Finance Analytics (DFA) has released its mortgage stress and default analysis for December 2017, showing about 29.7 per cent of households — 921,000 — are under “mortgage stress.”

About 24,000 households are under “severe mortgage stress”, up by 3,000 from November 2017.

DFA principal Martin North believes the risk of default for Australians has increased for 2018, with an estimated 54,000 households currently at risk of 30-day debt defaults in the next 12 months.

Several accountants and financial advisers have told Accountants Daily that their clients, including high-net-worth property investors, are increasingly looking to take on more risk to sustain their levels of debt.

Director at Verante Financial Planning, and chair of the SMSF Association’s NSW state chapter, Liam Shorte, said he’s seen evidence of investors asking accountants to increase their reportable income to increase their borrowing capacity, usually where they need to refinance. Historically, clients have sought advice on how to minimise their reportable income for tax purposes.

He also told sister publication Accountants Daily that more clients are asking their parents to do a “family pledge,” or guarantee about 20 per cent of a loan to help reduce debt while refinancing.

For Lielette Calleja, director at bookkeeping firm All That Counts, mortgage stress is most pronounced with small business owners, and doesn’t necessarily only affect those at the lower end of the earning scale.

“I would have to say that small business owners are heavily affected. Your income is not always consistent, as opposed to being a PAYG. Mortgage stress is across the board I don’t believe it discriminates as it’s relative to each type of borrower. Property investors and high-net-worth individuals tend to be asset rich but lack cash flow until their development is complete and/or sold/leased out,” Ms Calleja told Accountants Daily.

Further, Ms Calleja is finding clients are modifying their behaviours and expenses to adjust to a new normal in household debt levels.

“Families that are not in a position to refinance are resorting to taking their kids out of private schools and foregoing luxury holidays, even simple things like making your own lunch instead of buying is becoming the Aussie way,” she said.

“Small business owners are coming to the conclusion that having good financials consistently all year round is critical in keeping their mortgage stress levels at bay,” she added.