Last Friday, the UK’s Prudential Regulation Authority (PRA) proposed a more flexible approach to determining Pillar 2A capital requirements for banks calculating risk-weighted assets (RWAs) according to the standardised approach. The PRA’s proposal aims to use Pillar 2A to reduce some of the variation between standardised risk weights and internal models outputs for similar risks, remove future duplication between IFRS 9 provisions for expected loss and the standardised approach, create incentives for smaller lenders to move away from higher risk mortgage lending and facilitate greater competition among UK banks.

We expect that the proposed changes will reduce the capital requirements for small banks and building societies, freeing up capital for further growth. However, in an already competitive market, with many smaller firms growing faster than the market, increased competition will negatively pressure margins and reduce profitability for all banks, a credit negative.

The proposal more closely aligns the RWAs calculated with the standardised approach and the internal ratings-based approach by allowing lenders the PRA deems adequately governed and well managed to benefit from lower Pillar 2A capital requirements if their loan portfolio is considered low risk. Disincentives would be created for higher-risk lending for which standardised risk weights are often equal to or lower than the upper band of the PRA’s internal ratings-based benchmarks. The PRA’s proposal follows the Competition Market Authority’s report recommending greater competition in the UK retail banking.

The proposal also seeks to address the potential for an effective double counting of expected loss that these firms may incur with the adoption of IFRS 9 on 1 January 2018, which would not have applied to lenders using the internal ratings-based approach.

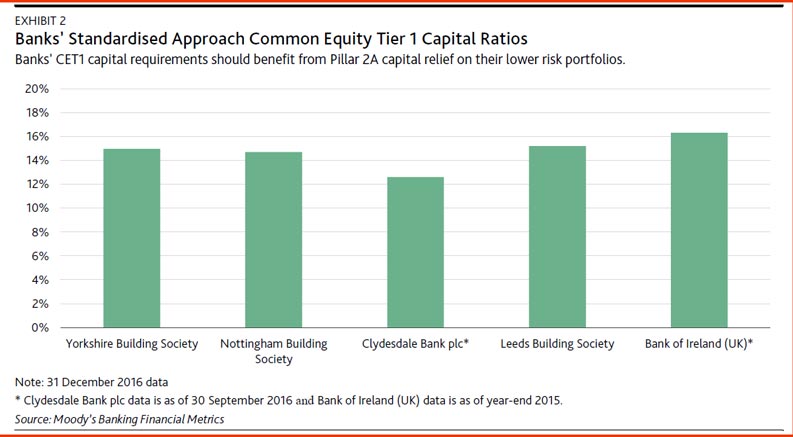

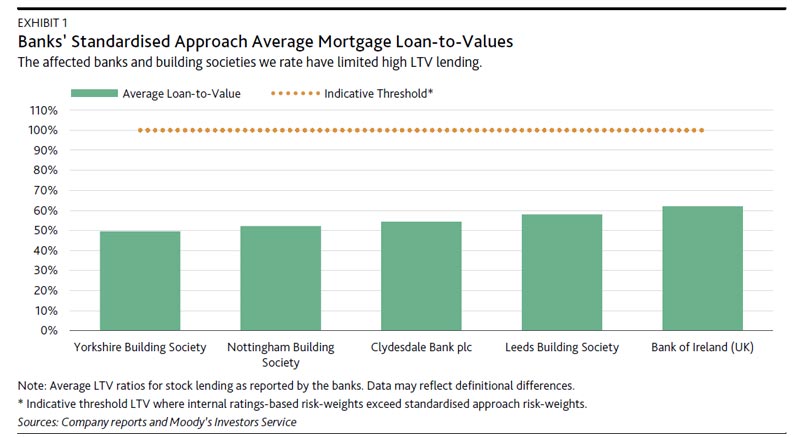

We expect that the UK banks and building societies that we rate and which use the standardised approach will largely receive reduced Pillar 2A requirements under this proposal because of their focus on residential mortgages with limited high loan-to-value (LTV) exposures. These banks’ low-LTV and residential mortgage focus, as shown in Exhibit 1, means that they are likely to benefit from capital relief without significant incentives to change lending practices. However, all of these institutions have achieved material growth in their mortgage books over the past few years, targeting increases in volume to offset increasing margin pressure. We view negatively further incentives to foster growth for these firms through a relaxation of Pillar 2A capital requirements because doing so will weaken the affected banks’ stress capital resilience. Exhibit 2 shows banks’ reported common equity Tier1 capital ratios. We note that most of the affected banks we rate are already expanding their lending faster than the market, with annual growth of around 10% (excluding Yorkshire Building Society) in 2016, compared with 4% market growth.

We expect the PRA’s proposal to contribute to already-strong competition in the UK mortgage market, adding negative pressure to net interest margins, and negatively affecting the profitability of the banks we rate.

Affected firms are also likely to benefit from a lower minimum requirement for own funds and eligible liabilities (MREL) as a result of these proposals because of a reduction in the combined Pillar 1 and Pillar 2A capital requirements, reducing the loss-absorption capacity for creditors in the event of their failure. A subset of these firms, which have total assets in excess of £15-£25 billion, are likely to see the greatest MREL relief because they are subject to the strictest form of the requirements.