The latest edition of the Digital Finance Analytics Household Finance Security Index, to end April, released today, shows a lift from 88.14 to 89.20. This is still below the long term neutral score of 100, but is the highest score so far this year.

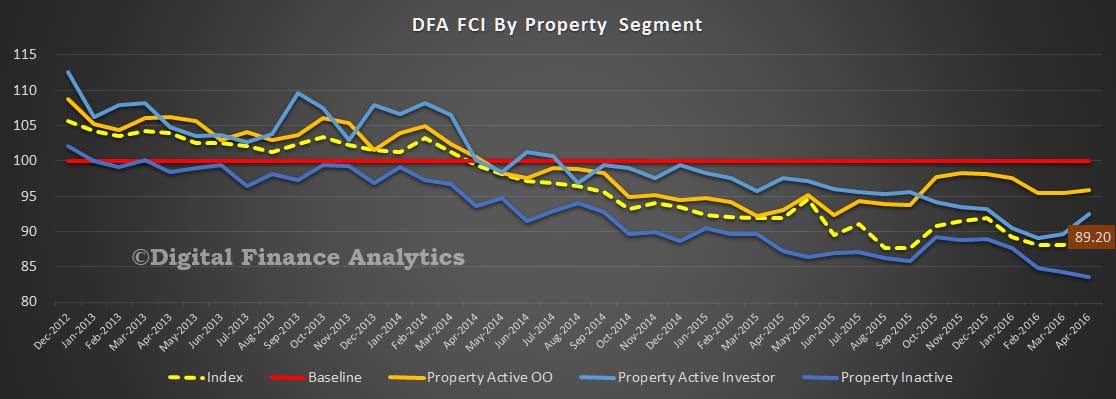

Of note is the significant spike from 89.67 to 92.45 in confidence among property investors, thanks to the Government stance on negative gearing, the expectation of interest rate cuts, and better news on home price growth. Investor households in NSW and VIC improved the most. Property active owner occupied households saw a small lift from 95.43 to 95.93, thanks to the expectation of lower mortgage rates (though offset by lower returns from those with deposits). Improved stock marker performance assisted. Once again, stronger positive scores in NSW and VIC were somewhat offset by noticeably weaker scores in WA and QLD.

Of note is the significant spike from 89.67 to 92.45 in confidence among property investors, thanks to the Government stance on negative gearing, the expectation of interest rate cuts, and better news on home price growth. Investor households in NSW and VIC improved the most. Property active owner occupied households saw a small lift from 95.43 to 95.93, thanks to the expectation of lower mortgage rates (though offset by lower returns from those with deposits). Improved stock marker performance assisted. Once again, stronger positive scores in NSW and VIC were somewhat offset by noticeably weaker scores in WA and QLD.

Overall costs of living were flat. We saw a further fall in those who had received a pay rise whilst those with property on average saw their net worth rise again.

There was a noticeable fall in those households who are not property active – either renting or living with family or friends. On average their score fell again, from 84.3 to 83.5. These households are more exposed to costs of living (including rising rentals), have no leverage to the rising property market and are more stressed financially than property holding segments. Around one third of households fall into this group.

By way of background, these results are derived from our household surveys, averaged across Australia. We have 26,000 households in our sample at any one time. We include detailed questions covering various aspects of a household’s financial footprint. The index measures how households are feeling about their financial health. To calculate the index we ask questions which cover a number of different dimensions. We start by asking households how confident they are feeling about their job security, whether their real income has risen or fallen in the past year, their view on their costs of living over the same period, whether they have increased their loans and other outstanding debts including credit cards and whether they are saving more than last year. Finally we ask about their overall change in net worth over the past 12 months – by net worth we mean net assets less outstanding debts.

One thought on “Property Investor Confidence Lifts”