A new report from the Financial Stability Board overviews the development of FinTech platforms and looks at potential risks such activity brings. The report highlights that the growth is strong in certain markets, but the business models and partnering models vary widely. In volume terms China, US and UK lead the way.

There is diversity in Fintech target borrowers. In some markets, they are primarily consumers, in others, small business. Loans can be unsecured, or secured. A growing trend is the partnering with incumbent banks.

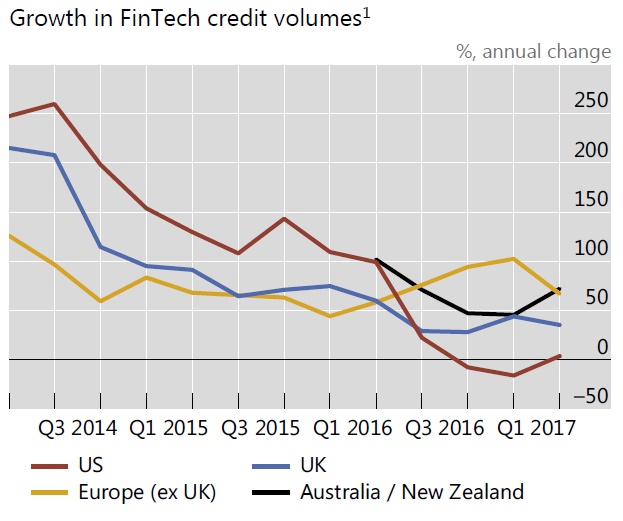

Although FinTech credit markets are currently small in size relative to traditional credit markets, they are growing at a fast pace. In some markets, the share of lending is sufficient to impact financial stability, and as growth continues, more measures may be required.

“A bigger share of FinTech credit in the financial system could have both financial stability benefits and risks,” says CGFS chairman William C Dudley (President, Federal Reserve Bank of New York).

“A bigger share of FinTech credit in the financial system could have both financial stability benefits and risks,” says CGFS chairman William C Dudley (President, Federal Reserve Bank of New York).

Potential benefits include increased access to alternative funding sources in the economy and efficiency pressures on incumbent banks. At the same time, risks may arise, including weaker lending standards and more procyclical credit provision.

“The emergence of FinTech credit markets poses challenges for policymakers in terms of how they monitor and regulate such activity. Having good-quality data will be key as these markets develop,” said chairman of the FSB Standing Committee on Assessment of Vulnerabilities Klaas Knot (President, De Nederlandsche Bank).

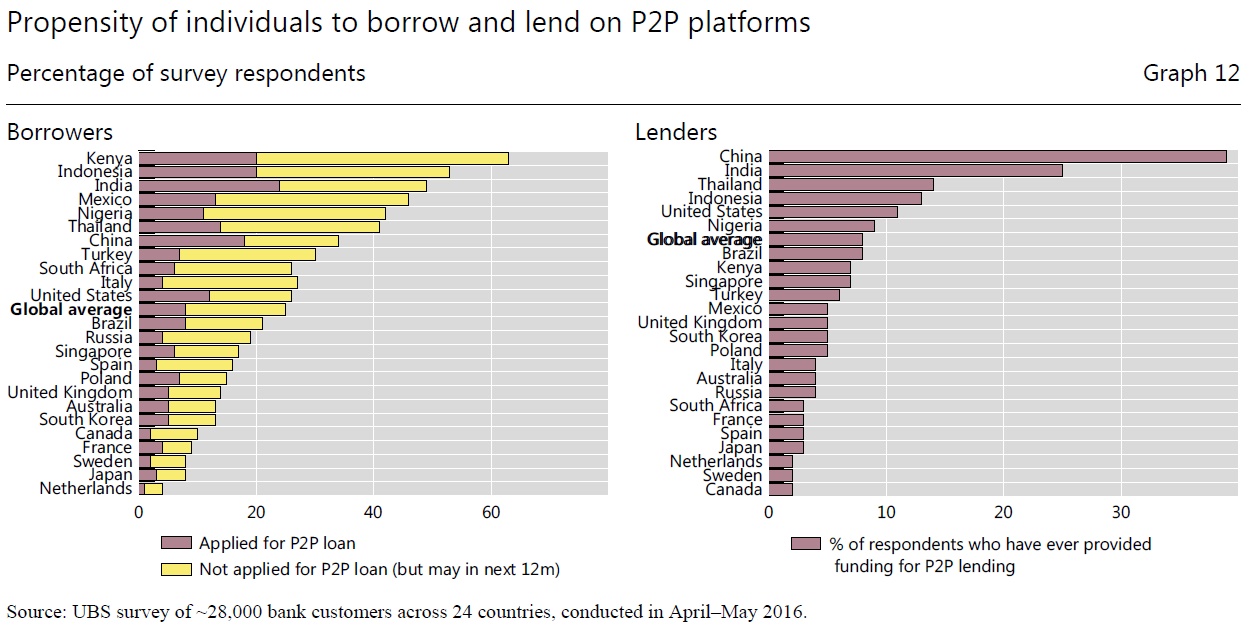

Size and structure of FinTech credit markets

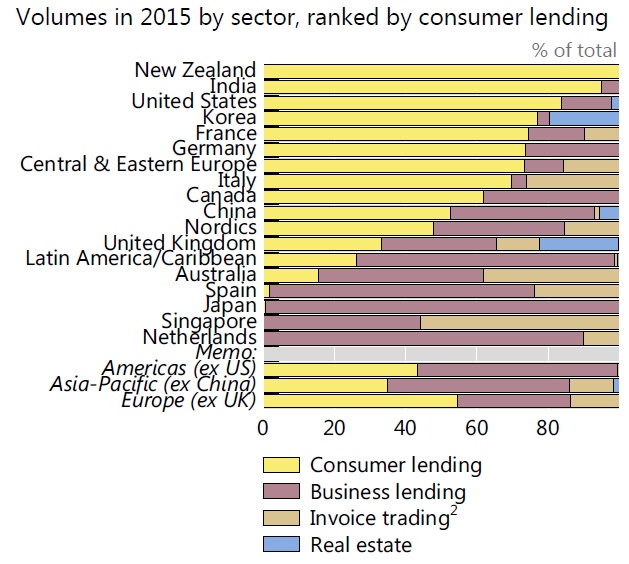

Academic survey data on lending volumes in 2015 show considerable dispersion in FinTech credit market size across jurisdictions. In absolute terms, the largest FinTech credit market is China (USD 99.7 billion in 2015), followed at a distance by the United States (USD 34.3 billion) and the United Kingdom (USD 4.1 billion). In each of these three markets, new FinTech credit volumes were USD 60–110 per capita in 2015. Lending volumes were very small in other countries. It is noteworthy that the survey data for China are judged to have a lower platform coverage than other large markets; activity in China may therefore be underrepresented in a relative sense.

The composition of FinTech credit activity by borrower sector has varied noticeably across jurisdictions. In the United States, more than 80% of lending activity in 2015 was to the consumer sector (including student loans), while high shares of consumer lending were also evident in several other countries, such as Germany, Korea and New Zealand. In contrast, in Australia, Japan and the Netherlands, FinTech credit was almost entirely directed to the business sector as measured to include invoice trading (a non-loan typeof business credit). FinTech credit in the United Kingdom was also mostly extended to the business sector, with a significant portion of this in the form of secured real estate lending.

The FinTech credit market structure also varies across those jurisdictions for which data are available. The Chinese market has by far the highest number of FinTech lending platforms. In the United Kingdom, there are 21 platforms that have full regulatory authorisation, but a further 66 are being assessed for authorisation, of which 32 have interim permission to undertake activity. France also has a relatively high number of platforms, with a significant number of entrants after FinTech-specific legislation was introduced in 2014. In most jurisdictions, FinTech credit market activity appears to be reasonably concentrated among the five largest platforms, with the most notable exception being the Chinese market.

The FinTech credit market structure also varies across those jurisdictions for which data are available. The Chinese market has by far the highest number of FinTech lending platforms. In the United Kingdom, there are 21 platforms that have full regulatory authorisation, but a further 66 are being assessed for authorisation, of which 32 have interim permission to undertake activity. France also has a relatively high number of platforms, with a significant number of entrants after FinTech-specific legislation was introduced in 2014. In most jurisdictions, FinTech credit market activity appears to be reasonably concentrated among the five largest platforms, with the most notable exception being the Chinese market.

FinTech credit can be primarily segmented into private consumer loans and business loans. Debt refinancing or debt consolidation appears to be the most common purpose of FinTech consumer loans (including for student loans in the United States). To a lesser extent, consumer

loans are also taken out for vehicle purchase or home improvement in Australia, France and Italy. The US P2P consumer loan market is split between unsecured consumer lending and student lending. Platforms target prime and near-prime customers for the former, and higher quality

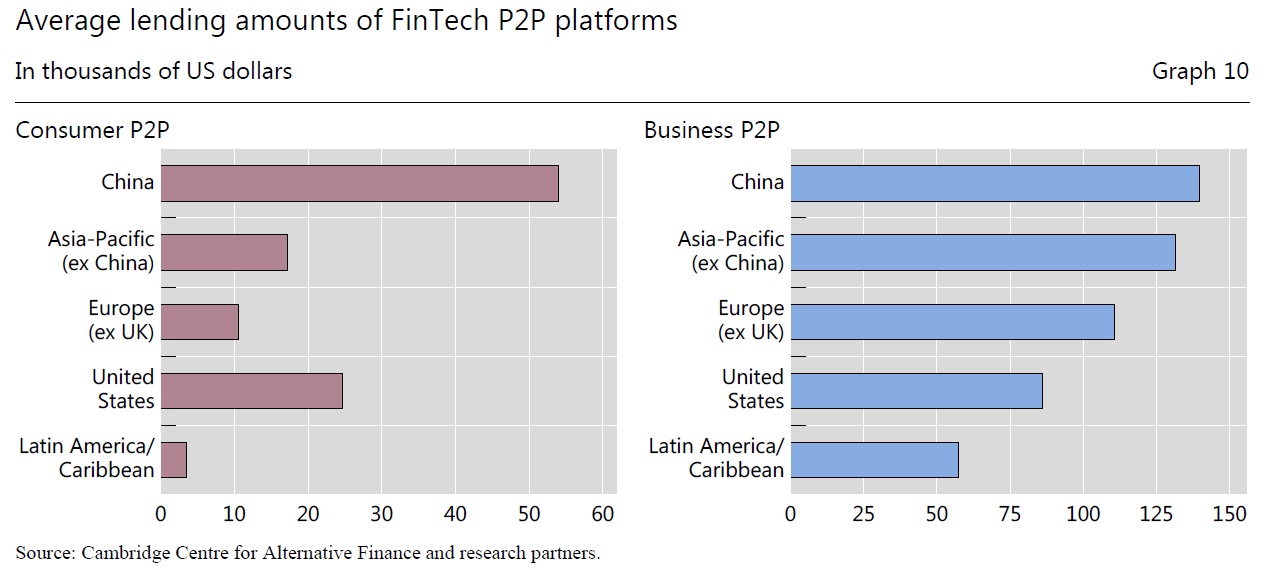

borrowers with limited credit history for student lending. The available data suggest that, in most jurisdictions, average FinTech consumer loans are typically in the range of USD 5,000–25,000, with the United States at the top end of that range (Graph 10). Average borrowing amounts are much larger in China, at more than USD 50,000.

Business loans in the United States are typically for small and medium-sized enterprises (SMEs). Platforms offer both secured and unsecured loans. The small business lending segment comprises nearly one quarter of overall FinTech lending, and the borrowers are more heterogeneous than consumer loan borrowers. In the United Kingdom, the majority of P2P business lending appears to be extended to small businesses. AltFi data suggest that around two thirds of P2P business lending is on a secured basis, mostly real estate but also non-property collateral.

Business loans in the United States are typically for small and medium-sized enterprises (SMEs). Platforms offer both secured and unsecured loans. The small business lending segment comprises nearly one quarter of overall FinTech lending, and the borrowers are more heterogeneous than consumer loan borrowers. In the United Kingdom, the majority of P2P business lending appears to be extended to small businesses. AltFi data suggest that around two thirds of P2P business lending is on a secured basis, mostly real estate but also non-property collateral.

Platforms in the Americas and Europe appear to be more domestically focused in their lending than in their capital or fund-raising activities, with only around 10–12% of platforms lending more than 10% to borrowers abroad. There is more cross-border lending in the Asia-Pacific region (around 40% of platforms lending more than 10% abroad), and the pattern of cross-border flows appears broadly similar for both lending and raising debt.

Scandals at FinTech platforms

Scandals at FinTech platforms

Over the past 18 months, there have been a number of scandals in the FinTech lending sector.

While the fallout from these incidents has been limited, each one has raised concerns about performance and has attracted the attention of regulators to a less regulated industry.

Lending Club (United States): In May 2016, Lending Club, the largest US marketplace lending platform and one of only a few that are publicly listed, announced that the company had repurchased USD 22 million of near-prime personal loans previously sold to a single investor. Lending Club stated that the repurchased loans did not conform to the requirements of the buyer, and an internal review revealed evidence of data manipulation on certain noncredit fields. Concurrently, Lending Club announced that it had discovered a previously undisclosed ownership interest of senior executives in a fund designed to invest in marketplace loans. These disclosures resulted in the resignation of the CEO and several other senior executives.

While spillover effects to other platforms were relatively limited, this incident has prompted greater regulatory and investor scrutiny. Market participants reported that investors were subsequently seeking greater transparency in deals and underwriting practices.

TrustBuddy (Sweden): TrustBuddy was a P2P lending platform based in Stockholm. Launched in 2009, the platform originally specialised in payday loans, but was expanding into more conventional consumer loans. In August 2015, after reporting significant losses and as part of a transition to a broader focus on consumer lending, TrustBuddy brought in a new management team. The new team found evidence of misconduct, and an internal investigation revealed that the platform owed significantly more to investors than it held in assets. It appeared that TrustBuddy had been allocating new lender capital to cover bad debts, and using capital to make loans to borrowers without assigning the loans to a lender.

TrustBuddy reported the situation to the Swedish Financial Services Authority, which ordered TrustBuddy to cease its operations immediately. Trading in TrustBuddy shares was also suspended, and the platform filed for bankruptcy several days later.

While direct market reaction to this platform failure was muted, the incident raised questions about the safety of FinTech lending, and has prompted further regulatory scrutiny.

Ezubao (China): Ezubao, a Chinese FinTech lender purportedly active in small business lending, experienced the largest financial fraud in Chinese history. Ezubao unexpectedly stopped operating in December 2015, and ongoing customer investor complaints spurred a police investigation. In early 2016, it was revealed that Ezubao was a massive Ponzi scheme, in which more than 900,000 individual investors were defrauded of USD 7.6 billion. The platform, founded in 2014, was a relative newcomer to the market, but came under investigation for suspected illegal business practices early on. Most of the products offered by Ezubao were discovered to be fake, and the company was nothing more than a vehicle used to enrich top executives.

The FinTech lending industry in China is large and very fragmented. While the stock price of another large Chinese P2P lender, Yirendai, dropped precipitously around the time of the Ezubao announcement, it rebounded quickly. Other platforms do not appear to have been affected by the negative headlines.

Financial stability implications of FinTech credit

At this stage, the small size of FinTech credit relative to credit extended by traditional intermediaries limits the direct impact on financial stability across major jurisdictions.

However, a significantly larger share of FinTech-facilitated credit in the financial system could present a mix of financial stability benefits and risks in the future. Among potential benefits are effects associated with financial inclusion, more diversity in credit provision and efficiency pressures on incumbents. Among the risks are a potential deterioration of lending standards, increased procyclicality of credit provision, and a disorderly impact on traditional banks, for example through revenue erosion or additional risk-taking. FinTech credit also may pose

challenges for regulators in relation to the regulatory perimeter and monitoring of credit activity.

It is important to emphasise that FinTech credit is currently very small in nearly all jurisdictions. Perhaps only in the UK does P2P lending appear to be a significant source of credit to a particular segment – it accounted for nearly 14% of equivalent gross bank lending flows to small businesses in 2015. Reflecting the current small overall size of the sector, much of the analysis in this section is based on the assumption that FinTech credit continues to expand at a fast pace and that it becomes a significant share of credit activity. This analysis does not attempt to assess the likelihood of such an outcome.

Bearing in mind the pace of innovation and the rapid development of the industry, this section considers the implications for financial stability – both benefits and risks – of FinTech platforms becoming material providers of credit. It also considers the implications of the use

of securitisation to fund FinTech credit provision and the possible response from incumbent banks to the growth of FinTech credit.

The emergence of FinTech platforms has led to, and will continue to lead to, responses from the traditional banking sector. Specifically, banks may: (i) seek to acquire, or set up their own, FinTech credit platforms; (ii) make use of similar technologies for the traditional on-balance sheet lending business, such as those for credit assessment, either by developing them in-house or by partnering with FinTech credit platforms; (iii) invest directly in the loans of FinTech credit platforms; or (iv) retreat from market segments where FinTech credit platforms have a growing competitive advantage. The financial stability implications differ by scenario, but a few general trends may be surmised.

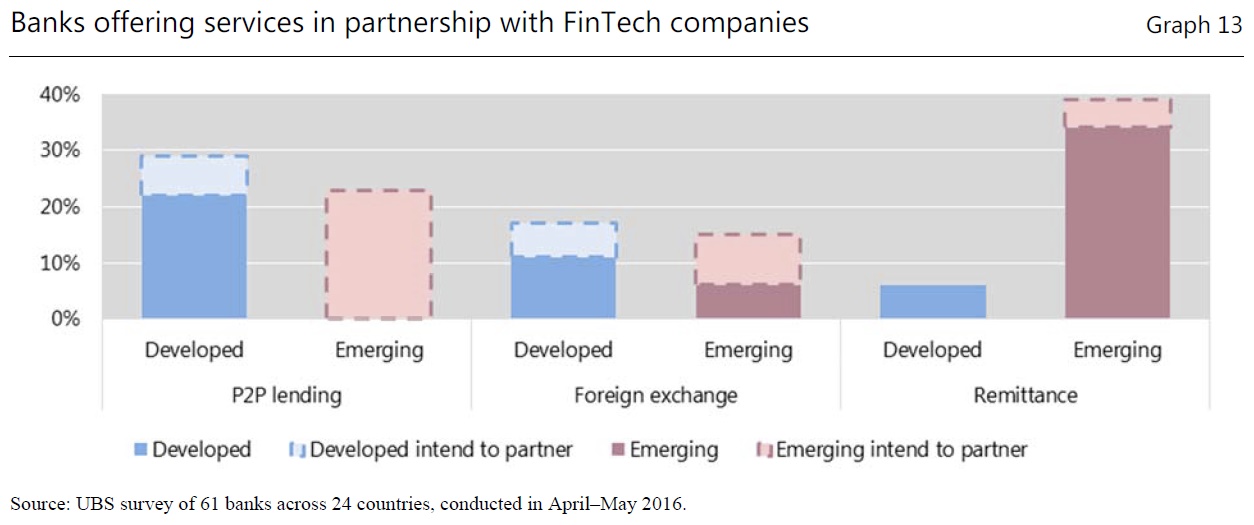

The growing adoption of online platforms and competitive pressures may lead to the greater efficiency of incumbent banks. By acquiring new online and data-based technologies, banks may “leapfrog” some current challenges in legacy IT systems. Similarly, successful partnerships between banks and FinTech platforms could create an opportunity to improve risk analysis or offer a better service to a particular segment of the market (such as the small loans segment). According to a UBS survey, around 22% of developed market banks have a partnership with a P2P lending platform. No emerging market banks surveyed reported having a partnership, but 23% intend to form a partnership in the future.