The RBA has release an FOI response relating to documents created since 1 July 2015 containing information on Australian metropolitan apartment vacancy rates.

They say that a first look at the data indicates that the large additions to supply may be weighing on the apartment markets in inner-city Brisbane and Melbourne. It also highlights the strength of current conditions in the Sydney apartment market, whereas Perth and areas heavily exposed to the mining industry are experiencing some weakness in housing markets

The substantial volume of apartment construction currently taking place across Australia has been concentrated in Sydney, Melbourne and Brisbane. The large amount of expected apartment completions over the coming years has led to concerns around potential oversupply, particularly in the inner-city areas of Brisbane and Melbourne. By number, these 3 city’s CBDs are forecast to have the largest amount of apartment completions over the coming two years As a share of the existing stock, the new forecast supply in Brisbane CBD will increase the dwelling stock in that area by 25 per cent. Adjacent areas to the Brisbane CBD, such as Brisbane Inner – North, and Holland Park – Yeronga are also forecast to have substantial increases in supply.

In Melbourne, the total number of new units is estimated at over 16 000 over the next two years, well above the forecast increase in other areas and as in Brisbane, neighbouring areas such as Port Phillip are also expected to have large numbers of new units.

Liaison suggests developers will increasingly offer rental guarantees as apartment supply increases (as a way of securing investor sales) and will be quick to adjust rents in response to vacancies. This raises the risk that a ‘flight to quality’ will translate to the broader apartment market over time through softer demand for older low quality, low amenity apartments.

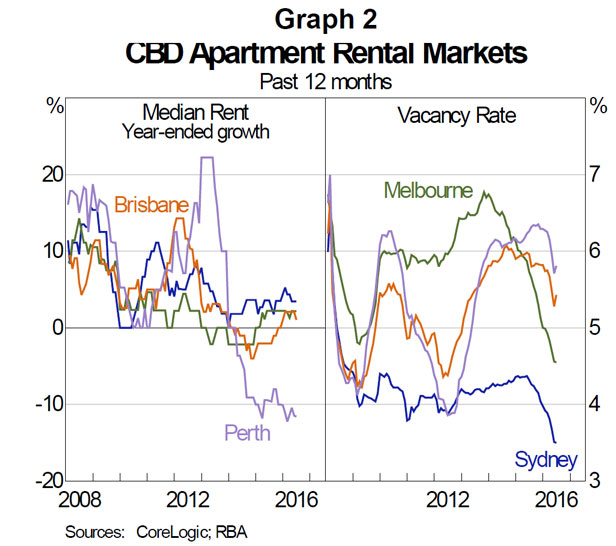

In Sydney, the areas forecast to have large numbers of new units are more geographically dispersed and the proportional increase to the dwelling stock is generally smaller than for Melbourne and Brisbane. The dataset provides information about market conditions at a more granular level. For example, CBD apartment market conditions differ markedly across cities; the weakness in the Perth economy has led to sizeable declines in apartment values and rents as well as elevated vacancy rates, Brisbane and Melbourne’s apartment market conditions are subdued, while Sydney’s remains strong.

For Greater Sydney, expected apartment completions are higher than in the other capital cities. But oversupply is less of a concern, because this expected supply forms a lower share of the dwelling stock and is relatively spread out across the inner and middle suburbs. For those areas within Sydney forecast to experience larger increases in supply relative to the existing dwelling stock, (such as Strathfield – Burwood – Ashfield, Parramatta, Ryde – Hunters Hill and Auburn), there is little sign that oversupply concerns are weighing on these areas, with both value and rental growth remaining relatively strong However, in Melbourne and Brisbane, value growth in areas with the largest amount of expected completions (such as Melbourne City and Brisbane Inner) is relatively weak.

In Darwin, the housing market faces major headwinds as population growth slows. Contacts reported that high-density housing is oversupplied after years of strong building activity, which has led to falls in rents and prices and a rise in vacancy rates. High-rise construction has fallen significantly and building companies have had to adapt by rapidly shedding staff.

Apartment vacancy rates are already the highest of any capital city and residential rents have fallen considerably “white collar” workers – such as in engineering and design – do rent apartments. These highly-paid workers are either leaving now or have already left, which could partially explain the high vacancy rates already in Darwin. The decrease in accommodation costs resulted in Darwin’s CPI growth falling to around 0 per cent in year-ended terms in June 2016.