Financial system vulnerabilities remain elevated and more effort is required to ensure that the system remains resilient over the longer-term, Reserve Bank Governor Adrian Orr says in releasing the November Financial Stability Report.

International risks to the financial system have increased. Global growth has slowed amid continued uncertainty about the outlook for world trade. This has resulted in reductions in long-term interest rates to historic lows, including in New Zealand. While necessary to maintain near-term inflation and employment objectives, prolonged low interest rates can promote excess debt and investment risk-taking, and overheat asset prices, Mr Orr says.

Mr Orr noted that the Reserve Bank’s Loan-to-Value Ratio (LVR) restrictions have been successful in reducing the more excessive household mortgage lending, thereby improving the resilience of banks to a significant deterioration in economic conditions.

But, there remains the risk that prolonged low interest rates could lead to a resurgence in higher-risk lending. As such, we have decided to leave the LVR restrictions at current levels at this point in time.

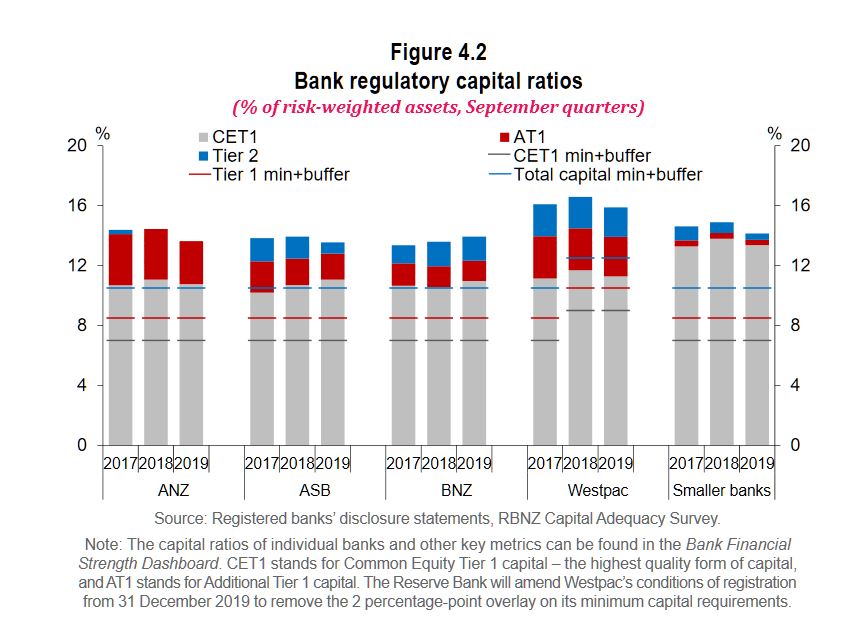

Mr Orr says the Reserve Bank is committed to bolstering the long-term resilience of the financial system. “Strong bank capital buffers are key to enabling banks to absorb losses and continue operating when faced with unexpected developments. The Reserve Bank has proposed increasing these buffers further with final decisions on the Capital Review proposals to be announced on 5 December.”

Deputy Governor Geoff Bascand says good governance and robust risk management processes within financial institutions are important to maintain long term resilience. Our recent reviews of banks and life insurers, and the number of recent breaches in key regulatory requirements, reinforces the need for financial institutions to improve their behaviour.

“We are engaging with industry to ensure that they strengthen their own assurance processes and controls. We have also reviewed our own supervisory strategy and will be taking a more intensive approach, which will involve greater scrutiny of institutions’ compliance,” Mr Bascand says.

“Some life insurers have low solvency buffers over minimum requirements. Recent falls in long-term interest rates are putting further pressure on solvency ratios for some of these insurers. Affected insurers are preparing plans to increase solvency ratios and are subject to enhanced supervisory engagement. This highlights the need for insurers to maintain strong buffers, and insurer solvency requirements will be reviewed alongside an upcoming review of the Insurance (Prudential Supervision) Act.”