Today we continue to feature research published in the latest edition of The Property Imperative, The full report is available on request. We look across the property investment sector, which remains strong despite lower growth in investment lending. We continue to see that tax benefits and the prospects of better gains than deposit accounts or shares drives the market. This despite the fact that some investors have a negative net yield, thanks to low rental growth.

Solo Investors.

About 992,000 households only hold investment property, 2.5% of which are held within superannuation. Households in this segment will often own one or two properties, but do not consider they are building an investment portfolio.

Around 68% of households expect prices to rise in the next 12 months, 38% of households expect to transact within the next year, 53% will need to borrow more, and 37% will consider the use of a mortgage broker.

Around 68% of households expect prices to rise in the next 12 months, 38% of households expect to transact within the next year, 53% will need to borrow more, and 37% will consider the use of a mortgage broker.

There are a number of barriers to investment, which our surveys identified. Many investors had already bought, so were not in the market (34%). More than 26% of potential investors were concerned by possibly adverse change to regulation – negative gearing or capital gains and 9% specifically referred to risks in the May budget. Some (12%) said they felt property prices were now too high.

There are a number of barriers to investment, which our surveys identified. Many investors had already bought, so were not in the market (34%). More than 26% of potential investors were concerned by possibly adverse change to regulation – negative gearing or capital gains and 9% specifically referred to risks in the May budget. Some (12%) said they felt property prices were now too high.

Portfolio Investors

Households who are portfolio investors maintain a basket of investment properties. There are 191,000 households in this group. The median number of properties held by these households is eight. Most households expect that house prices will rise in the next 12 months (70%), and 64% said they will transact in the next 12 months. Many will borrow more to facilitate the transaction (90%), and 52% will use a mortgage broker. Significantly we now see about 23% of portfolio investors looking to their property investments as the main source of income, it has in effect become their full time job. A significant characteristic is the cross leverage from one property to the next.

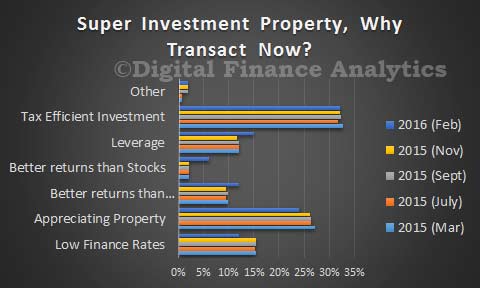

Super Investment Property

Throughout the survey we noted an interest in investing in residential property via a self-managed superannuation funds (SMSFs). It is feasible to invest if the property meets certain specific criteria.

Overall our survey showed that around 3.75% of households were holding residential property in SMSF, and a further 3.5% were actively considering it.

Of these, 33% were motivated by the tax efficient nature of the investment, others were attracted by the prospect of appreciating prices (24%), the attractive finance offers available (12%), the potential for leverage (15%) and the prospect of better returns than from bank deposits (12%).

Of these, 33% were motivated by the tax efficient nature of the investment, others were attracted by the prospect of appreciating prices (24%), the attractive finance offers available (12%), the potential for leverage (15%) and the prospect of better returns than from bank deposits (12%).

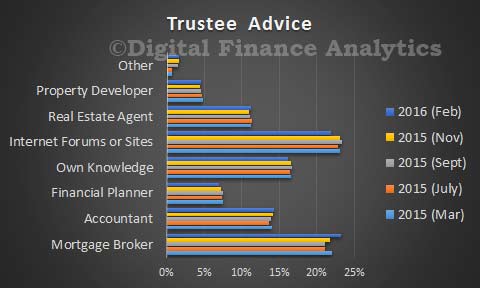

We explored where SMSF Trustees sourced advice to invest in property, 23% used a mortgage broker, 22% online information, 11% a Real Estate Agent, 14% Accountant, and 7% a Financial Planner. Financial Planners are significantly out of favour in the light of recent bank disclosures publicity on poor advice.

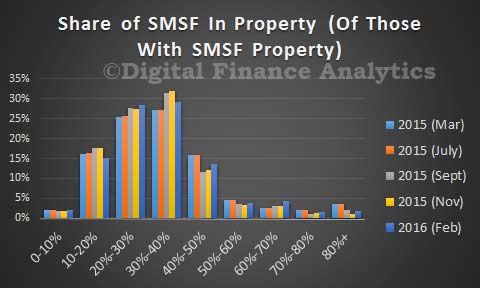

The proportion of SMSF in property was on average 34%.

The proportion of SMSF in property was on average 34%.

According to the fund level performance from APRA to December 2015, and DFA’s own research, Superannuation has become big business, with total assets now worth over $2 trillion (compare this with the $5.5 trillion in residential property in Australia), an increase of 6.1 % from last year.

According to the fund level performance from APRA to December 2015, and DFA’s own research, Superannuation has become big business, with total assets now worth over $2 trillion (compare this with the $5.5 trillion in residential property in Australia), an increase of 6.1 % from last year.

APRA reports that Self-Managed Superannuation funds held assets were $594.6 billion at December 2015, a rise from $578.9 billion in Sept 2015.