The latest RBA Financial Stability Review includes coverage on the Banks’ Exposures to Inner-city Apartment Markets. They say banks are most exposed to inner-city housing markets through their mortgage lending rather than via their development lending. Sydney and Melbourne have the largest exposures. That said, they downplay the risks, thanks to the run-up in prices providing a buffer (though this is not true for new transactions) whilst admitting that there is no data on the geographic footprint of mortgage lending in the returns the banks provide, and not all banks would necessarily have the same level of exposures. Another area where we think better data is needed. Also, what happens if off-the-plan purchasers walk away before completion?

The large number of new apartments recently completed and currently under construction in many capital cities raises the risk of a marked oversupply in some geographic areas. The banking system’s exposure to these apartment markets arises from its financing of apartment construction as well as lending to the purchasers of the apartments once construction is complete. This box examines the banking system’s development and mortgage exposures in the inner-city areas of Brisbane, Melbourne and Sydney, where apartment construction has recently been most concentrated.

As indicated here, if apartment market conditions were to deteriorate in these inner-city areas it is more likely that banks would experience material losses on their development lending rather than on their mortgages. This is because of both a higher probability of default and higher loss-given-default on their development lending than on their mortgage lending for apartment purchases. However, while this box examines the situation for the Australian banking system as a whole, individual banks may have more concentrated exposures in certain geographic areas, including exposures to riskier or lower-quality developments, and hence it is unlikely that losses would be evenly distributed across the banking system if a downturn were to happen.

Current Market Conditions

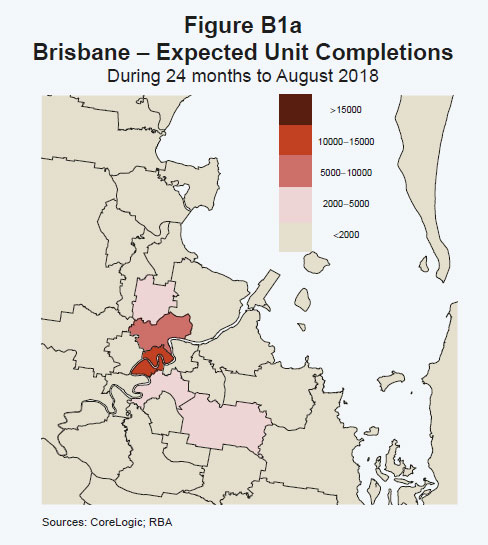

Following the marked pick-up in apartment construction in recent years, inner-city Melbourne is forecast to have the largest number of completions (around 16 000) over the next two years, followed by Brisbane (12 000) and Sydney (10 000) (Figure B1a, Figure B1b, Figure B1c).

In Brisbane and Melbourne these new apartments will represent a far larger increase in the dwelling stock than in Sydney. Furthermore, apartment price and rental growth in Brisbane and Melbourne are relatively subdued – notwithstanding some strengthening in rents in Melbourne of late – and rental vacancy rates are higher than in Sydney (Graph B1). It is therefore foreseeable that these additions to the stock will have a greater effect on housing market conditions in these areas.

Exposures

The routine regulatory data disclosures do not require banks to report their exposures by geographic region. Nonetheless, data on banks’ total Australian mortgage and development lending – along with data on construction activity, housing prices and buyer profile in these areas – can provide some rough estimates of the magnitude of these exposures and hence a broad indication of how exposed banks are to a downturn in these markets.

Overall, these estimates suggest that, by value, banks are most exposed to inner-city housing markets through their mortgage lending rather than via their development lending (Graph B2). The data suggest that around 2–5 per cent of banks’ total outstanding mortgage lending is to inner-city Brisbane, Melbourne and Sydney, and this share is likely to grow as the apartments currently under construction are completed. At around $20– 30 billion, mortgage exposures are estimated to be larger in Sydney, reflecting Sydney’s higher apartment prices and greater number of mortgaged dwellings, than in Brisbane and Melbourne where mortgage exposures are estimated at around $10–20 billion in each inner-city area. By contrast, the available data suggest that around one-fifth of banks’ total residential development lending is to these areas. Development exposures are a little larger in Melbourne and Brisbane than in Sydney, due to the greater volume of apartment construction currently underway, though they are each less than $5 billion.

Potential Losses

Banks would experience losses on these exposures in default events where the value of the properties is insufficient to cover the debt outstanding. Australian mortgage lending has historically had very low default rates – around ½ per cent – and had high levels of collateralisation. In Sydney in particular, a very large price fall would be required before the banks would experience sizeable losses, since the rapid price growth over recent years has increased borrowers’ equity in their apartments and thereby lowered banks’ losses-given-default.

In contrast, inner-city Melbourne and Brisbane have experienced far less price growth, limiting borrowers’ accumulation of equity. To gain a broad indication of the size of potential losses to banks, one can consider a hypothetical scenario where default rates rose to between 5 and 15 per cent on inner-city mortgages, and then combine this with a range of housing price falls. Under this scenario, bank losses remain very low until price falls reach over 25 per cent or so (Graph B3).

Repeating this scenario for developer exposures is challenging, because the exposures are more idiosyncratic and the largest losses can be on incomplete developments. In addition, the average level of developer equity in their apartment projects is not readily available and anecdotal evidence suggests that it varies significantly by building. A simple way to model potential losses on developer lending is to use loss rates in line with those seen on all Australian residential development lending during the financial crisis.

In this scenario, losses still remain fairly small (Graph B4). Alternative comparisons are the Spanish and Irish financial crisis experiences, which were associated with housing price falls of more than 30 and 50 per cent, respectively, and impairment rates on commercial property of over 30 per cent.

In these situations, the losses to banks would be several times larger than the recent Australian experience. However, Australia is not facing the same economic and financial headwinds as Spain or Ireland did during the financial crisis, where the extent of overbuilding was much greater and prevalent across their entire countries, contributing to very sharp deteriorations in economic conditions. More likely, any oversupply in Australia would be more localised to certain geographic areas, and potential price falls tempered as the population moved to absorb the new (and cheaper) supply of housing in these areas over time.